Conflict in the Middle East and the closure of the Strait of Hormuz have sent sulfuric acid prices soaring, leading to a sharp increase in the costs of producing lithium, nickel and other important metals essential to the energy transition.

Benchmark Mineral Intelligence said sulfur prices have risen by more than 50% since the start of the war in Iran, while sulfuric acid prices have doubled in some regions, disrupting supply chains for battery metals and forcing some refineries to reduce production amid a shortage of physical sulfur supplies.

“Sulfuric acid is a vital raw material for many important minerals, and the disruption to the sulfur market due to the ongoing conflict in the Middle East has had knock-on effects on key markets,” said Will Talbot, Director of Raw Materials Research at Benchmark. “The notable risk is that the most important metals companies reduce production or even close operations entirely.”

Lithium pressure

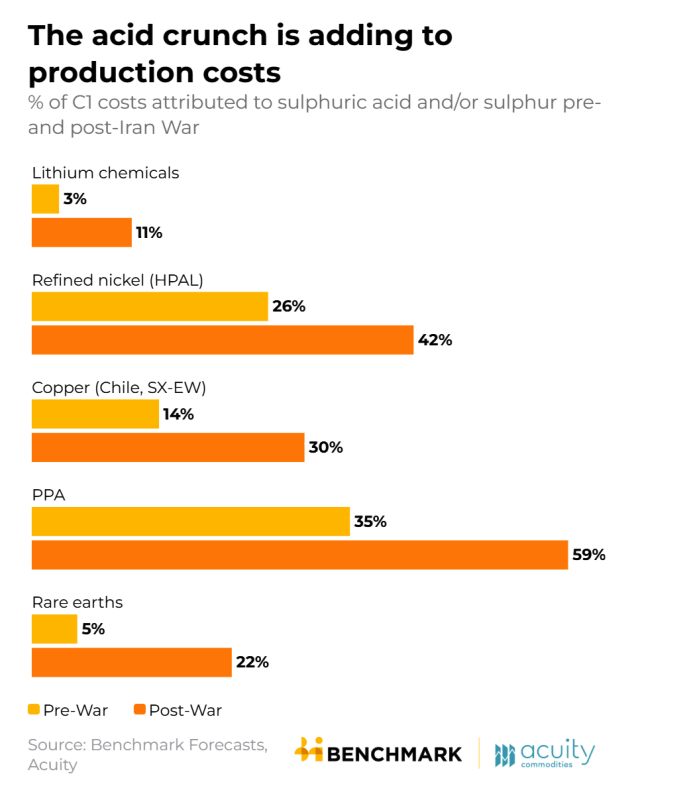

The supply shock is reshaping the economics of battery material production. Sulfuric acid previously represented about 3% of the cost of producing lithium chemicals from hard rock sources, but now represents 11%, surpassing energy as the largest single component of C1 cost, Benchmark said. Sulfuric acid now contributes 22% of total lithium conversion costs from hard rock, and has become the “single most volatile and material input” in lithium processing, the consultancy’s own report said.

Nickel production via high-pressure acid leaching has also become highly exposed to sulfur markets. Sulfur now accounts for 42% of HPAL nickel costs, compared to 26% before the conflict, Benchmark said. Indonesia, the world’s largest nickel producer, obtained 76% of its sulfur imports from the Middle East last year, while producing one ton of nickel through HPAL processing requires more than 10 tons of sulfur.

Supply risk

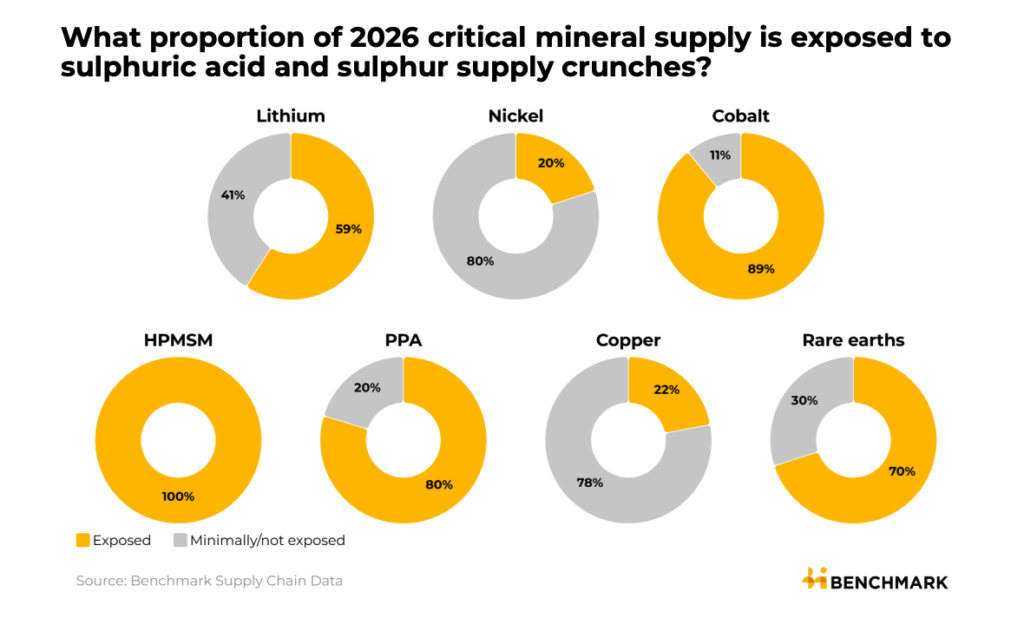

The report warned that physical availability, not just pricing, has become the biggest risk in the industry because at least half of the global seaborne sulfur trade passes through the Strait of Hormuz. More than half of the global production of lithium, cobalt, rare earths and purified phosphoric acid expected in 2026 is exposed to sulfur and sulfuric acid disturbances, according to Benchmark. High purity manganese sulfate monohydrate, used in electric vehicle batteries, relies entirely on supplies of sulfuric acid.

China’s informal restrictions on sulfuric acid exports have exacerbated pressure on refineries outside the country. Spot prices for acid in Indonesia and Chile have risen to more than $380 and $440 a tonne, respectively, as transformers scramble for alternative supplies, Benchmark said. Prices for lithium carbonate used in batteries in China have already risen by about 65% this year in dollar terms.

Wider implications

Copper producers are feeling the impact unevenly. While the solvent extraction and electrowinning processes that account for 22% of global mined copper production require large quantities of acids, copper smelters benefit because sulfuric acid is a profitable byproduct of the smelting process. Processing and refining fees for copper concentrate have fallen sharply since the strikes on Iran as higher acid prices improve smelters’ economics, Benchmark said.

The supply squeeze highlights how geopolitical conflict is increasingly colliding with the supply chains of the energy transition. Countries with domestic sulfur and acid production capacity, such as the United States, are likely to be more isolated than import-dependent jurisdictions including Australia, Benchmark said. Even if the Strait of Hormuz reopens quickly, the company warned that the damaged oil refining infrastructure in the Gulf may take a long time and significant investments to recover, prolonging pressure on important global metals markets.

Source link