The dollar’s broader weakness reasserted itself last week, even as it managed a modest late rebound against the euro. However, across the board, the dollar remains under pressure, as momentum and underlying sentiment point to further declines ahead. Technically and fundamentally, the dollar is now skating on thin ice, as recent price action suggests that the near-term recovery has already come to an end.

This weakness is not due to a single catalyst, but rather to the convergence of forces that are reshaping global markets. Strong risk sentiment has reduced demand for safe haven assets. At the same time, changing central bank dynamics are eroding the dollar’s advantage. In addition, the sharp and unexpected reversal in the Japanese yen acted as a powerful catalyst, accelerating the repositioning process and amplifying the downward pressure on the greenback.

Taken together – stock market strength, policy divergence, and yen intervention – they create a powerful combination. What stands out is not only the presence of these factors, but also their harmony.

AI-led profit surge pushes risks to record highs

Risk appetite was the dominant force in the markets last week US stocks extend their rise to new highs. The S&P 500 and NASDAQ finished the week strong, capping what turned out to be their best monthly performance since 2020. Even the more cyclical Dow Jones posted its strongest gains since November 2024, underscoring the breadth of the move.

The rise was driven by a strong earnings season that decisively beat expectations. Analysts entered the quarter concerned that higher interest rates and higher energy costs would pressure corporate margins. Instead, the results showed that companies were able to maintain their pricing power and manage costs effectively, strengthening confidence in the resilience of the US economy.

Technology stocks, especially those related to artificial intelligence, remained at the heart of the advance. Alphabet and Microsoft delivered strong results, highlighting that heavy investments in AI are now translating into tangible revenue growth. Cloud and enterprise services showed particularly strong momentum, confirming that the topic of AI is evolving beyond early-stage infrastructure spending to real-world implementation and monetization.

And perhaps most importantly, this Stocks continued to be strong despite ongoing geopolitical tensions. Markets largely ignored the risks surrounding the conflict in the Middle East, as traders appeared increasingly insensitive to the headlines. Instead, the focus remained firmly on growth prospects and earnings momentum. As long as this dynamic continues, risk appetite is likely to remain high, continuing to pressure the dollar and shaping the broader market direction.

Technically, the long-term uptrend in stocks remains firmly in place, with both the S&P 500 and NASDAQ maintaining strong bullish structures. The recent breakout to record levels reinforces the view that the current uptrend has not yet been exhausted, especially since pullbacks remain shallow and well supported.

to Standard & Poor’s 500The near-term outlook remains bullish as long as support remains at 7046.55. The next upside target is a 61.8% forecast of 4835.04 to 6902.34 from 6316.91 at 7605.63.

A similar structure is seen in Nasdaq. As long as the support at 24199.00 holds, the current uptrend is expected to extend towards the 61.8% forecast of 14784.03 to 24019.99 from 20690.25 at 26398.07.

Tightening convergence outside the Fed is weighing on the dollar

The main driver behind the dollar’s weakness last week was the changing outlook for global monetary policy.

to Federal ReserveThe decision to keep interest rates at 3.50%-3.75% was widely expected, but the internal dynamics were far from calm. The meeting had four opponents – the highest since 1992 – with three regional chairs (Hamack, Kashkari and Logan) opposing the inclusion of mitigation bias in the statement. This reflects growing concern within the Committee that inflation risks remain high and that the policy may not yet be sufficiently restrictive.

