- Return of Fed rate cut bets after Iran war ceasefire.

- US Producer Price Index numbers to test whether the Fed can resume interest rate cuts.

- ECB meeting minutes and UK data to test ECB and BoE forecasts.

- Australian traders await the AU employment report and China’s GDP.

Dollar declines amid ceasefire in the Middle East

The US dollar started the week lower on hopes that the United States and Iran could work things out and end their conflict, and its decline accelerated on Wednesday after headlines emerged that the two countries had agreed to a two-week ceasefire, including reopening the Strait of Hormuz, through which a fifth of the world’s oil shipments pass. The White House confirmed that Israel was also on board for the ceasefire.

WTI fell as much as 16% on the news and stocks rose significantly as the news came just one day after US President Trump threatened widespread attacks on civilian infrastructure, specifically warning that “an entire civilization will die tonight” if his demands are not met.

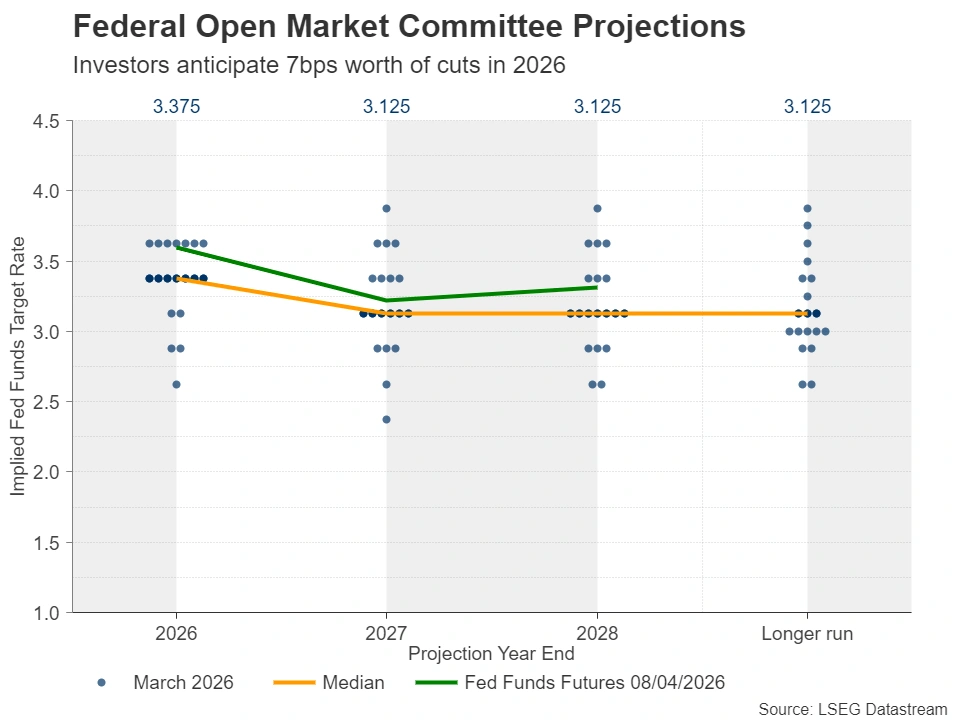

The ceasefire and falling oil prices eased inflation fears, prompting investors to begin speculating that the Federal Reserve may need to resume cutting interest rates after the truce. According to Federal Reserve funds futures, there is about a 30% chance of a quarter-percentage point cut by the end of the year.

That’s even after minutes of the Federal Open Market Committee’s latest decision showed that a growing group of Fed officials believe raising interest rates may be necessary to prevent inflation from spiraling out of control. Perhaps, with the ceasefire now in place, investors were convinced that the rise in oil prices would be temporary, as Fed Chair Powell emphasized in his remarks last week.

Focus shifts to US Producer Price Index inflation data

Next week looks relatively light compared to the previous two weeks, as the only US releases worth mentioning are the March Producer Price Index numbers, due on Tuesday, as well as industrial and manufacturing production rates, due on Thursday.

