Canada – Quiet week before inflation test

Canadian financial markets were relatively stable this week, although rising bond yields signaled a modest rise in interest rate expectations. In the absence of key domestic data, markets were shaped by global forces, as oil price volatility and continued inflation uncertainty pushed Canadian government yields higher across the curve. The TSX rose during the week, while demand for the US dollar strengthened, causing the Canadian dollar to fall by three-tenths of a cent as continued volatility directed flows towards the US dollar.

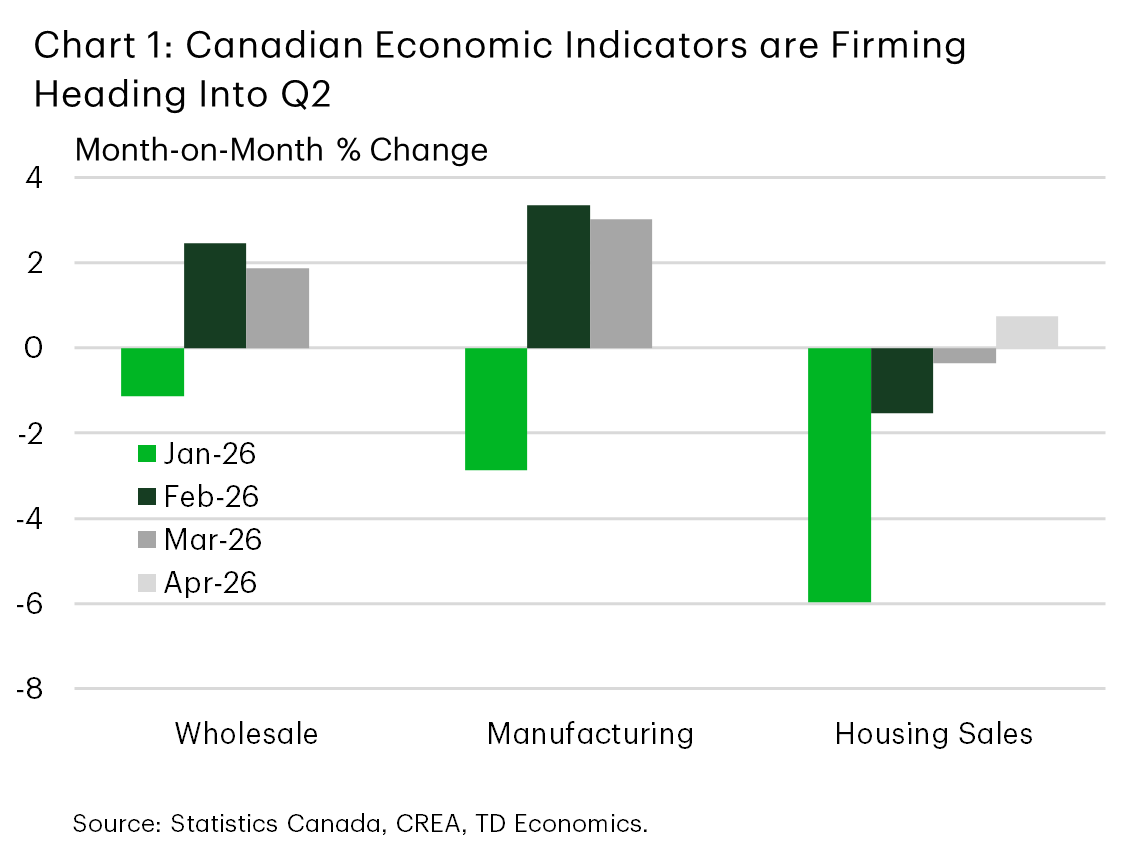

This week’s data provided an increasing read on economic conditions (Chart 1). Wholesale trade and manufacturing sales for March bolstered the trajectory of goods sector activity, with early indicators pointing to some stabilization after a weak start to the year. While neither release is likely to materially change the broader growth backdrop, they will help improve tracking of first-quarter GDP, which indicates modest growth.

Meanwhile, in the housing market, April home sales rose, consistent with our view that activity should see a rebound in the second quarter. Housing starts data also exceeded consensus expectations. Looking back, we still expect only a gradual improvement in housing conditions in 2026, as higher borrowing costs, affordability issues, and slower population growth continue to dampen demand and construction.

In a week of little economic data, a summary of the Bank of Canada’s deliberations reinforced uncertainty about the policy outlook. While higher energy prices are expected to lift inflation soon, the Governing Council saw room to be patient and keep interest rates steady as the economy develops as expected. They stressed that forecasts still depend heavily on incoming data, with risks in both directions. Continued strength in oil prices could expand inflationary pressures and necessitate policy tightening, while weak trade-related growth or external shocks may necessitate easing of restrictions, given uncertainty about remaining slack in the economy.

Along with the monetary policy update, reports of ongoing negotiations between Ottawa and Alberta over industrial carbon pricing and a potential West Coast pipeline indicate a shift toward aligning climate policy with major project development. Such efforts could help improve the visibility of investment in Canada’s energy sector, with implications for long-term growth capacity.