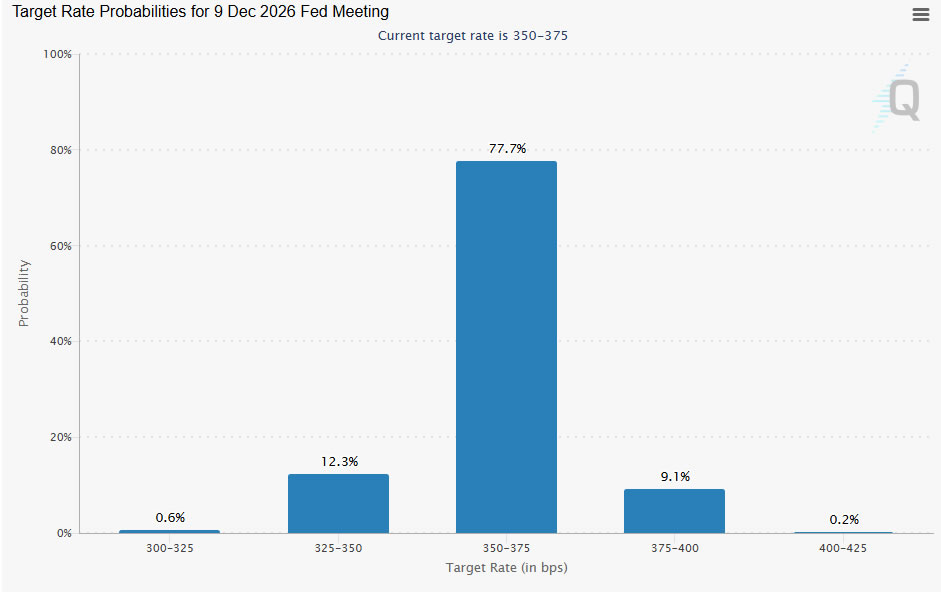

Despite this tough opposition, the broader message from the Fed remains one of patience. Although interest rates are somewhat restricted at 3.50-3.75%, there is no urgent need for further tightening. Market prices reflect this balance, with about a 77% probability that prices will remain unchanged until the end of the year. Expectations for interest rate cuts fell sharply to around 12%. The Fed is no longer the most hawkish player, but it is also unwilling to ease monetary policy.

the Bank of EnglandIn contrast, the bank is leaning more clearly towards tightening monetary policy. The April 30 decision to keep interest rates at 3.75% came by 8 votes to 1, with chief economist Hugh Bell opposing in favor of an immediate 25 basis point hike. His position highlights growing concerns about persistent inflation, especially resulting from energy-related cost pressures and the risks of second-round effects.

The markets took this signal seriously. The June rate hike rate stabilized at around 60%, after jumping to 70% immediately after the interest rate announcement. The total tightening forecast is around 65 basis points for this year. Even as the Bank of England acknowledges fragile growth conditions, the bias is shifting towards further tightening.

the European Central Bank He’s also getting close to work. While he kept the deposit rate at 2.00%, President Christine Lagarde’s neutral tone was quickly overshadowed by reports that policymakers are preparing to raise interest rates in June if energy prices remain high. The ECB is seen as “waiting patiently” rather than taking its stand.

This shift is driven by inflation dynamics. The jump in April’s CPI to 3.0%, combined with Lagarde’s admission that the eurozone is moving toward a “negative scenario,” has markets pricing in a 90% probability of a June rate hike. The forecast now extends to three 25 basis point increases by the end of 2026, targeting a final rate of 2.75%.

Perhaps the most dramatic transformation is occurring in Japan. the Bank of JapanThe 6-3 vote on April 28 was a major departure from its historically unified position. The three dissenters – Nakagawa, Takata and Tamura – have pushed for an immediate rate hike to 1.00%, arguing that the central bank risks falling behind the curve as inflationary pressures build.

This internal division was reinforced by the sharp upward revision of inflation expectations for 2026 to 2.8%, well above the traditional target range. Market expectations have quickly adjusted, with the probability of a June rate hike rising to around 74%. July remains a fallback option, especially if geopolitical risks intensify and threaten growth.

Together, these developments highlight a clear convergence in the tightening of global policies. While the Fed remains in a waiting mode, others are catching up or even surpassing it in terms of hawkish bias. This narrowing of interest rate spreads is a key structural driver of dollar weakness, and unless the Fed reasserts its leadership, pressure on the greenback is likely to continue.

An intervention shock causes the yen to rise

The most dramatic development in the currency markets last week was the sudden and strong reversal in the Japanese yen. After the USD/JPY pair broke the 160-point “red line,” Japanese authorities drew a clear line in the sand. What followed was a sharp and violent move that caught the markets by surprise and led to a widespread reassessment of trading positions.

