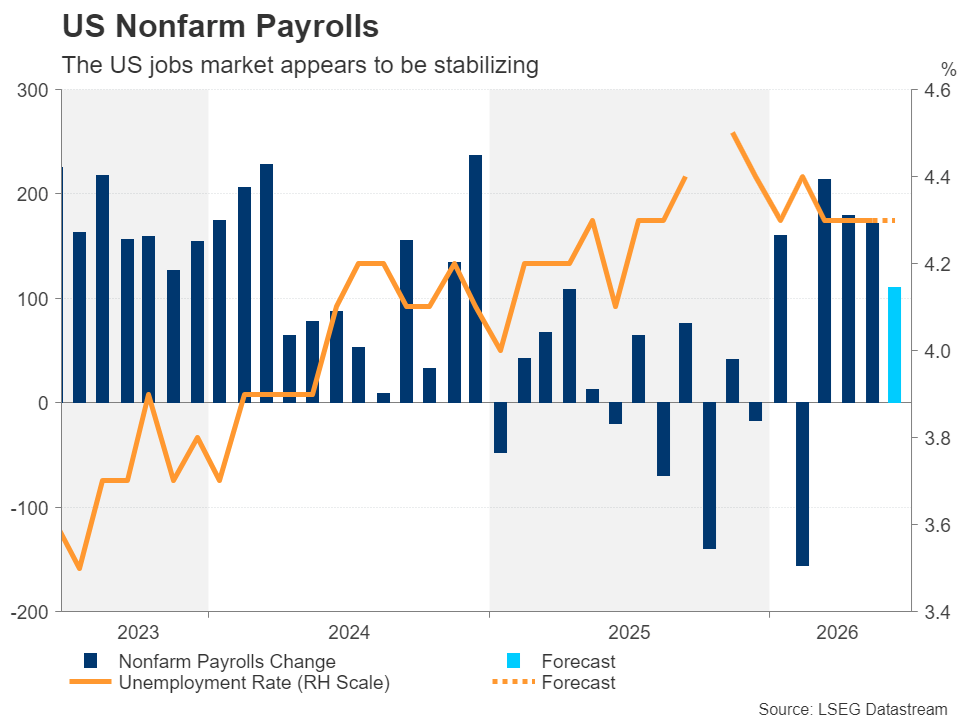

- The US jobs market will likely slow in June, but the World Cup could skew the data.

- Warsh’s debut in Sintra will also be crucial for the US dollar.

- But after the FOMC’s surprise in June, will the optimistic forecasts be matched?

- Warsh will speak on Wednesday (13:00 GMT), and the non-farm payrolls report is due early Thursday (12:30 GMT).

A stream of data and central bank talk

Investors are bracing for a busy week, as the latest jobs report will not be released for just a day due to markets being closed on Friday for Independence Day, but new Fed Chairman Kevin Warsh is speaking for only the second time since taking office. If that’s not enough to keep traders glued to their desks, there’s also a slew of other US data on the way that could shape expectations about the Fed’s policy path.