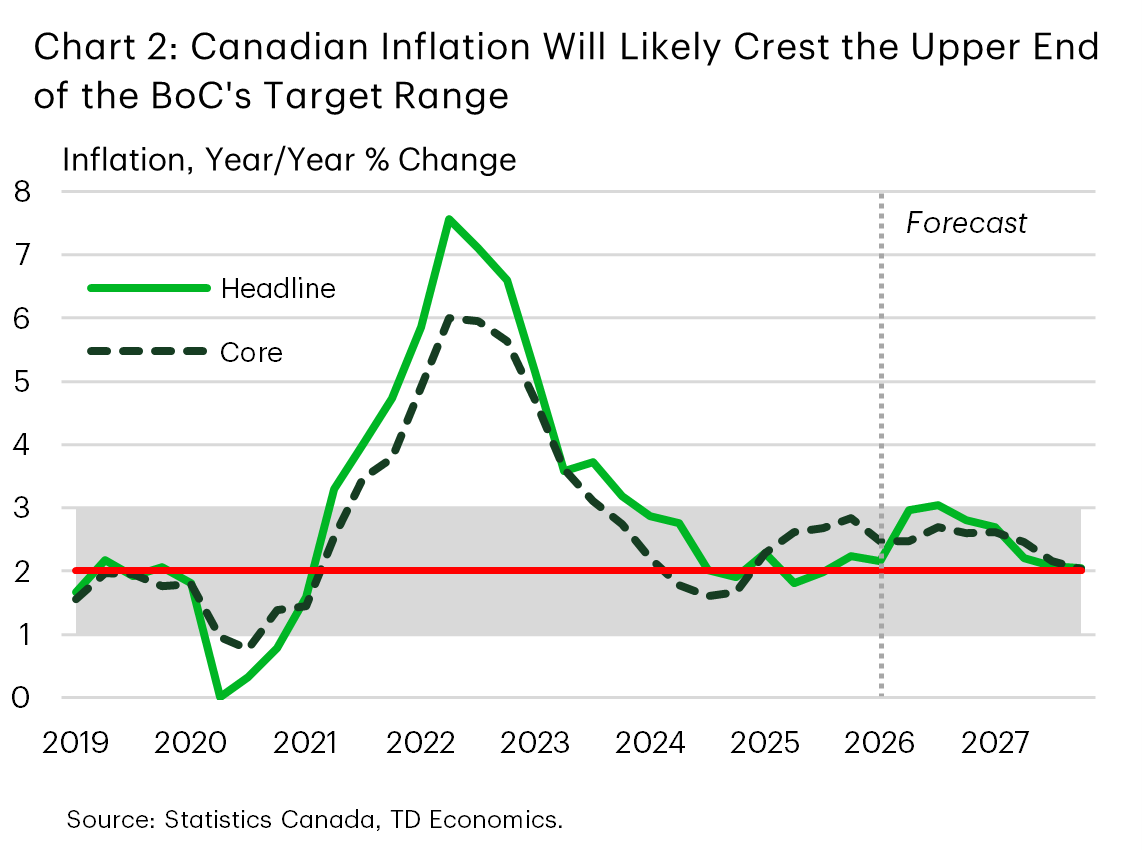

This week’s developments reinforce a familiar theme: an economy that is growing modestly but facing significant uncertainty, and a central bank firmly in a wait-and-see mode. Attention now turns to next week’s April inflation (CPI) release, where inflation is expected to rise due to the effects of the energy base. We expect headline inflation to peak at around 3% later this year before falling back towards target (Chart 2). The key question will be whether price pressures will remain under control or will they begin to expand more meaningfully to underlying components.

United States – Changing of the Guard

The changing of the guard at the Fed was formalized this week, with the Senate confirming Kevin Warsh as Powell’s successor on Wednesday. This means that Jerome Powell’s eight-year term as president ended on Friday. Warsh takes over at a time when inflation pressures are rising sharply on the back of rising global energy prices. Details about a potential resolution to the conflict in Iran remained elusive this week, sending WTI prices up 9%. Stock markets were virtually unchanged during the week, with the S&P 500 rising 0.2%, with US Treasury yields rising about 20 basis points, reflecting stronger inflation readings.

