short

- Bank of America reiterates “buy” on Alphabet with a target of $430 — a 10.9% upside from $387.66.

- Analysts cite AI Overviews at 2.5 billion users, AI Mode at 1 billion, and Gemini doubling from 400 million to 900 million monthly active users in the year.

- The report has some nuances: The stock is down 2% on I/O day, free cash flow is expected to decline to roughly $29 billion in 2026 due to increased capex, and Bank of America publicly questions whether AI query monetization will “materially outpace” traditional search.

Google had great I/O. Then its stock fell 2%. Bank of America still says buy.

Bank of America analysts Justin Post and Nitin Bansal published their note on May 20 maintaining a “buy” rating and a $430 price target for Alphabet — a 10.9% upside from its current price of $387.66. Their verdict: “Google is no longer playing catch-up, as search advertising and agents have demonstrated a wave of groundbreaking product innovations.”

The revolutionary case runs on three user metrics from Google’s I/O disclosures. AI Overview — AI summaries at the top of search results — now has 2.5 billion users. AI Mode, the conversational layer of search, has 1 billion people and is doubling every three months. Gemini’s monthly active users have risen from 400 million a year ago to 900 million today.

The BofA read that the ramp “indicates that Google has successfully moved search users toward native AI experiences, reducing the risk of competitive disruption.”

The bank is honest about what’s yet to be solved, although whether monetizing AI queries can “fundamentally go beyond search” is an open question. More complex queries mean more ad surface area in theory. The data has not yet confirmed this.

Five bets on the table

BofA organized its I/O analysis around five product paths.

On models: Gemini Omni Gemini integrates with video and media creation tools — what the bank calls the company’s “push toward world-class AI systems capable of understanding and interacting across multimedia environments.” Gemini 3.5 Flash offers “significantly faster inference speeds and lower costs compared to competing frontier models,” a price and performance advantage that matters to the cloud as much as it wins over consumer applications.

When searching: Gemini AI is now integrated directly into search alongside new “search agents” – permanent background agents that continuously monitor finances, shopping, travel and sports on users’ behalf. The redesigned Gemini app adds dynamic layouts, smooth animations, and AI-generated visuals.

On agents: Gemini Spark It is a 24/7 cloud-based personal agent that handles Gmail, Docs, Sheets, Calendar, Chrome, and third-party services without requiring any user input. It’s Google’s response to the boom in proxy tools like Hermes and OpenClaw.

BofA argues that Google’s “captive audience and speed of deployment” gives it a head start on “locking in the ecosystem and behavioral assumptions around agent workflows.”

In commerce: Universal Cart allows users to save, track, and purchase across retailers including Target and Walmart. Amazon is not in the cart. The hotel reservation is “likely several months away,” according to Bank of America, with some negotiations ongoing.

On hardware: Two categories of Gemini-powered glasses — the first audio models expected this fall, and the display-based glasses previewed last year. The first audio line is likely “in direct competition with Meta’s Ray-Ban.” Camera specifications and battery life have not been announced, which BofA reads because Google still has “work to do before release.”