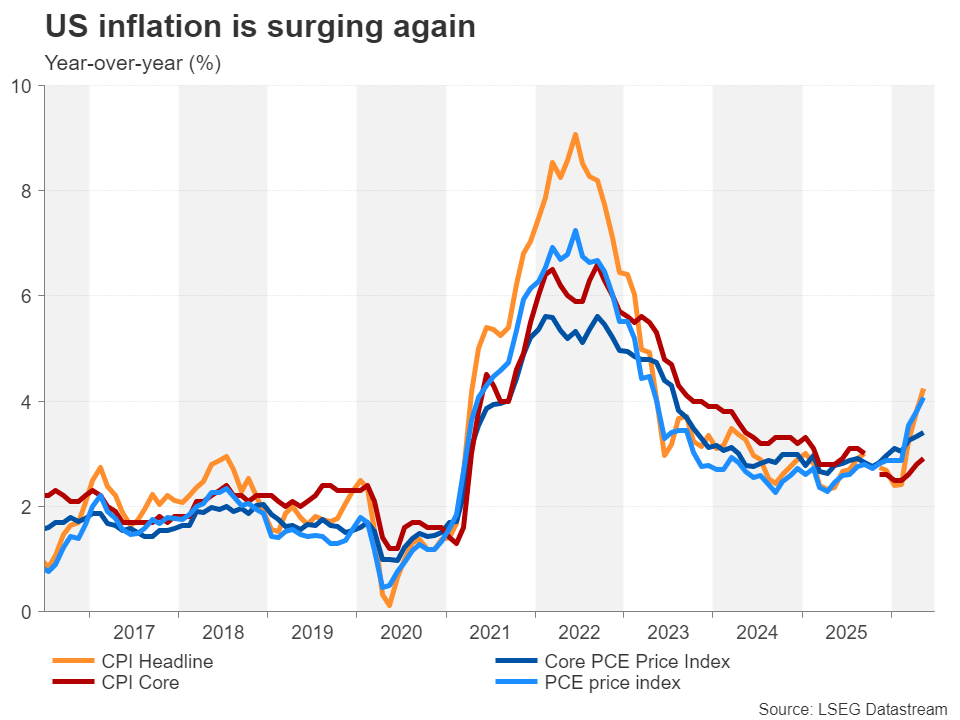

As these risk events approach, investors are taking somewhat hawkish positions, factoring in just over three-quarters of the probability of a 25 basis point rate hike in September, representing a slight decline from near-100% probabilities following the policy decision in June. However, markets have read Kevin Warsh’s message loud and clear – taming inflation is the Fed’s top priority right now, and not much is expected in the way of future guidance.

Deciphering the new Fed Chairman

The latter has increased the chances of greater volatility in reaction to incoming data, not only with investors scrutinizing each economic indicator but also due to a lack of clarity about which data points the Fed will focus more on under the new regime. Wednesday’s panel discussion in Sintra, Portugal, organized by the European Central Bank, is an opportunity for Lorsch to outline more details about how the Fed intends to return inflation to 2%.

However, with other central bank chiefs also invited to participate in the committee – the Bank of England’s Bailey and the Bank of Canada’s Macklem, along of course with President Lagarde – Warsh may not reveal his views much more than he did in his post-meeting press conference two weeks ago. If anything, there is a risk that Warsh will not sound as hawkish as he did in his first FOMC appearance, which could reflect New York Fed Chairman Williams’ recent neutral stance on the direction of interest rates.

Is another hot NFP report on the cards?

If this happens, the negative reaction to any bullish surprises in Thursday’s jobs report will likely be more subdued. After May’s better-than-expected reading of 172K, the June Nonfarm Payrolls forecast calls for a more moderate increase of 110K. The unemployment rate is expected to stabilize at 4.3% for the fourth month in a row. However, growth in average hourly earnings is expected to accelerate slightly to 3.5% year-on-year in June.

Another stronger than expected headline number would increase bets on a rate hike in September, or even earlier in July. This is certainly possible because lower energy prices due to de-escalation in the Middle East and a boost to the economy from hosting the FIFA World Cup likely led to increased employment in June.

Volatile times against the dollar

However, for the US dollar, it will be a tough lead-up to the jobs announcement on Thursday. Aside from the ECB Forum and NFP data, traders will also have to juggle the June Consumer Confidence gauge and May JOLTS Job Openings on Tuesday, as well as the ISM Manufacturing PMI, ADP Employment Change and Challenger Layoffs, all for June, on Wednesday.

Meanwhile, any updates on the US-Iran talks will also test dollar bulls, not to mention comments from other central bankers at Sintra. In particular, the euro will be almost in the spotlight, as Lagarde may seem a bit more optimistic about the eurozone’s inflation outlook now that oil prices are almost back to pre-war levels.

