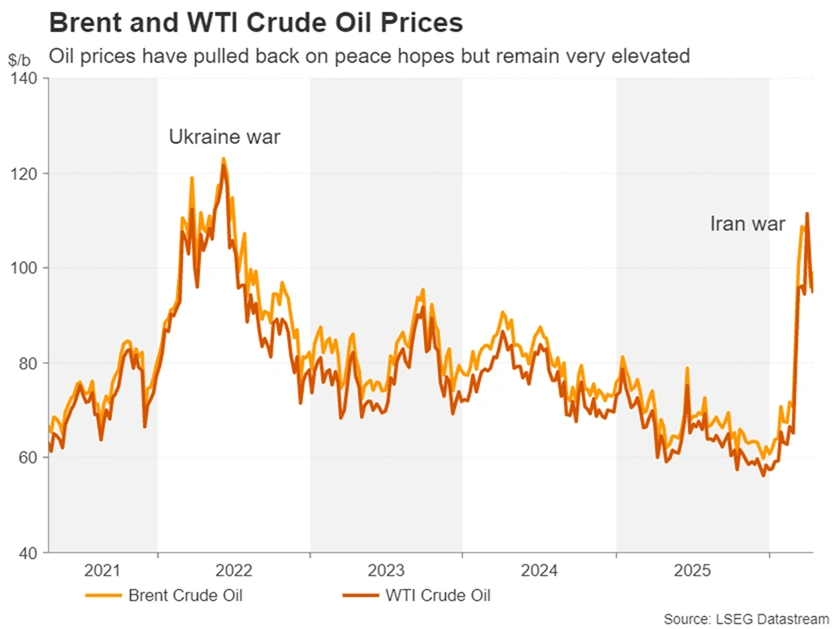

- Hope for an agreement between the United States and Iran is boosting sentiment, but oil prices remain high.

- March CPI is scheduled for Canada, Japan, New Zealand and the United Kingdom.

- April Purchasing Managers’ Indices (PMI) are also available ahead of central bank decisions.

- Kevin Warsh’s Senate hearing is likely to overshadow US data.

Geopolitics must remain in the drivers seat

Hopes are rising that US and Iranian negotiators can reach an agreement in the coming days to end the seven-week war that has damaged energy supplies from the Persian Gulf. There appears to be a good chance of holding a second round of direct talks between the two sides as early as this weekend, after the failure of the first round a week ago.

More importantly, the fragile ceasefire agreed upon 10 days ago is set to expire on Tuesday, so at the very least, investors are hoping for an extension. Reports indicate that the United States and Iran are close to agreeing to a two-week extension to allow more time for negotiations. Despite this, President Trump has indicated that he prefers to reach an agreement without the need for an extension.

Trump believes the war is “very close to being over” but has nonetheless decided to send additional troops to the Middle East, likely increasing pressure on Iran to accept the deal. Another positive development is that Israel and Lebanon also agreed to a ceasefire to stop the fighting between Iran-backed Hezbollah in southern Lebanon and Israeli forces.

However, the decline in oil prices has stalled amid doubts about whether peace in the region can be achieved so quickly and concerns about Trump’s reaction if new negotiations fail again. There has been little relief on the supply front after US warships entered the Strait of Hormuz to blockade ships heading to and from Iranian ports, although other ships are able to pass through it safely.

But Trump appears open to making potential concessions to China, which could allow some Chinese tankers to use Iranian ports — something that is likely to be discussed when he meets with President Xi in mid-May.

Any setback in efforts for peace in the next few days could easily push oil prices above $100. However, stocks are at greater risk of a correction, with Wall Street hitting new highs even before an agreement is reached on how to bring a permanent end to the conflict in the Middle East.

Workshops to face Senate test

Barring any unwelcome escalation with Iran, the main focus in the United States will be on Kevin Warsh’s Senate confirmation hearing. The long-awaited hearing before the Banking Commission, which was postponed due to “delays in paperwork,” has finally been scheduled for Tuesday, April 21.

But there is a much bigger hurdle than paperwork that could stand in the way of finally confirming Trump as the next chairman of the Federal Reserve, succeeding Jerome Powell. All Republican votes on the committee are needed to approve Warsh’s nomination. But Republican Sen. Thom Tillis continues to threaten to derail Warsh’s bid to become Fed chairman unless the Justice Department drops its investigation into Powell and the White House abandons its legal case to remove him.

