Our summary of recent economic events and what to expect in the coming weeks.

Notable Canadians

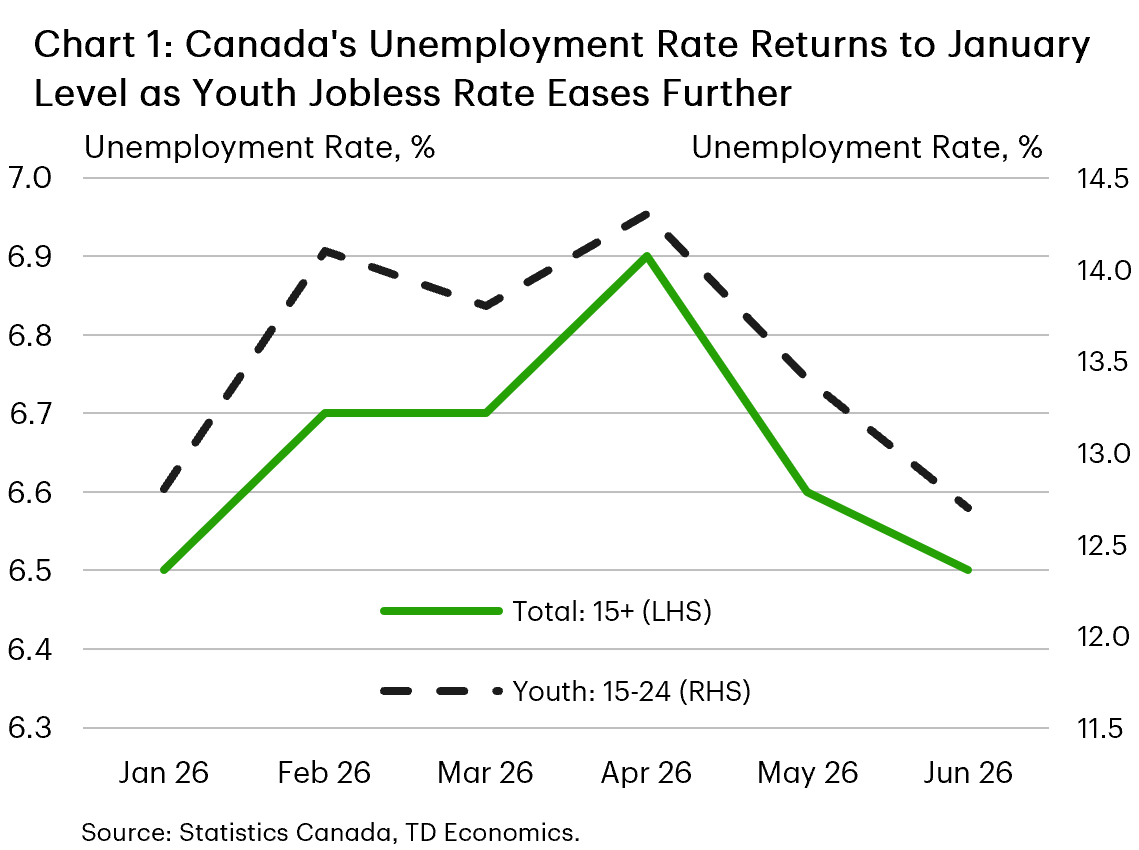

- Canada’s economy added 18,000 jobs in June, while the unemployment rate fell to a five-month low of 6.5%.