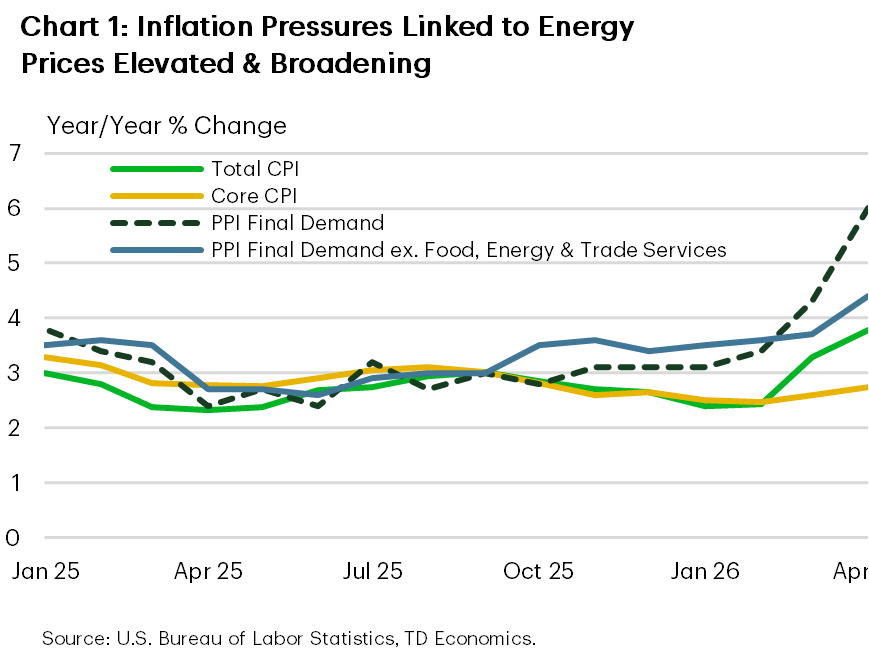

In terms of economic data releases, April inflation data was the biggest news. The headline CPI reached a three-year high of 3.8% year-on-year (y/y), on the back of rising energy prices (Chart 1). Excluding energy and food products, core CPI accelerated for the second straight month to 2.7% year-on-year, partly due to the impact of energy prices on categories such as airline ticket prices. The report missed a broad shift to non-energy categories, but with energy prices rising through early May, subsequent reports may be less dire, especially if a resolution is not found in the near term.

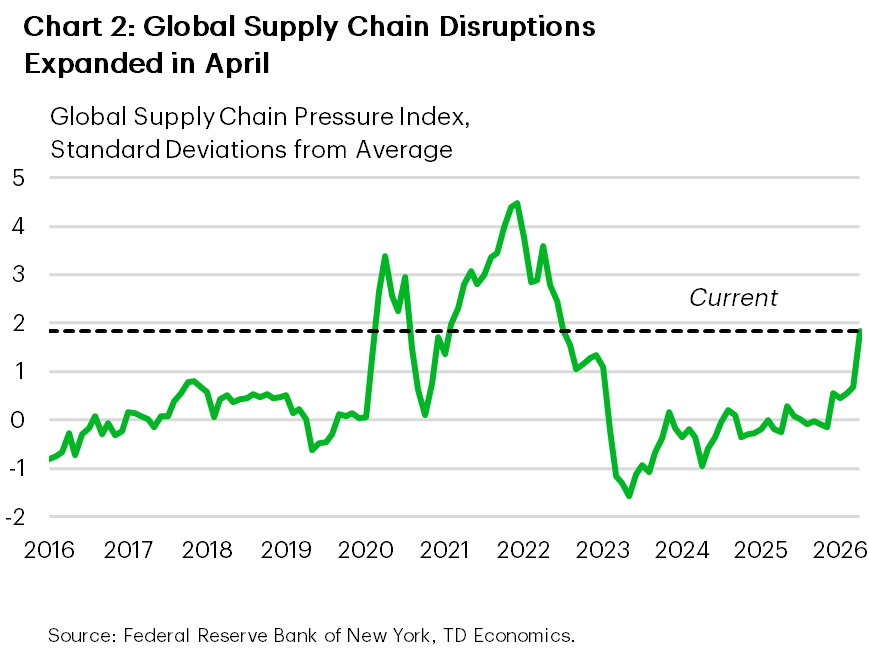

Upstream, the impact of higher energy prices was similarly evident for producers in April, with the Producer Price Index rising 6% year-on-year. Selling price pressures have not risen this high since late 2022, as global supply chain disruptions began to converge to those seen during the initial period of the pandemic (Chart 2). The impacts of these developments on businesses and consumers will be closely monitored by the Federal Reserve.

To that end, the April retail sales report provided an early glimpse into consumer health. It showed a strong gain of 0.5% month-on-month in nominal terms, but after adjusting for inflation, sales fell by 0.2%. This likely partly reflects a similar contraction in real earnings during the month, which, if sustained, will continue to weigh on consumption going forward. A resolution to the Iranian conflict in the near term would help alleviate some of these pressures, although the effects are likely to be gradual as supply disruptions take a long time to completely disappear. Taken together, these cross-currents make near-term policy expectations highly dependent on incoming inflation data.

Against this backdrop, Fed officials in public statements this week cited concerns about inflation reports. Several officials, including Chicago Fed President Goolsbee and Boston Fed President Collins, have indicated that tighter financial conditions may be needed to suppress emerging inflationary pressures. The balance of opinion among officials confirmed that a neutral stance would be appropriate in the near term to allow time to evaluate the data received. As of writing, financial market prices for a rate hike by the end of the year have risen to 40%.