But with Trump unlikely to agree to such moves, the nomination process could deadlock, adding new uncertainty to markets, with only one month remaining before Powell’s term as president ends.

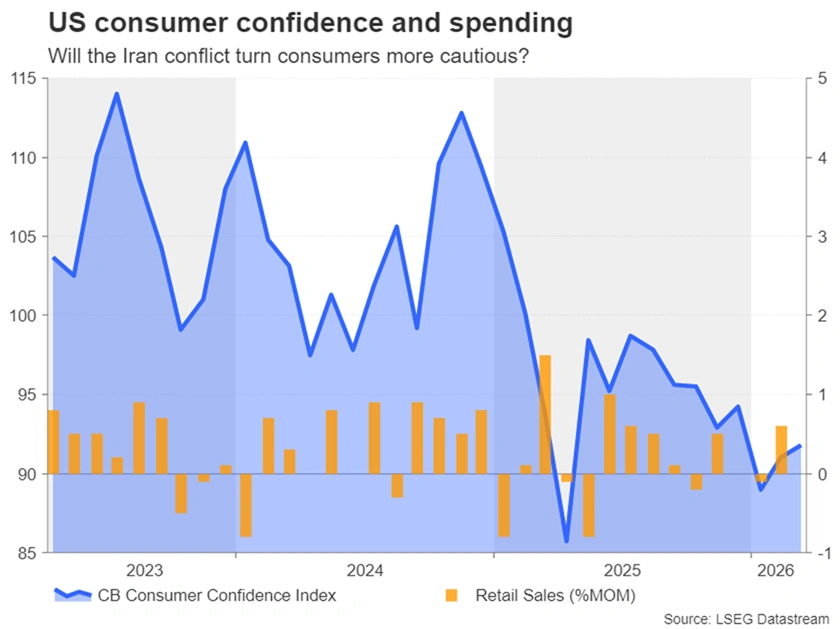

On the data front, next week will be fairly quiet, with retail sales and S&P global PMIs on the economic agenda, while Fed spokespeople will be completely absent as the blackout period ahead of the policy decision scheduled for April 29 begins at midnight on Friday. So the data may not attract much attention unless it disappoints by a significant margin, especially if Tuesday’s retail sales numbers indicate that consumers retreated in March when the United States began its military strikes on Iran.

Sterling prepares for recessionary inflationary data

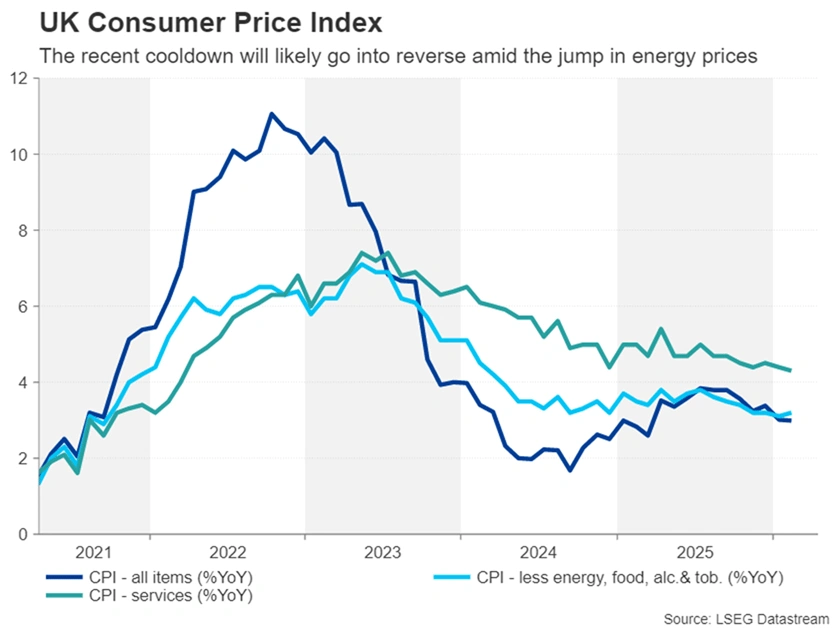

With the US dollar positioned to extend its decline from post-war highs into a third week, the British pound will have a chance to shine as it prepares for a barrage of British data. Employment numbers will be released first on Tuesday, followed by the CPI report on Wednesday, the flash PMI on Thursday, and retail sales on Friday.

The UK labor market has recorded modest job growth since October, but this has not been enough to reduce the unemployment rate, which has risen to 5.2%. Any further increase in the unemployment rate in the three months to February would discourage Bank of England policymakers from raising interest rates too early.