It appears that the intervention was decisive. Estimates indicate this More than US$30 billion has been deployed During April 30 and May 1, with reports from the Nikkei citing Bank of Japan data indicating nearly 5 trillion Japanese yen (32 billion US dollars) in yen purchases. The size of this step confirms the authorities’ determination to stop speculative excesses and restore stability to the currency.

The impact was immediate and far-reaching. The yen rose nearly 2.2%, pushing USD/JPY lower towards the 156 area. More importantly, the move led to a rapid unwinding of crowded buy-carry trades, amplifying the effect far beyond the yen itself. The dollar, already under pressure from other factors, faced additional downside as positions were liquidated across the board.

This episode wasn’t just about price action, it was a warning shot. This intervention effectively reintroduced two-way risks into what had become a one-sided market. Traders who were comfortable with the USD/JPY push higher were forced to reevaluate, and opportunistic buying of the yen emerged as markets began to test how willing the authorities were to defend the currency.

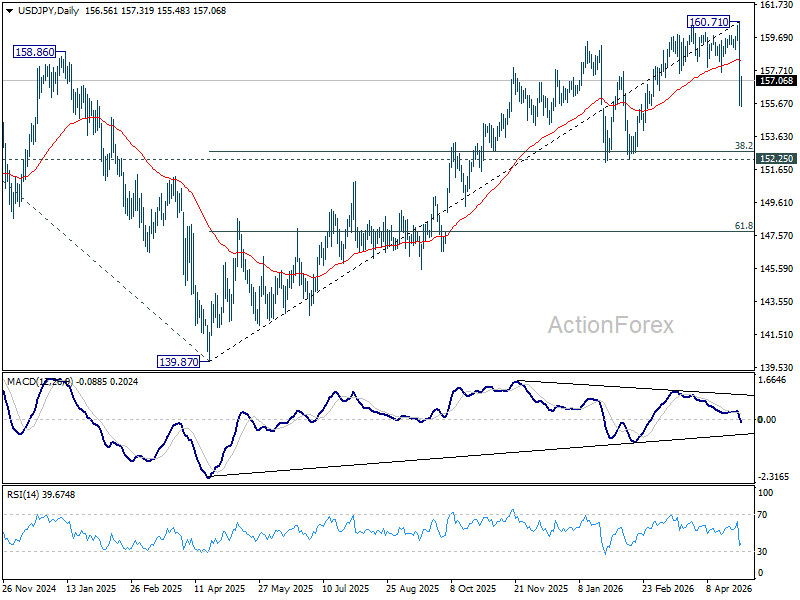

Technically, the sharp decline from 160.71 indicates that a medium-term top should have been formed, reinforced by bearish divergence on the D MACD. However, the subsequent decline is now seen as a correction to the broader uptrend from 139.87, rather than a complete reversal – at least for now.

Near-term risks point to a deeper pullback towards the 152.25-152.74 cluster support area (38.2% retracement from 139.87 to 160.71 at 152.74). . Strong support is expected in this area, which should contain the downside and allow for a bounce. in the meantime, USD/JPY is likely to consolidate within a broad range of 152-160With future direction depending on policy developments and global risk dynamics.

The bearish slope of the DXY remains intact to retest the bottom at 95.55

Last week’s rebound in the dollar index did little to change the broader bearish outlook. The retracement from 95.55 should be completed at 100.64, less than the 38.2% retracement from 110.17 to 95.55 at 101.13. This failure to sustain gains reinforces the view that the rally was corrective and not the start of a new trend.

Rejection at key technical levels adds weight to this interpretation. Notably, the DXY has returned below the 101.13 Fibonacci resistance and the 55 W EMA, currently located near 99.49. These levels have acted as a constant ceiling, keeping the medium-term bias tilted to the downside and indicating that sellers are still in control.

