USD/JPY is once again knocking on Japan’s intervention zone door, but this week’s battle is about much more than just Tokyo entering the market. It has become a high-stakes game of chicken. Traders believe Japan is reluctant to intervene ahead of the US non-farm payrolls report on Thursday. And Japan knows that traders think so. The result is a dangerous window where both sides may be waiting for the other to blink first.

The Ministry of Finance has good reason to be patient. Launching a large-scale intervention just days before one of the most important US data of the year would be a costly gamble. If Tokyo spends $30-40 billion to push USD/JPY back below 160.00, only to see payrolls crush expectations and send the dollar higher again, those reserves could be wiped out within hours. Worse still, a failed intervention would damage the psychological deterrent that has become one of Japan’s most valuable policy tools.

Japan also has little incentive to fight a market that is still moving in a relatively orderly manner. Officials have repeatedly stressed that the intervention is designed to mitigate excessive one-sided volatility and not to defend a particular exchange rate. A steady rise driven by pre-payroll positioning is very different from the kind of unregulated rise that usually justifies formal action.

This hesitation is exactly what encourages speculators to bullish the dollar. Hedge funds, carry traders, and momentum calculators know that Tokyo is unlikely to burn through its ammunition ahead of such a major macro event. With the Fed keeping interest rates at 3.50%-3.75% after its hawkishness in June, and the Bank of Japan recently raising interest rates to 1.00%, the yield advantage is still very much in the dollar’s favour. As long as the interest rate gap exceeds 350 basis points, traders will have every incentive to continue testing the resistance around the 162.00 level.

Ironically, the most dangerous period for dollar bulls may begin after the payroll report rather than before. If the data simply meets expectations – or even disappoints slightly – the dollar may start to decline on its own. This would give Tokyo a much better opportunity to intervene, because it would no longer be resisting a strong macro trend. Alternatively, officials can use the market’s momentum against speculative positions.

Timing can further amplify the effect. With US markets closed for the Independence Day holiday, foreign currency liquidity is expected to decline sharply. Under these circumstances, a routine yen buy that would normally move the market by about 100 pips could instead lead to a violent 400-500 pip decline with stop-loss orders cascading across an empty market. Therefore, the biggest risk of intervention this week may come after the salaries are published, rather than before.

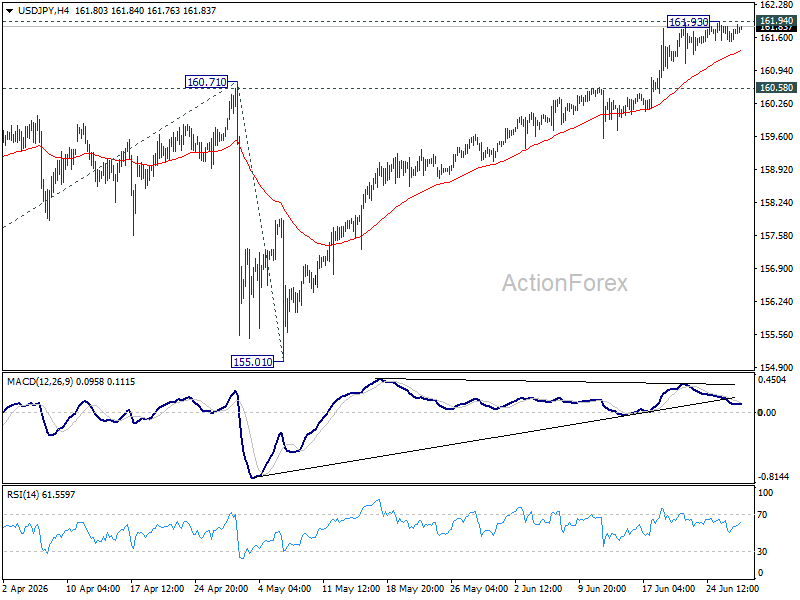

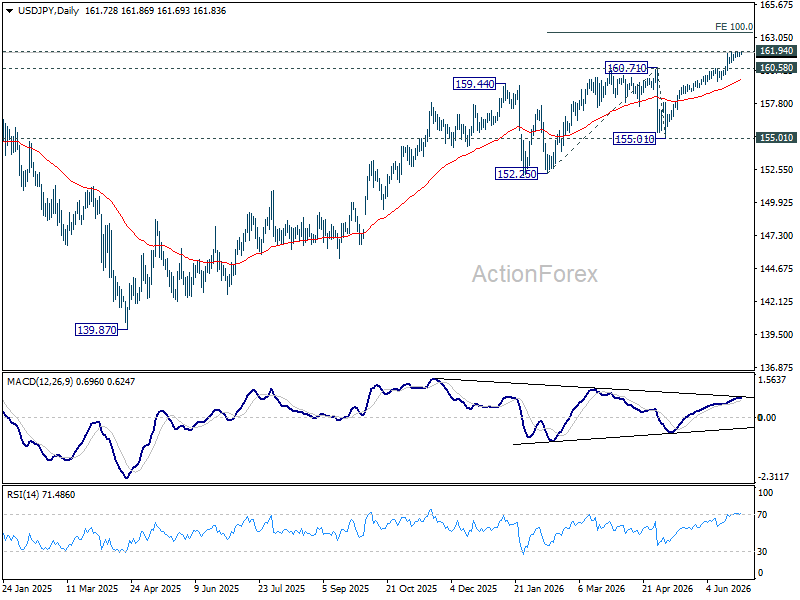

Technically, USD/JPY remains confined to a very narrow range below the 161.94 region (highest level in several decades in 2024). Further upside remains preferable as long as support at 160.58 holds. A strong break of 161.94 would target a 100% forecast from 152.25 to 160.71 from 155.01 at 163.47 next.

However, a strong break of 160.58 would confirm a short-term top, and quickly push USD/JPY below the 55 EMA (now at 159.71).