However, hawkish MPC members may need more convincing to stay put if March’s CPI numbers ring alarm bells about inflation returning to the upside. UK inflation has finally started to slow this year, falling to 3.0% year-on-year, but with fuel prices rising on the back of the energy crisis, headline CPI almost certainly reversed course in March when the Iranian conflict began.

Preliminary PMI estimates could get even gloomier if there is a further deterioration in April, raising the possibility of stagflation. On the more positive side, the UK economy appears to have gotten off to a much stronger start in the first two months of 2026 than expected, so any upward surprises in PMIs will give the Bank of England less reason for caution, especially if combined with hotter-than-expected CPI data.

After recovering back above $1.35 this week, the pound may extend its gains beyond $1.37 after an upbeat set of releases.

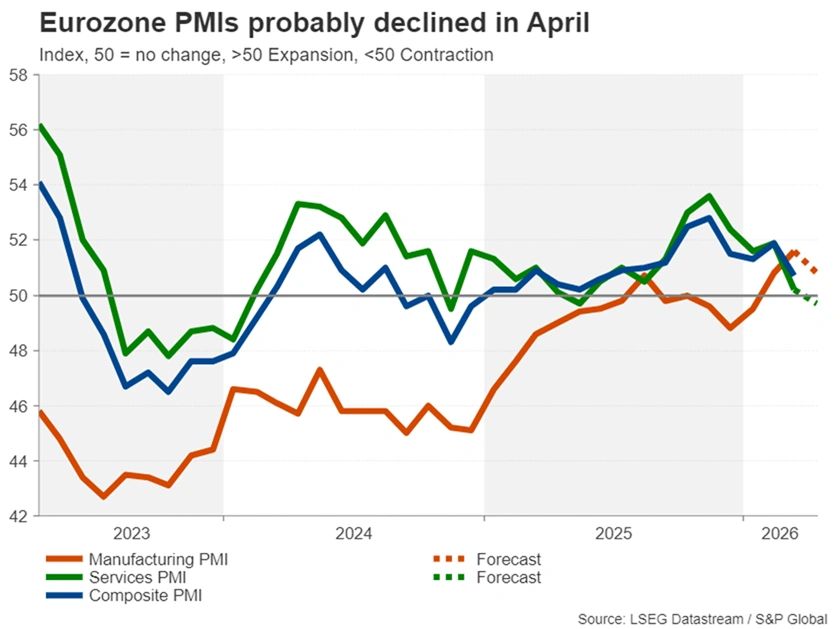

Eurozone PMIs are on the lookout as the European Central Bank considers raising interest rates

April’s PMIs will also grab the spotlight in the Eurozone, where stagflation risks are also rising. However, while the ECB was quick to adopt a hawkish stance immediately after oil prices rose to just under $120, policymakers have since backed down, indicating they are “in no rush” to take a pre-emptive move, with the Bank of England using similar language.

After falling in March, the services PMI is expected to fall again in April, falling below 50 amid pressure on consumers and businesses from a rise in energy prices.

The euro could come under pressure from weaker-than-expected PMI numbers on Thursday, as the European Central Bank will be less inclined to act prematurely if the economy is in trouble.

Euro traders will also be watching German business surveys, with the ZEW economic sentiment index released on Tuesday and the Ifo business climate gauge due on Friday.

The Canadian dollar is unable to reap the benefits of oil’s jump

Japan, Canada and New Zealand will also receive CPI updates next week. The Bank of Canada and the Bank of Japan meet in the last week of April, along with the Federal Reserve, the European Central Bank and the Bank of England, so inflation releases will be closely watched.

Canada’s key inflation measures moderated in February, putting the Bank of Canada in a more comfortable position ahead of an expected rise in the CPI. Moreover, Canada, like the United States, is less energy dependent than Europe and Asia, so the impact of higher oil prices will be less pronounced.

However, a stronger-than-expected CPI report on Monday could boost the prospects for a rate hike from the Bank of Canada, which is currently not fully priced in until October. This may provide some support to the Canadian dollar, which has been lagging other commodity-linked dollars recently, despite Canada being a major oil exporter.