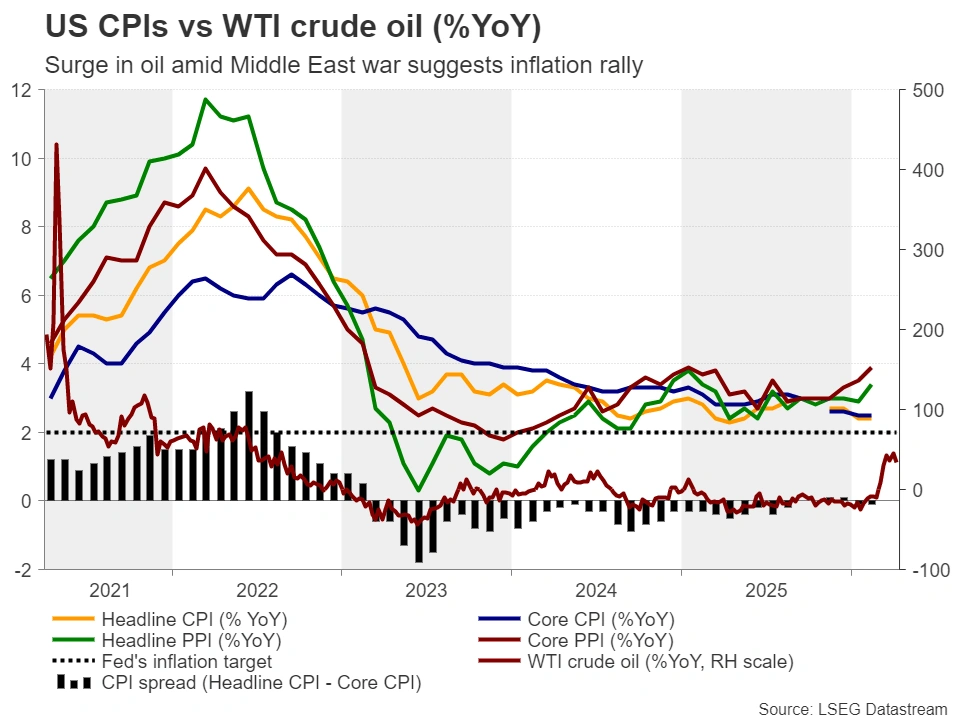

A strong rise in PPI numbers may revive fears that the inflation problem may be more serious than initially thought, as higher producer prices now could translate into firmer consumer prices in the following months. Therefore, anything that suggests rates may remain high for longer may persuade investors to scale back their bets on a rate cut.

However, provided the truce in the Middle East remains in effect, this is unlikely to revive bets on an interest rate hike and, therefore, the dollar is unlikely to achieve a meaningful recovery.

