So, there are two things to consider today…

First, at Fed Chairman Kevin Warsh’s hearing, there were some things he said today that we will no doubt return to over the coming weeks (and indeed months once he’s finally confirmed). But there is one thing that really stood out. He’s gone on record as not liking the idea of forward guidance, and he said it again today. We sympathize with that, but mostly because we think forward guidance has been overused. When used sparingly, it can be very powerful. As we all appreciate, this has not been the case with the Fed in recent years.

But here’s the thing. Isn’t it using forward steering now? He goes on to highlight that AI will allow the Fed to lower interest rates, as it will lead to lower inflation. Leaving that aside, we believe the timing of this impact is longer than his comments suggest, as the simple act of saying you will cut the price for reason “x” is actually forward guidance. We will have more to say about Warsh in the coming weeks and months.

Okay now on to the consumer. Where does the consumer stand right now? We have data through March, and for now, consumers are doing well in the wake of the Iranian conflict. Gas prices have risen, inflation fatigue is real, and sentiment has fallen as inflation expectations rise in the wake of the conflict. Despite all this, hard data still indicates resilience in consumer spending, at least for now.

Controlled retail sales (excluding gas, autos, and building materials) were strong during March, and also remember that with commodity prices close to stabilizing in March, this nominal strength is not an inflation story.

Consumers are still spending, in part because larger tax refunds offset the initial hit from higher gasoline prices. Refunds are currently up over $40 billion over last year, which represents a 17% increase from the previous year (and very close to our forecast of around 18%). The total number of refunds sent has risen to 3 million more compared to the same time last year. So it will be difficult to ignore this reality, especially when it comes to the state of spending today.

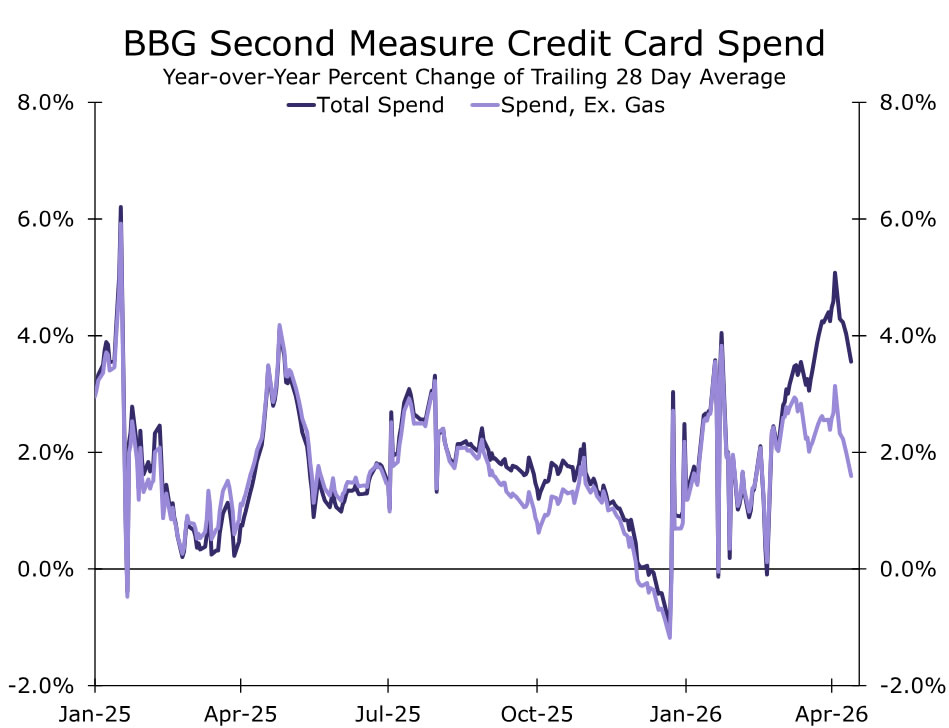

And also remember that the recovery story was an important part of our narrative that growth would look strong this year before the war. For now, public finances remain a tailwind. Credit card spending through mid-April (chart below) indicates a strong spending pace. Just keep in mind that the longer this war lasts and energy prices remain high, the more shock absorbers public finances will become.