Attention is turning strongly to Islamabad as the United States and Iran begin their first high-level talks since the start of the war, with markets looking for signs of a breakthrough that could develop into a broader agreement in Islamabad. The result will be a defining moment for energy markets, inflation, and global risk sentiment, with delegations led by US Vice President J.D. Vance already on the ground to see what could shape the course of the ceasefire and beyond.

The Islamabad meeting, at its core, is not just another diplomatic event, but the most important overall catalyst in the current environment. The talks aim to transform the fragile two-week ceasefire into a more sustainable framework, with ramifications extending from the reopening of the Strait of Hormuz to the normalization of global energy flows.

From here, Three broad scenarios appear. The collapse of the talks will see markets quickly return to pre-ceasefire mode, with oil rising back towards crisis levels and risk sentiment deteriorating. A “freeze” scenario – where dialogue continues without tangible progress – is likely to leave markets range bound, with optimism fading but without any new escalation expected. The third and most market-moving outcome is the emergence of a framework for a final agreement, even without a final agreement being reached.

Crucially, Markets will not wait for signed agreements, but rather are moving on credible paths. If investors see even a partial framework emerging from Islamabad, pricing could quickly shift toward a de-escalation scenario. In this case, the dollar would be at risk of a sharp sell-off, driven by improved risk appetite, lower oil prices, and a renewed focus on policy divergence against the Fed.

Three scenarios: crash, freeze or frame

The basic framework of the Islamabad talks revolves around three possible paths: collapse, freeze, or framework. Each scenario represents a different stage of geopolitical risk pricing and carries clear implications for global markets.

1. Collapse: Reset “Operation Epic Rage”.

A collapse would be the most annoying outcome. Failure to reach common ground is likely to return markets to their pre-ceasefire mode, with oil prices rebounding sharply toward $120 and stocks reversing last week’s gains. Investors will quickly reposition their positions in preparation for renewed escalation, re-emergence of inflation risks and tightening of financial conditions.

2. “Freeze”: limited-range disinfectant

On the other hand, the “freeze” scenario would exacerbate the current uncertainty. Continuing dialogue without concrete commitments – particularly regarding the Strait of Hormuz or sanctions – is likely to derail the recent rise. Markets can drift sideways, as the absence of progress limits optimism while the absence of escalation limits downside.

3. Framework: Agreement management at the forefront

The most positive scenario is that a framework for an eventual Islamabad agreement emerges. Importantly, markets do not need a final agreement to respond. Even incremental progress – such as agreement on key issues or timelines – can be enough to stimulate forward-looking positioning. With risk assets already supported by strong momentum since the ceasefire announcement, traders may move early, pushing stocks towards new highs and pulling oil back towards $90 or even lower as expectations shift towards de-escalation.

Risk appetite momentum may push the dollar lower

If markets begin to embark on a reliable path toward the Islamabad agreement, the first and most immediate driver of dollar weakness will be Strong extension of risk sentiment. Stock markets have already built strong upward momentum, with the S&P 500 posting its best weekly performance since November and now sitting within striking distance of record highs. In such an environment, investors are likely to lean heavily towards risky assets.

At the same time, The Fed’s forecasts provide a crucial tailwind to the move. Recent inflation data supports the view that the oil shock has not yet translated into broader inflationary pressures. Core CPI rose only modestly from 2.5% y/y to 2.6% y/y in March, providing little evidence of second-round effects. This would keep the Fed’s “temporary” narrative intact, allowing policymakers to consider an energy-driven rise in headline inflation rates.

However, there are concerns about inflation expectations. The University of Michigan poll showed a sharp jump in one-year expectations from 3.8% to 4.8%, along with a rise in long-term expectations to 3.4%. On the surface, this may challenge the Fed’s confidence. But these readings appear reactionary, as most responses were collected before the April 7 ceasefire and subsequent decline in oil prices.

Moreover, the outlook is likely to be highly sensitive to developments in energy markets. If oil prices decline due to progress toward the Islamabad agreement, inflation expectations could reverse just as quickly as they rose. This would reinforce the view that current inflation fears have not yet taken hold.