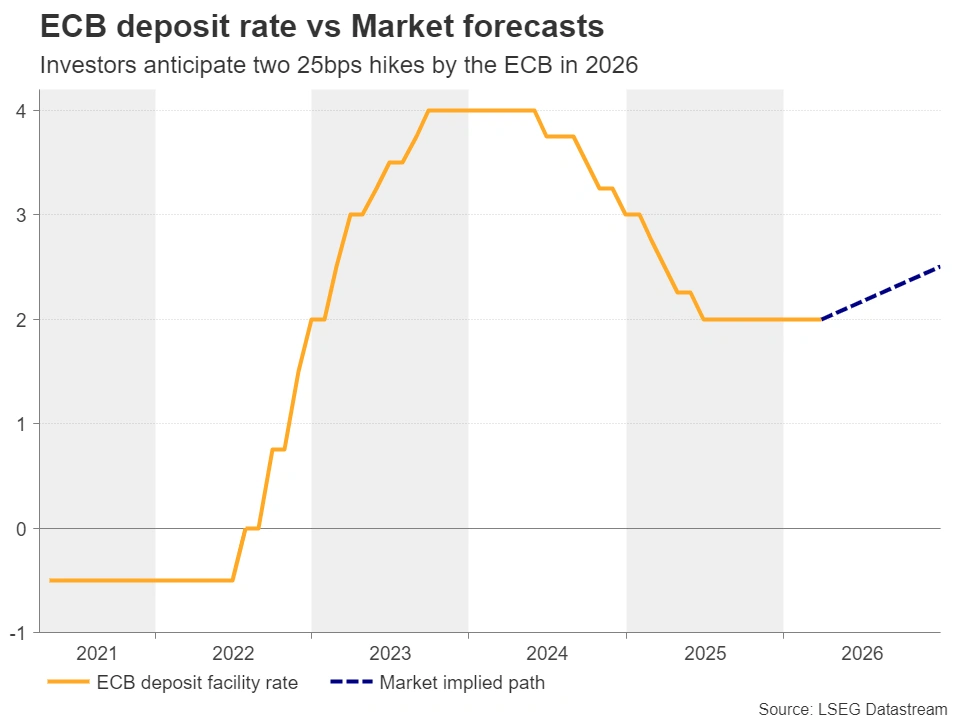

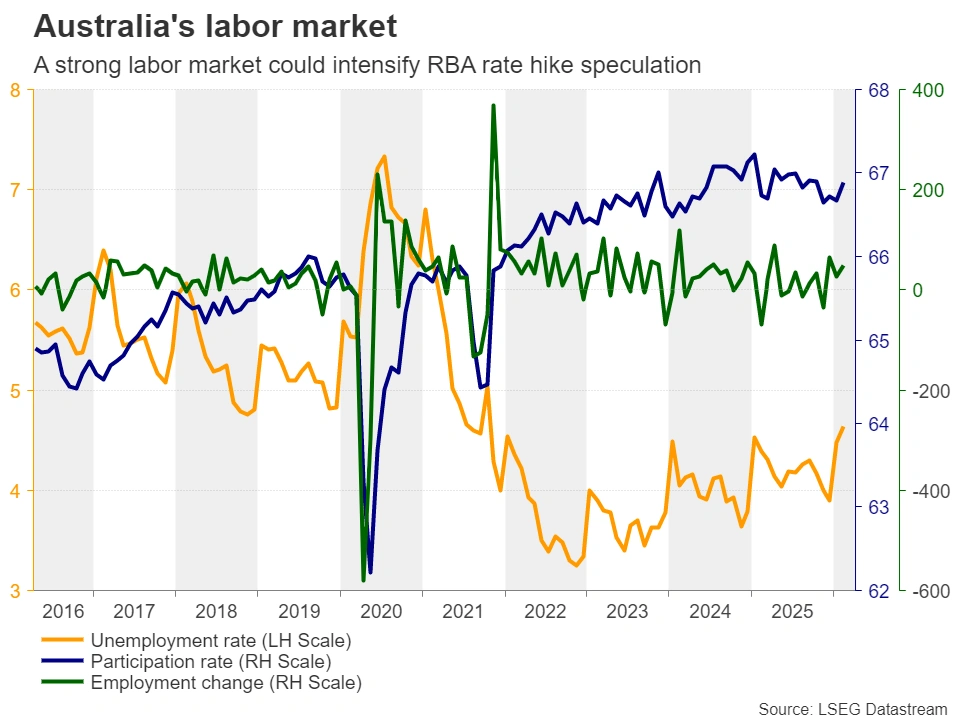

After all, despite lowering interest rate paths elsewhere as well, most major central banks are still expected to continue raising interest rates, marking a divergence between them and the Fed. The European Central Bank is still expected to hit the rate hike button twice this year, while the Bank of England is set to raise interest rates by 30 basis points. The possibility of the Bank of Japan raising interest rates later this month remains a coin toss, and there is a strong 60% chance the Reserve Bank of Australia will go ahead with a third consecutive quarter-point rate hike at its next meeting in May.

Minutes of the European Central Bank meeting reveal the extent of officials’ readiness to raise interest rates

Speaking of the European Central Bank, the minutes of its latest monetary policy decision, held on March 19, will be released on Thursday. At that meeting, policymakers kept interest rates unchanged, but indicated they were closely monitoring growth and inflation risks from rising energy prices amid the war in Iran, adding that they were ready to adjust their strategy if necessary.

More recently, Dimitar Radev, a policymaker at the European Central Bank, noted that euro zone inflation expectations are at risk of rising more quickly, and that the bank must be prepared to raise interest rates quickly. This, combined with flash CPI data that revealed a jump in headline inflation to 2.5% year-on-year in March from 1.9%, allowed investors to maintain their bets of around 50 basis points for a rate hike by the end of the year.

Therefore, Euro traders will scrutinize the meeting minutes to see how willing other policymakers are to shift to raising interest rates if the situation warrants it. Although this information may be considered outdated, because the meeting took place amid an escalating war, the intense hawkish flavor could reinforce the idea that the ECB may consider raising interest rates even after the ceasefire, allowing the euro to continue to rise against its US counterpart.

Weak data in the UK may impact the Bank of England’s bets on raising interest rates

In the UK, monthly GDP, industrial and manufacturing production figures, as well as trade data, will all be released for February. Weak growth figures even before the outbreak of war in the Middle East may lead investors to question whether it would be wise for the Bank of England to proceed with raising interest rates, especially in light of the ceasefire.

Therefore, a decline in interest rate cut bets could weigh on the pound, but with the US dollar weaker, any losses in the pound may be more prominent on the EUR/GBP pair.

Australian jobs report and Chinese GDP move the Australian dollar

The risk-linked Australian dollar was among the currencies that benefited the most amid the truce announcement, rising as much as 1.75% on Wednesday. The increase in risk appetite and the RBA’s still hawkish interest rate expectations are very supportive variables for the currency. Thursday’s strong March employment report could allow investors to exploit the prospect of a third consecutive 25 basis point RBA hike and thus allow further advances in the commodity currency.

Australian traders are likely to focus on Chinese data as well, as China is Australia’s main trading partner. During the Asian session on Wednesday, the world’s second largest economy will release its trade data for March. First-quarter GDP is scheduled to be released on Thursday, along with industrial production, retail sales, investment in fixed assets and the unemployment rate, all for March.

Although trade tensions between the United States and China have eased, the conflict in the Middle East and the rise in oil prices during March may have left their mark on the Chinese economy, which is the world’s largest oil importer. If the data indicates that China was able to withstand the pressure, the Australian dollar could rise further.