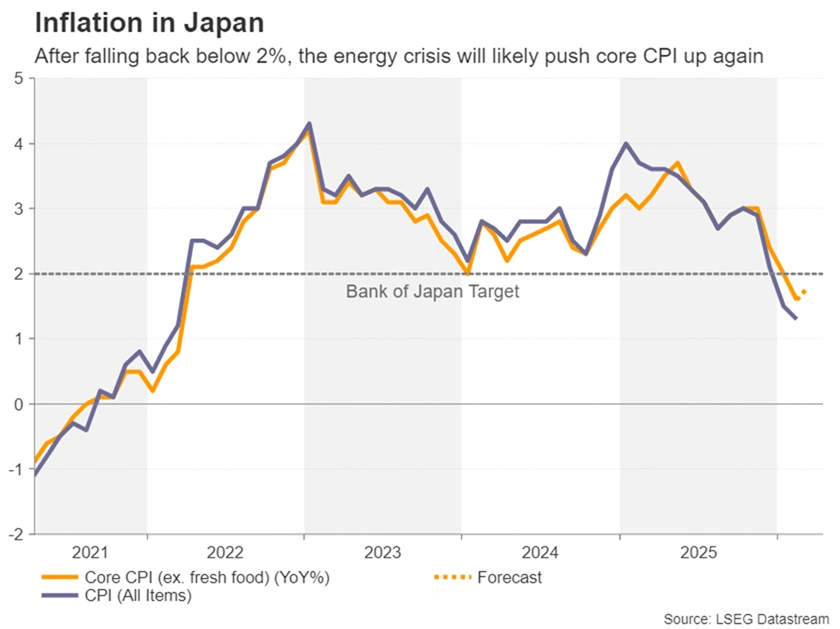

Can Japan’s CPI support the yen?

The yen also performed poorly, barely benefiting from the dollar’s weakness, although the Bank of Japan’s April decision was the most “lively” of all the central bank’s meetings that week.

As usual, the Bank of Japan gave mixed signals about the possibility of a rate hike in April. The Iran war may have made policymakers more cautious in the short term amid concerns about its effects on the economy, but interest rate hikes later in the year are becoming more inevitable.

March’s CPI numbers likely won’t add much clarity to investors regarding the Bank of Japan’s thinking, nor will Thursday’s flash PMIs, leaving the yen exposed. Meanwhile, despite its broader decline, the US dollar remains supported above 158 yen and stands poised to test 160 yen, which is considered a risk zone for intervention.

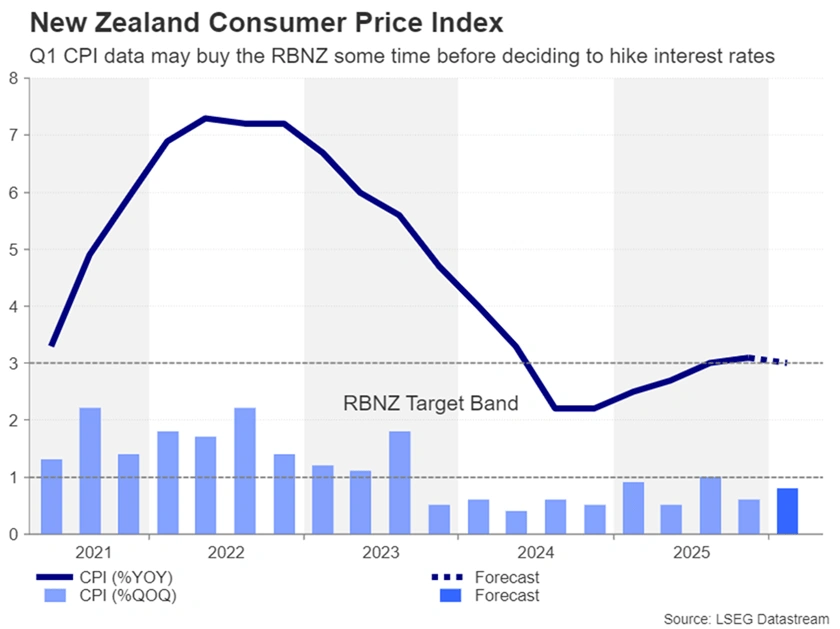

Kiwi awaits Q1 CPI amid RBNZ doubts

Elsewhere, the New Zealand dollar was unable to keep up with its Australian counterpart in April, with the Reserve Bank of New Zealand’s somewhat questionable bias. The Reserve Bank of New Zealand echoed its global counterparts when it indicated any decision to raise interest rates would depend on seeing evidence of second-round inflationary effects when it met earlier this month.

The 25 basis point increase was almost fully accounted for at the July meeting, but prospects for action much sooner in May could rise if Tuesday’s quarterly CPI readings come in above expectations.