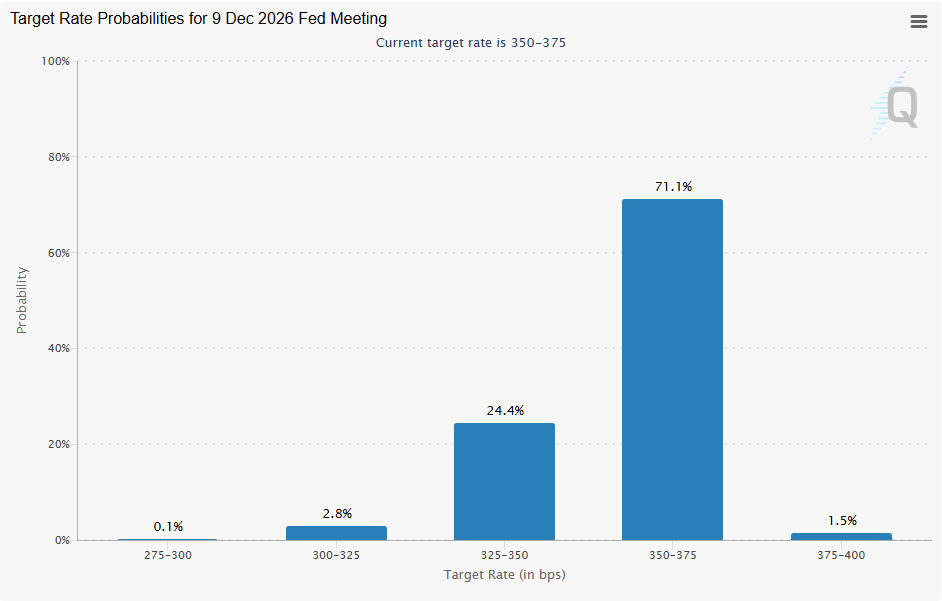

Market pricing reflects this balance. Futures indicate little possibility of a rate hike by the end of the year, with odds close to 1.5%. Majority expectations remain for the Fed to stabilize at 3.50-3.75% before eventually easing. In other words, interest rate cuts are seen as overdue rather than cancelled.

Rise vs. Hold: The Dichotomy That Could Sink the Dollar

The second main driver of dollar weakness lies in whether markets anticipate the Islamabad agreement Widening central bank policy gap. In a de-escalation scenario, the Fed would likely remain in a holding pattern in the near term and then return to cutting interest rates once the oil shock fades. This puts it firmly in the “stick to easing” camp, in contrast to many major central banks that are either tightening or preparing for further tightening.

This emerging dichotomy between “raise rates versus wait” is becoming increasingly clear. The European Central Bank, the Reserve Bank of Australia, the Bank of Japan, and possibly the Bank of England form the hawkish camp, while the Federal Reserve, Bank of Canada, Reserve Bank of New Zealand and Swiss National Bank remain more dovish. Such divergence creates structural headwinds for the dollar by depressing the yield advantage.

the European Central Bankin particular, stand out. With its benchmark rate at 2.00%, which is close to neutral, it has more room to raise interest rates than the Fed’s range of 3.50-3.75%. Europe’s increasing sensitivity to energy shocks also increases the urgency of tightening monetary policy, as policymakers seek to prevent the effects of second-round inflation from taking hold.

In contrast, the Fed is already operating near the upper end of its neutral range, as shown in the minutes of the recent FOMC meeting. With the labor market stable rather than overactive, policymakers can pause and evaluate the incoming data. If inflationary pressures decline alongside lower oil prices, the next step is likely to be a reduction rather than an increase.

the RBA This further reinforces the divergence. It is already facing an active tightening cycle this year, facing inflationary pressures resulting from strong domestic demand and supply-side disruptions associated with the closure of the Strait of Hormuz. Markets are anticipating additional increases in the coming months, widening the policy gap with the Fed.

In this context, The policy divergence acts as a powerful secondary force that amplifies the dollar’s downward trend. If risk sentiment starts to move, changing return dynamics could support it, making any sell-off in the dollar sharper and more persistent.

AUD/USD is looking to break the 0.72 level, and EUR/USD will follow if the agreement scenario ends

If the markets reach a credible Islamabad agreement, the forex markets are likely to move decisively. The combination of risk sentiment and widening policy divergence would favor currencies such as the Australian dollar and the euro, while putting continued pressure on the dollar.

Australian Dollar/US Dollar It stands out as the most obvious beneficiary. Improving global risk appetite and widening spread could push it through the key resistance level of 0.72. This would prepare the resumption of the upward trend in the medium term. In such a scenario, a move of AUD/USD towards 0.80 would become more than just a tactical trade, and develop into a base case for carry-focused investors.

EUR/USD It is also positioned to the upside, with a possible retest of the key 1.20 psychological level under a de-escalation scenario. More importantly, the ECB’s tolerance for a stronger euro could have changed. While policymakers have previously expressed concern about the euro being too strong due to its deflationary effect, the current environment is different. As inflationary pressures from energy rise, a stronger euro could help contain import costs, reducing the urgency to resist currency appreciation. Therefore, a sustained break above 1.20 may carry different implications than in previous sessions. Rather than seeing it as a political problem, it can be tolerated – or even welcomed – as part of a broader effort to stabilize inflation.

