Notable Canadians

- Markets swung in hopes of reaching a truce in the Middle East, but expectations remain fragile.

- Canada’s economy has faltered over the past two quarters, with weak domestic demand and erratic investment indicating weak momentum.

- The upcoming CUSMA review is now central, as Canada looks to link greater trade clarity to an energy-led investment strategy.

Highlights in the United States

- Renewed hopes for an extension of the US-Iran ceasefire sent WTI prices falling 9% this week to $88 per barrel.

- Consumer spending remained resilient in April, amid rising inflationary pressures and dwindling household savings.

- More Fed officials are joining the increasingly hawkish chorus, with Fed futures pricing in a 60% rate hike by the end of the year.

Canada – Canada’s economy falters ahead of trade negotiations

Hopes for a peace agreement to end the conflict between Iran and the United States and open the Strait of Hormuz dominated markets this week. Although optimism about a possible 60-day truce has pushed oil prices down sharply (they are down about 9% compared to late last week), volatility remains high. Markets continue to respond quickly to changing news headlines, underscoring the fragility of expectations. For Canada, this volatility comes at a time when access to US markets remains an open issue and continues to weigh on domestic activity.

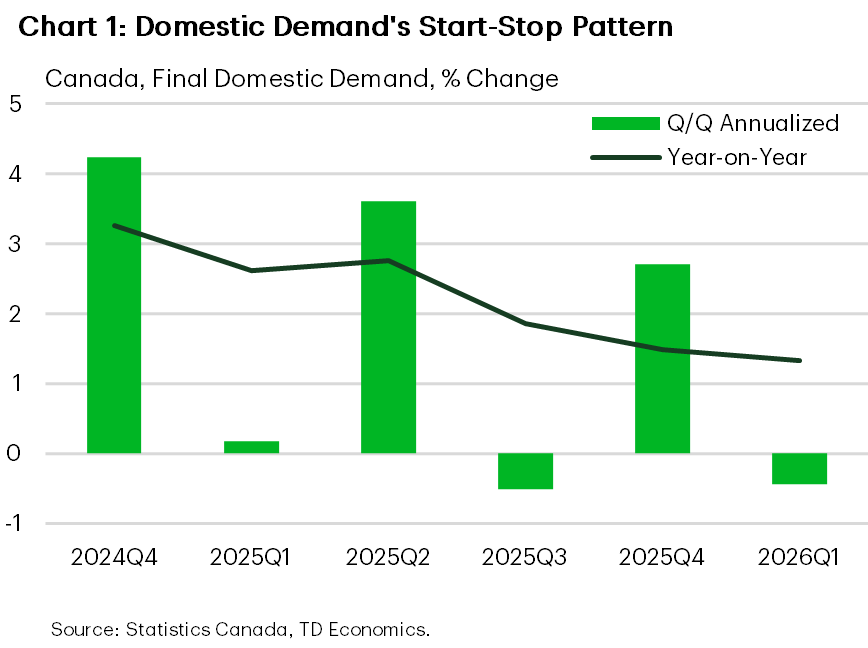

The Q1 GDP report showed that the economy had virtually ground to a halt (-0.1% q/q/q/q), which was lower than expectations. The weakness was widespread. Strong import growth brought the top figure down, but final domestic demand fell again (-0.4% QoQ), and continues to move forward erratically (Chart 1). Given the volatility, final domestic demand rose 1.3% year-on-year, but this is still below trend, and consistent with an economy operating below capacity.

Household spending grew 1.5% quarter-on-quarter, supported by services, but momentum eased from the fourth quarter. On the investment side, good growth in machinery, equipment and intellectual property products was offset by another significant contraction in residential investment (-7.9% QoQ) and weak expenditures on engineering structures. Government investment also reversed after gains in late 2025.

Overall, the economy continues to muddle with limited forward momentum. While early Q2 indicators point to some recovery (with GDP rising in April), the broader trend still points to a stagnant economy and weak growth.

Canada’s weak growth performance puts the focus squarely on the upcoming CUSMA review. The economy has operated under a cloud of uncertainty over access to US markets since the first batch of tariffs were announced last year. The three countries are scheduled to notify each other on Monday of the changes they want in the agreement, with discussions to follow. The United States and Mexico have already scheduled formal negotiating rounds. US-Canadian Trade Minister Dominic LeBlanc is expected to travel to Washington next week, but the timelines for the negotiations remain unclear.

For some insight into the negotiations, Prime Minister Mark Carney’s speech in New York this week highlighted Canada’s strategy. He called for a “new partnership” with the United States, while simultaneously setting Canada’s goal of establishing itself as an “energy superpower.”