In the near term, focus shifts to 97.63 price support. A decisive break below this level will confirm the resumption of the decline from 100.64 and open the way for a retest of the 95.55 low.

However, the downward momentum has not fully accelerated yet. While this bias remains bearish, the current pace of decline does not yet indicate an imminent collapse. Markets may need additional catalysts – such as further policy divergence or continued risk flows – to trigger a more decisive decline through 95.55.

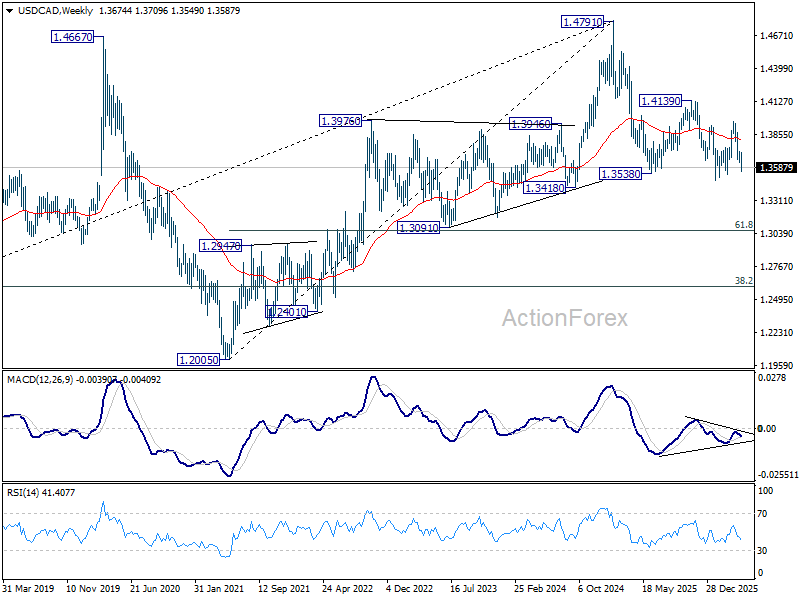

Weekly forecast for the USD/CAD pair

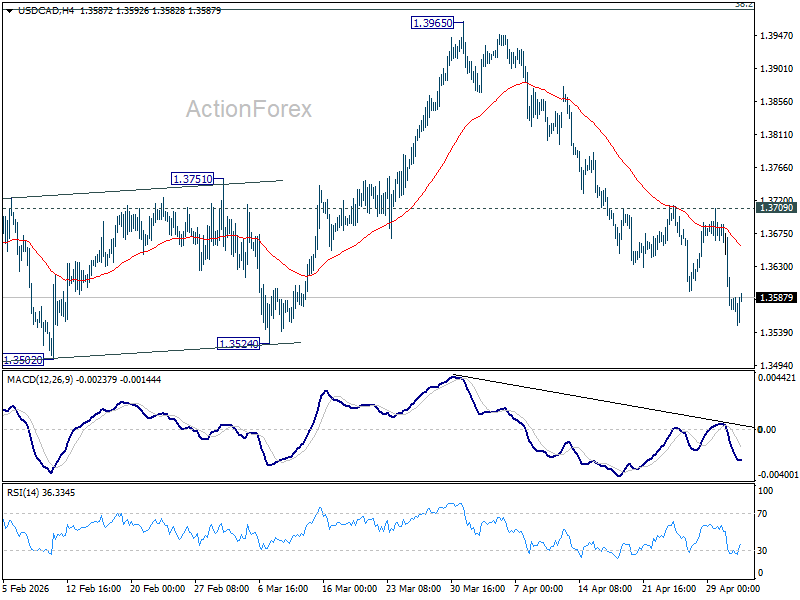

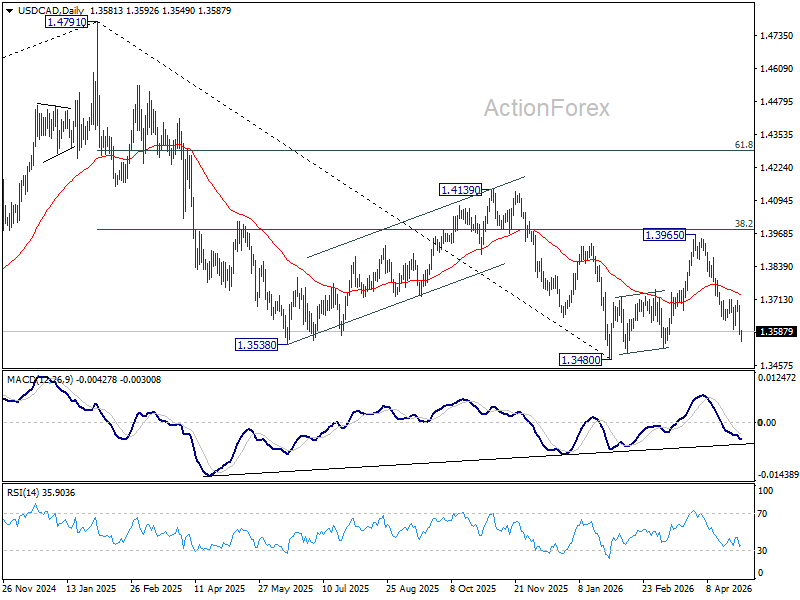

The USD/CAD pair continued to fall from 1.3965 last week after a brief rebound. Initial bias remains to the downside this week for a retest of the low at 1.3480. A decisive break there will resume the entire downtrend from 1.4791. For now, the risk will remain on the downside as long as resistance at 1.3709 holds, in case of a recovery.