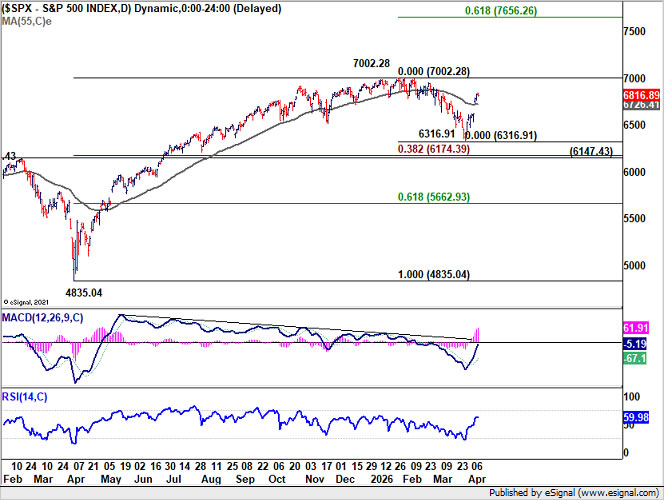

S&P 500 uptrend holds, Dollar Index risks renewed downside

The S&P 500’s strong rebound last week suggests that the corrective decline from 7002.28 has likely completed at 6316.91. Notably, strong support emerged from a key cluster area, including resistance turned support at 6,147.43, the 38.2% retracement from 4,835.04 to 7,002.28 at 6,174.39, and the 55 W moving average (now at 6,457.95). This confluence reinforces the view that the long-term uptrend remains in place.

We should see a retest of the 7002.28 high after that. While the initial uptrend may be limited there, potentially extending the current consolidation pattern with another pullback, a decisive breakout would signal a resumption of the broader uptrend. In this case, the next target is at a 61.8% forecast of 4,835.04 to 7,002.28 from 6,316.91 at 7,656.26.

For the Dollar Index, support at 98.65 is now in focus after last week’s decline. A strong break below this level indicates that the bounce from 95.55 has already reached 100.64. Rejection near the 38.2% retracement from 100.17 to 95.55 at 101.13, combined with the 55 W moving average (now at 99.62), keeps the medium-term outlook bearish.

If the price falls to 98.65, we should see a retest of the low of 95.55 next. A decisive break below this level would confirm a resumption of the broader downtrend from 114.77 (2022 high).

