The New Zealand dollar has emerged as one of the weakest major currencies this week, with the NZD/USD pair breaking to a multi-month low, as a combination of global risk aversion, broad-based dollar strength, and rapidly fading expectations of near-term RBNZ tightening weighed heavily on the currency. The selling has accelerated significantly in recent sessions, reflecting a sharp reversal from the narrative that supported the Kiwi during April and May.

The transformation begins with oil. Earlier this year, escalating tensions between the US and Iran sent energy prices soaring, raising concerns that imported inflation would become more persistent across the New Zealand economy. Markets responded by increasingly pricing in the prospect of a rate hike by the Reserve Bank of New Zealand, with speculation growing that policymakers may act as soon as the July 8 meeting. This hawkish narrative has helped support the New Zealand dollar even as concerns about global growth persist.

Since then the geopolitical background has changed dramatically. The US-Iran ceasefire agreement and subsequent progress toward a broader peace framework has seen oil prices fall sharply, removing much of the inflationary urgency that had pushed the Reserve Bank of New Zealand toward a more hawkish stance. Instead of debating whether a July rate hike is likely, investors are wondering whether the central bank needs to act at all in the near term. The collapse of the rally forecast has become a major headwind for the New Zealander.

Local economic conditions reinforce this caution. Q2 GDP forecasts point to stagnation or even outright contraction, while both the manufacturing PMI and services PMI remain stuck in contraction territory. Against this backdrop, the Reserve Bank of New Zealand faces a difficult balancing act. Policymakers remain alert to inflation risks, but excessive policy tightening could put additional pressure on an already fragile economy.

Market prices were adjusted accordingly. Just a few weeks ago, interest rate swaps were aggressively pricing in the possibility of a 25 basis point increase in July. These expectations have largely evaporated after the geopolitical escalation subsided. Recently, Westpac has argued that lower global fuel prices should mitigate the recent rise in inflation and reduce the risk of a broader and more persistent price acceleration. As a result, the bank now expects the RBNZ to remain on hold until September, while warning that policymakers may become increasingly cautious about how quickly interest rates should rise after that.

At the same time, the external environment is becoming increasingly hostile to the New Zealand dollar. Global technology stocks have come under pressure amid a wave of deleveraging, which has encouraged investors to reduce exposure to risk-sensitive currencies. Meanwhile, the dollar has benefited from safe-haven demand and growing speculation that the Federal Reserve may raise interest rates once or even twice later this year. This growing policy divergence between the Fed and the Reserve Bank of New Zealand has added additional pressure on the NZD/USD pair.

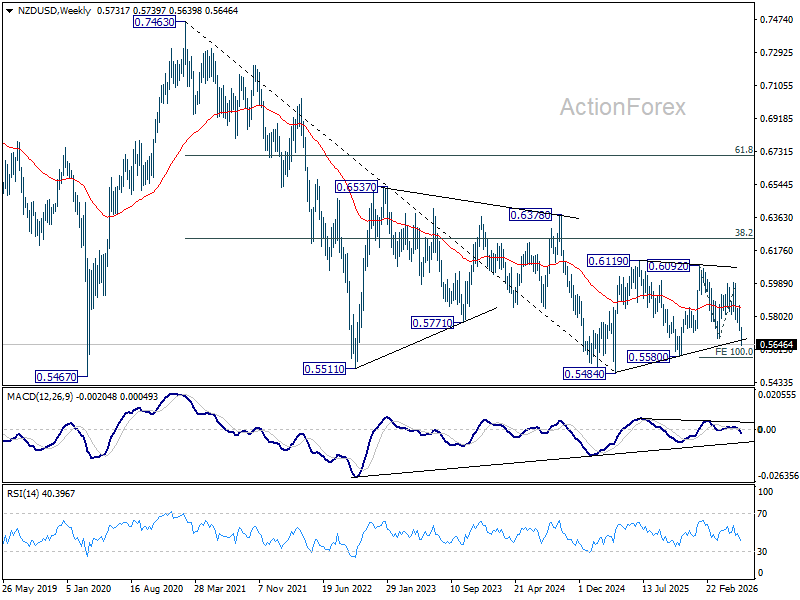

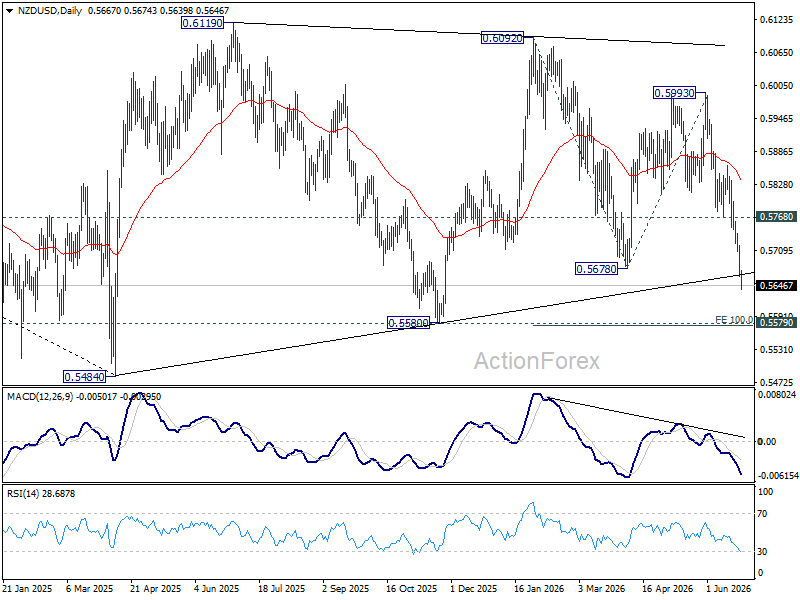

Technically, the outlook has deteriorated significantly. A break below 0.5678, the April low, confirms a resumption of the broader decline from the January high of 0.6092. As long as the support at 0.5768 turns into resistance, further losses remain preferable.

The next major target is at the 0.5580 support range, including a 100% forecast from 0.6092 to 0.5678 from 0.5993 at 0.5579. This area may be crucial.

A strong breakout would not only signal a renewed downward acceleration, but would also strengthen the case for the completion of the entire corrective pattern from the 2025 low at 0.5484 at 0.6092. Both could reinforce each other, and suggest that the long-term downtrend from 0.7463 (2021 high) is ready to resume through the 0.5484 low.