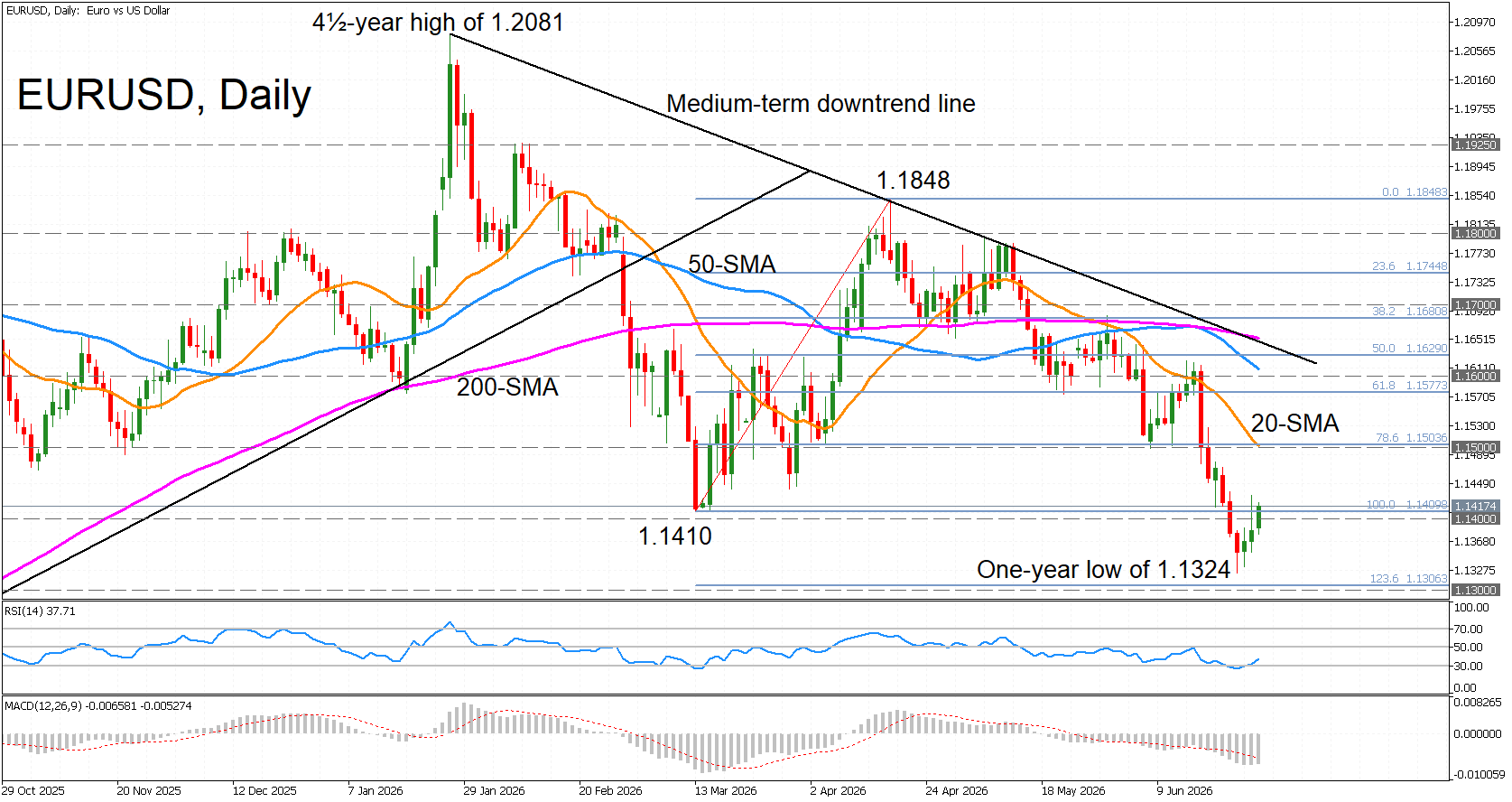

Is the euro in danger of breaching $1.13?

Interestingly, lower geopolitical risks were unable to offset the support the dollar received as a result of the Fed’s hawkish bias. The euro recorded its lowest levels in a year last week after falling below $1.1400. An upbeat set of labor market indicators from the US would reinforce the upbeat outlook, triggering a fresh sell-off towards the $1.1300 area, which is near the 123.6% Fibonacci extension of the March-April recovery.

But weak non-farm payrolls numbers, combined with more neutral Warsh data, could support the euro towards its 20-day moving average above $1.1500.

Wall Street will also be closely watching Warsh’s speech and salary numbers. The S&P 500’s recent lower high suggests the AI rally is starting to cool off. A hot jobs report would create a major hurdle to a new all-time high, as it would likely fuel a rate hike in September.