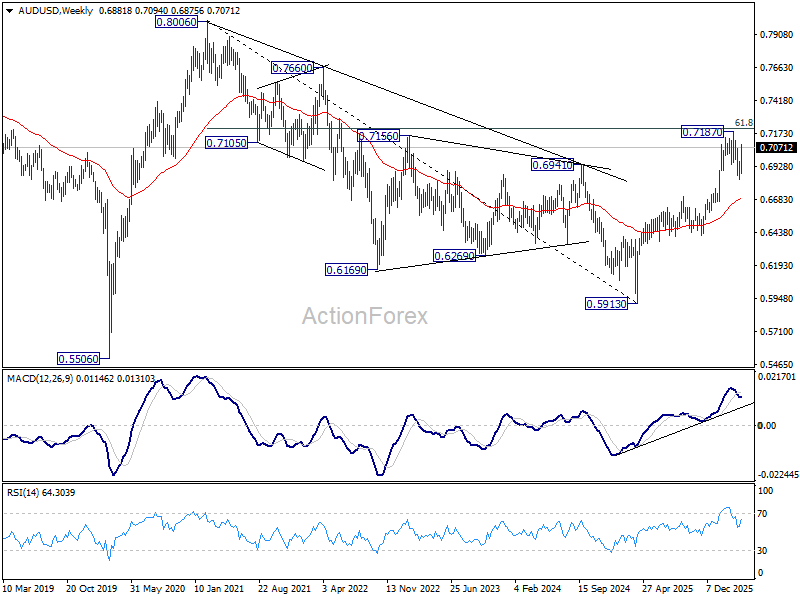

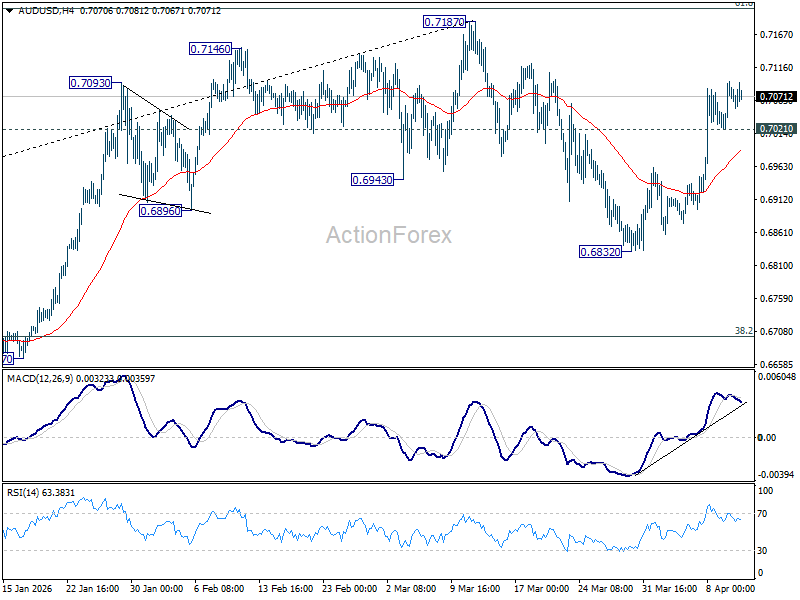

AUD/USD weekly report

The strong recovery of AUD/USD last week suggests that the pullback from 0.7187 has already been completed at 0.6832. Initial bias remains moderate to the upside this week to retest 0.7187. Strong resistance can be seen there for another decline to extend the corrective pattern in the near term. On the downside, minor support at 0.7021 would shift the intraday bias to neutral again first.

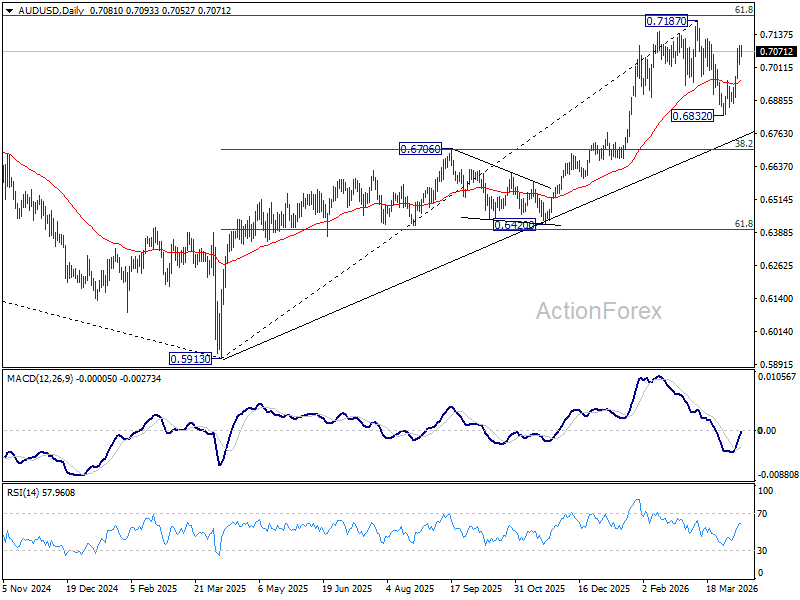

In the bigger picture, as long as the cluster support at 0.6706 holds, a rally from 0.5913 (2024 low) should remain in progress. A decisive break of the 61.8% retracement levels from 0.8006 to 0.5913 at 0.7206 will strengthen the case that it is indeed reversing the downtrend from 0.8006 (2021 high). However, a strong break of 0.6706 would mitigate this bullish case, and bring a deeper decline back to support at 0.6420, and possibly below.

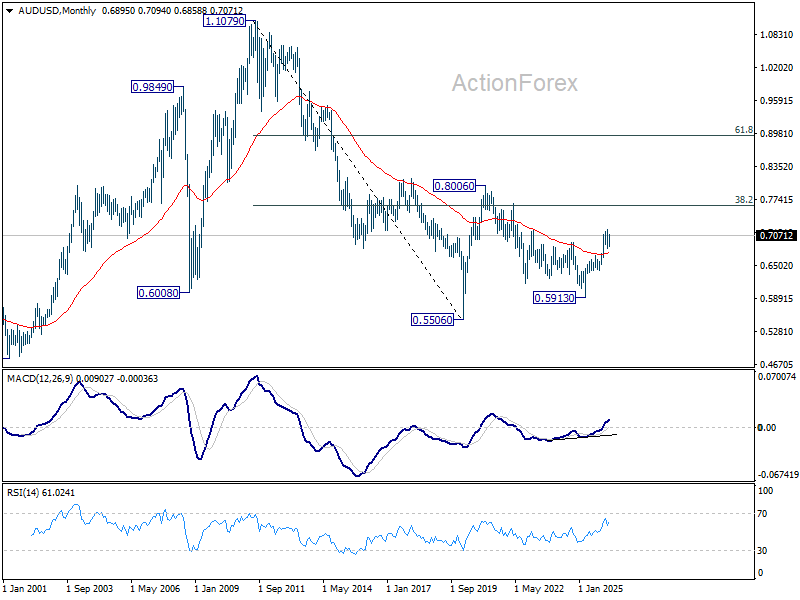

In the long-term picture, the rise from 0.5913 is the third leg of the entire pattern from 0.5506 (2020 low). It is still too early to judge whether this is an impulsive or corrective pattern. But either way, we should see further rise back to 0.8006 and possibly higher. This will remain the preferred case as long as the 55W EMA remains (now at 0.6683).