Yes, but…

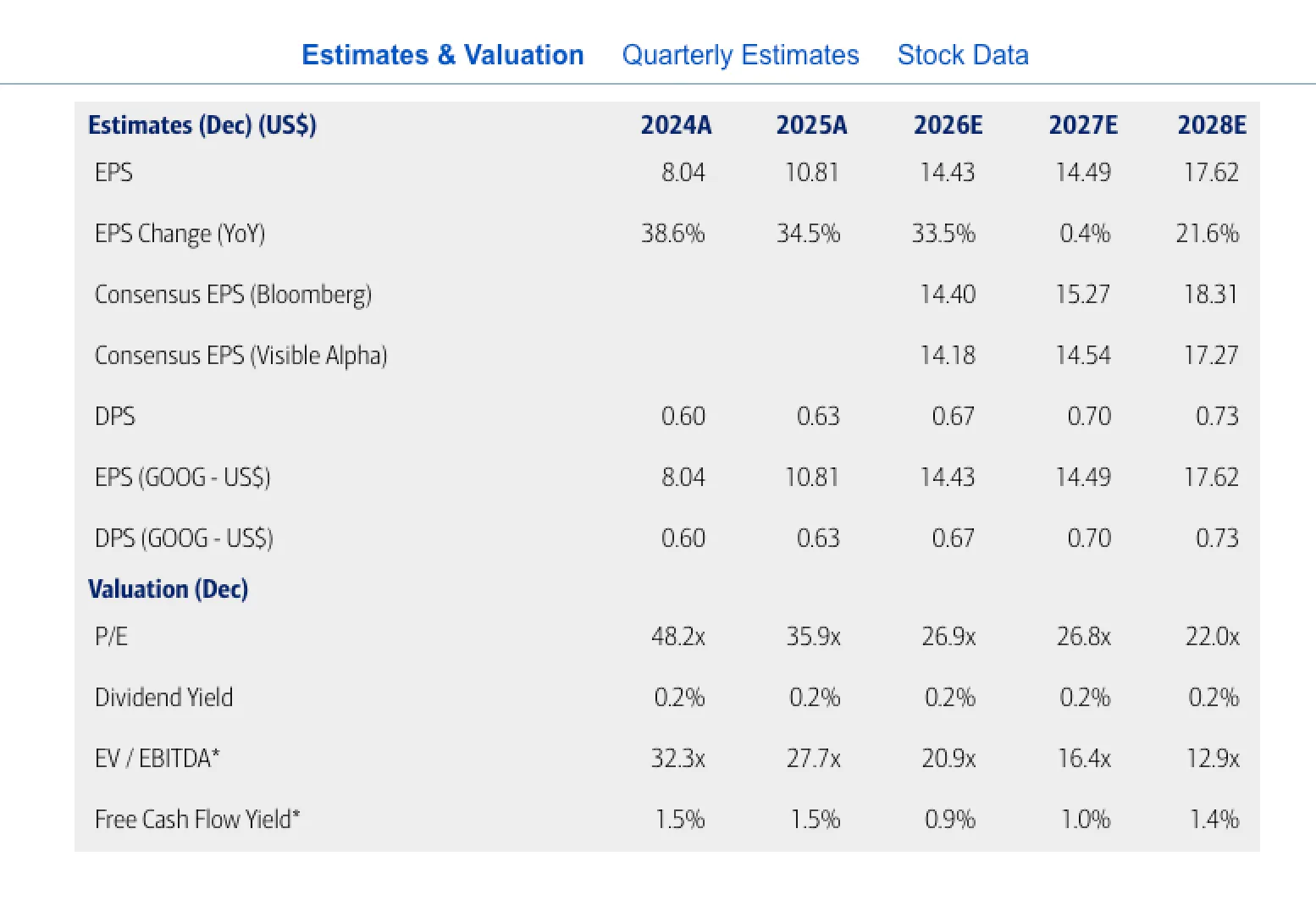

However, it’s not all roses for Google. Free cash flow is expected to decline from $73.3 billion in 2025 to $44.1 billion in 2026 with capital spending rising from $91.4 billion to $186.6 billion.

EPS stats tell a similar story: Bank of America is at $14.43 per share in 2026, barely moving to $14.49 in 2027 before recovering to $17.62 in 2028. And the spending is happening now. Returns are the story of 2028.

In terms of valuation, Alphabet is still significantly overvalued. BofA says the premium is “justified and could be sustained as confidence in Alphabet’s AI positioning improves.”

The report also points to four clear downside risks: search traffic shifting to AI competitors, LLM integration into search taking longer than expected, compliance pressure with the EU Digital Markets Act, and higher capital expenditures putting pressure on free cash flow.

BofA says Google shares could reach $430 because it values the company at 28 times its expected 2027 earnings, plus Google’s available cash. Alphabet’s Q3 and Q4 earnings will be the first real test of whether AI Mode’s 1 billion users translates into revenue growth that holds this steady.

Daily debriefing Newsletter

Start each day with the latest news, plus original features, podcasts, videos and more.