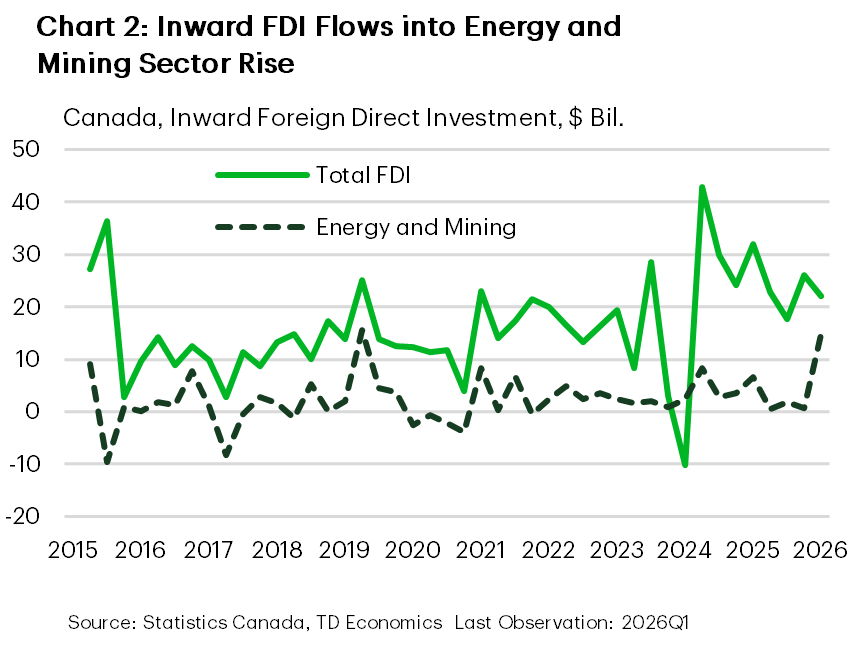

Recent FDI data suggest there may be something to this strategy. Inflows in the first quarter were $22 billion ($4 billion less than in the fourth quarter), and investments in the energy and mining sector reached $14.7 billion in the quarter (Chart 2). Although this data is volatile, it is consistent with Canada’s strategy to leverage its resource base and attract long-term capital.

The Canadian economy continues to flounder under a cloud of trade uncertainty. The hope is that clarity and stability in the trade relationship with the United States will emerge in the coming months. Increased economic certainty, combined with a push to attract global capital to invest in Canada, could lay the foundation for productivity-led economic growth.

United States – Mechanism for Reaching a Deal

It has been three months since the United States and Israel launched the initial attack on Iran. Hopes for a long-term peace solution rose this week following President Trump’s comments that the peace deal had been “largely negotiated.” Oil prices fell sharply on this news, although renewed attacks from both sides by mid-week briefly dampened the optimism. But by Thursday evening, news lines were reporting that the two sides had reached agreement on a 60-day memorandum of understanding to extend the ceasefire, pending approval by President Trump. Oil prices fell by 9% over the week, and the price of WTI currently stands at $88 per barrel. Meanwhile, economic data released this week boosted a more cautious but still resilient consumer amid renewed inflationary pressures. The S&P 500 rose 1.3% on the week, while the 10-year Treasury yield fell 12 basis points and currently stands at 4.44%.