In the bigger picture, price action from 1.4791 is seen as a corrective pattern for the entire uptrend from 1.2005 (2021 low). A deeper decline can be seen, as the pattern extends, to the 61.8% retracement levels from 1.2005 to 1.4791 at 1.3069. However, a decisive break of the 38.2% retracement level from 1.4791 to 1.3480 at 1.3981 will indicate that the three-wave correction down to 1.3480 has already been completed.

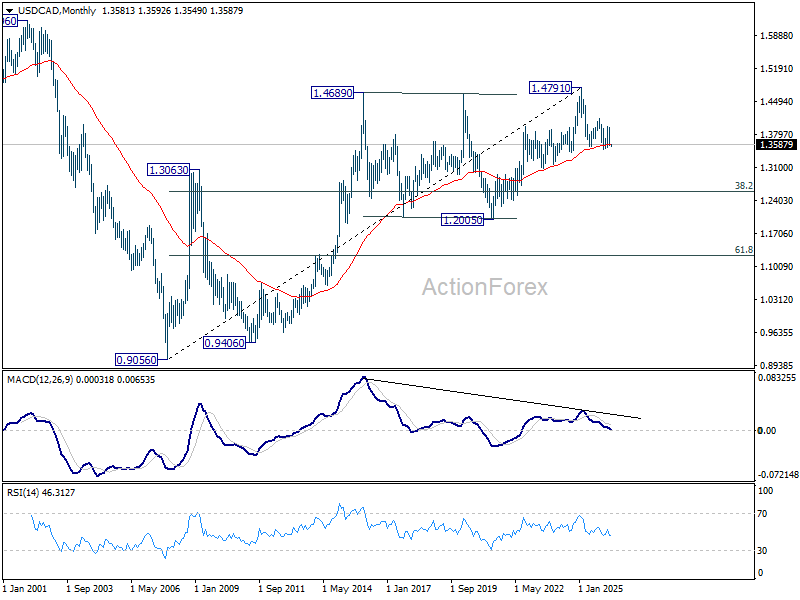

In the longer term, the high of the 55M MA (now at 1.3581) remains in place. Therefore, the uptrend from 0.9056 (2007 low) may still be in progress. However, given the case of a bearish M MACD divergence, sustained trading below the 55 EMA will argue that the uptrend has been completed in five waves up to 1.4791, and turns the medium-term outlook bearish for a correction to the 38.2% retracement from 0.9056 to 1.4791 at 1.2600.