Two reports. Forty-eight hours. One question. Has the RBA taken the long walk, or is there a final move still waiting in August? Wednesday’s Australian inflation report and Thursday’s employment data could provide the clearest answer yet. After three consecutive interest rate hikes earlier this year, the Reserve Bank of Australia in June paused at 4.35%. But this stop solved nothing. Inflation is still very high, policymakers are still complacent, and markets are deeply divided on whether the tightening cycle is truly over.

Consumer price index on Wednesday The release will be the first battlefield. Headline inflation is expected to rise from 4.2% y/y to 4.3% y/y, but the real story lies beneath the surface. Oil prices have collapsed since the US-Iran ceasefire, easing pressure on major measures ahead. If tapered average inflation continues to accelerate from 3.4% y/y to 3.6% y/y, it will send an uncomfortable message to the RBA that domestic inflation is proving more stubborn than hoped.

This is exactly the scenario that policymakers fear. Higher core inflation suggests that service prices and broader domestic cost pressures are offsetting the mitigation of lower oil prices. Rather than validating the June pause, it may strengthen the case for another rate hike before inflation expectations deepen.

Then he comes Thursday’s jobs report. Markets expect employment to grow by 30K after April’s unexpected loss of -18.6K jobs, while unemployment is expected to fall from 4.5% to 4.4%. If the labor market rebounds as expected, the message will be hard to ignore: inflation is rising again while employment remains resilient despite interest rates remaining at their highest levels in years.

And this combination of steady inflation and strong jobs is exactly what should keep expectations of an August rate hike alive. It may not be enough to launch the AUD/USD on a sustained rally against the broadly stronger US dollar, but it may be enough to keep the pair comfortably above 0.7000 and force traders to price in another move from the RBA.

The opposite result would be much more dramatic. If employment contracts again or unemployment rises above 4.5%, markets may begin to treat the June pause as the end of the tightening cycle. The RBA will not necessarily be over, but traders will likely be in for a long pause. In this scenario, AUD/USD may quickly lose its grip on the 0.7000 level.

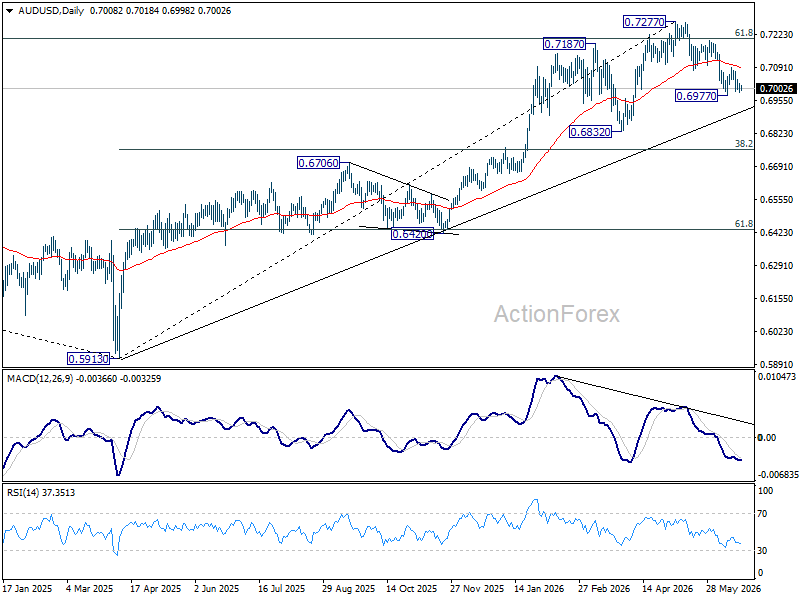

The technical picture suggests that the market is already cautiously bearish.

- AUD/USD was rejected with a 61.8% retracement from 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206.

- The daily bearish MACD divergence remains firmly in place.

- Repeated failure below the 55D EMA, currently at 0.7093.

They reinforce the view that The May high at 0.7277 could be an important medium-term top.

A hotter than expected CPI report could trigger a rebound. But unless buyers can force a sustained breakout above the 55D EMA, the burden of proof remains on the bulls. The biggest move may not come on Wednesday at all. It may come after 24 hours when the labor market ruling arrives.

On the downside, a strong breakout at 0.6977 would extend the decline from support 0.7277 to 0.6832 or to 38.2% retracement levels from 0.5913 to 0.7277 at 0.6756. If the pair decisively breaks above the 55 D moving average, the correction from 0.7277 may already be over, opening the door for a return towards the highs.

This week’s CPI and employment reports could determine whether August will lead to a final hike in interest rates – or confirm that the battle against inflation has entered a new phase. For AUD/USD, the answer may determine the fate of 0.7000.