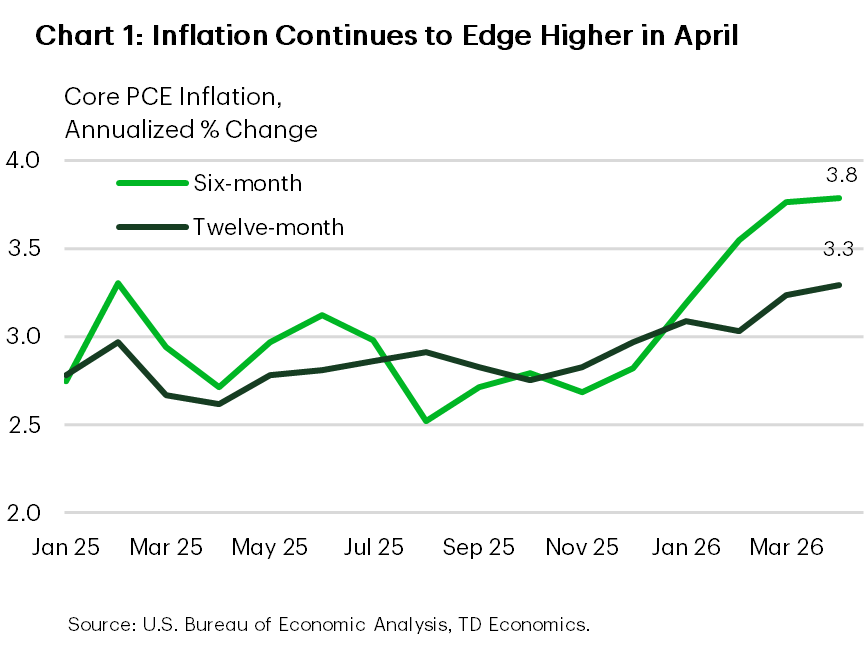

The release of personal income and spending data for April this week provided a new dose of reality about the pain inflicted on American households by the energy shock. PCE inflation rose to a three-year high of 3.8% year-on-year, and is likely to rise to 4% in May coupled with the continued rise in gasoline prices. The picture didn’t look much better once food and energy impacts were removed, with core PCE inflation rising to 3.3%. Three- and six-month measures were hotter, each rising 3.8% (Chart 1).

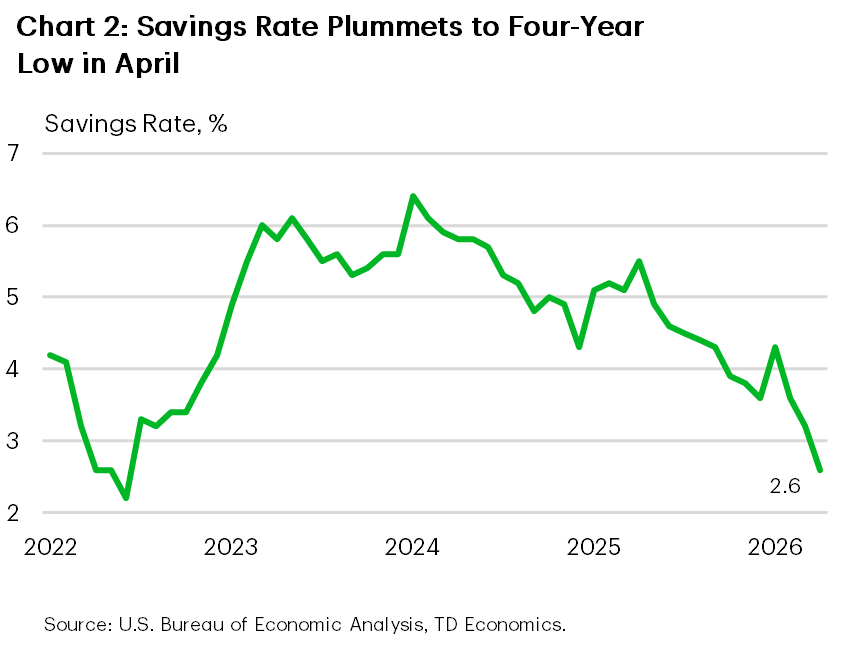

Despite the rise in inflation, the consumer remained reasonably resilient. Nominal spending rose 0.5% month-on-month in April, after a strong 1% increase in March. After accounting for inflation, April’s gains looked less impressive, but were still up 0.1% month-over-month. Hotter inflation is also eroding consumers’ purchasing power, with real disposable income falling for the third month in a row. This has led to households increasingly relying on savings to spend on fuel. But with the savings rate at a four-year low, reserves look increasingly slim.

According to a recent study conducted by the Conference Board, households reported lower spending intentions in the coming months. Fewer households plan to purchase expensive items while two-thirds of consumers plan to reduce overall spending due to higher prices. While polling metrics have been a less reliable indicator of actual spending after the pandemic, we can’t completely ignore the signal. The energy shock has increased pressure on affordability for low- and middle-income households, which did not benefit to the same extent from last year’s gains in housing and stock prices.

There is an increasing risk that affordability pressures will worsen if the energy shock lasts longer. A growing group of Fed officials appear increasingly hawkish amid rising inflationary pressures. Board member Lisa Cook said this week that if the decline in inflation did not resume soon, she would be “prepared to raise interest rates.” Meanwhile, Fed Chairman Kashkari reiterated that fighting inflation is a priority as the labor market now appears to be in good shape. This suggests that next week’s employment report will play second fiddle to the May CPI numbers due on June 10. Fed futures are now priced for a 60% rate hike by the end of the year, but a hotter inflation report could push expectations for a rate hike forward.