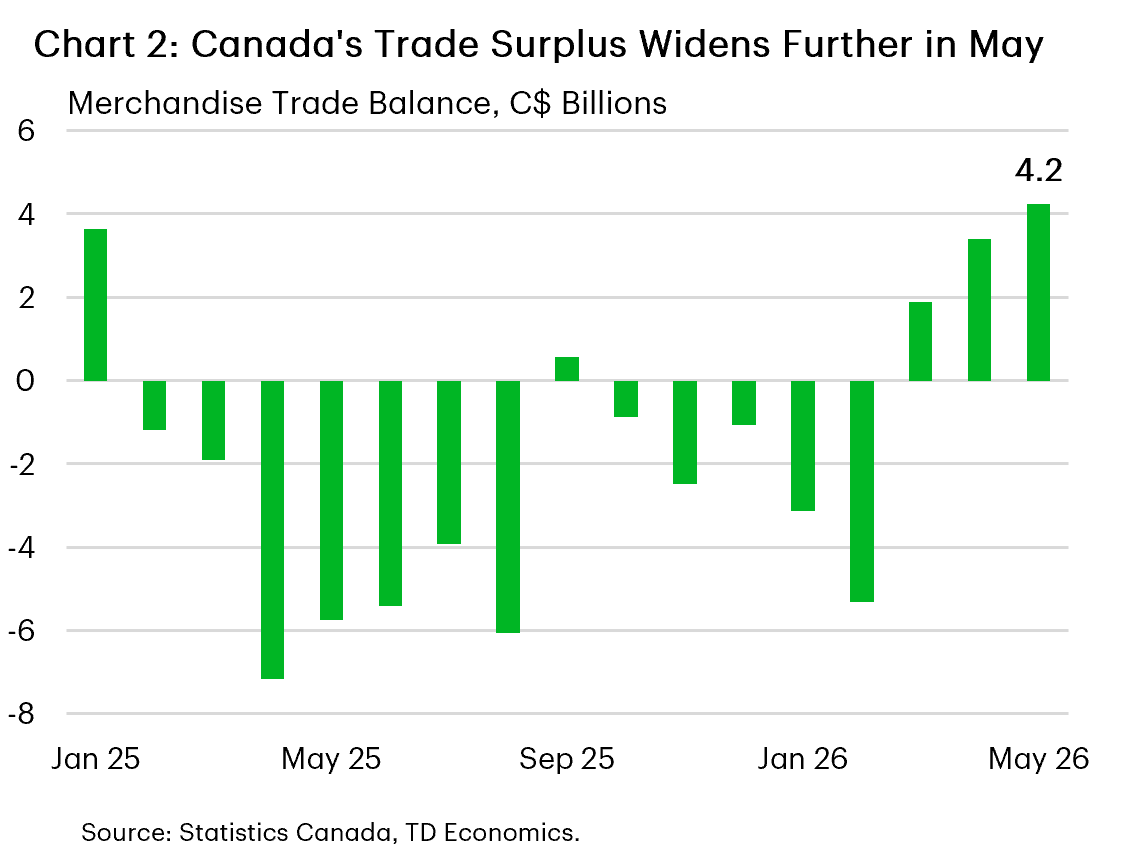

- Canada’s merchandise trade surplus widened in May, boosting prospects for a growth rebound in the second quarter.

- Business and consumer sentiment remained weak, amid a slight rise in household inflation expectations. However, this is unlikely to change the Bank of Canada’s outlook, as interest rates are expected to remain at 2.25% upon next week’s announcement.

Highlights in the United States

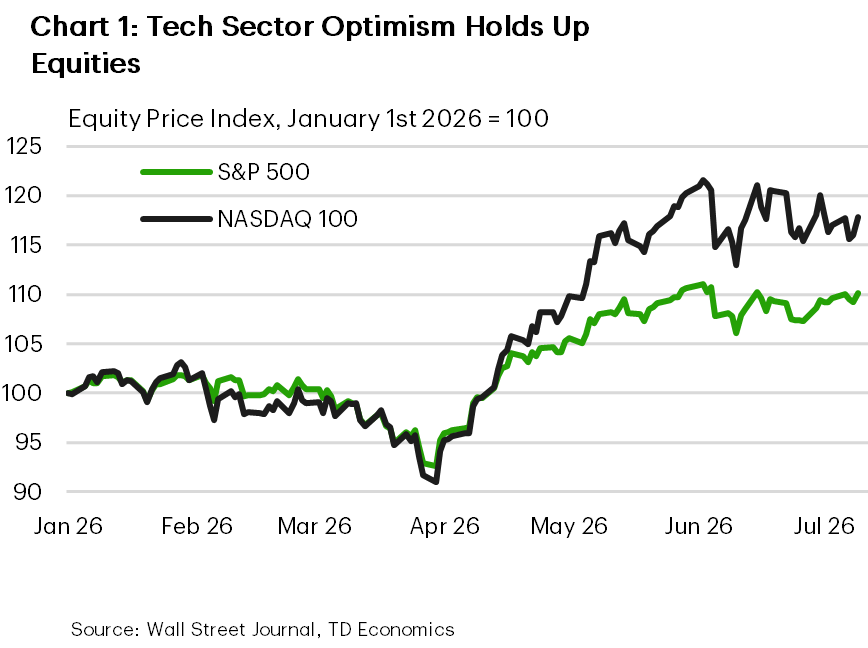

- Markets had a week of geopolitical shocks, as optimism in artificial intelligence and chips helped keep US stocks near record levels.

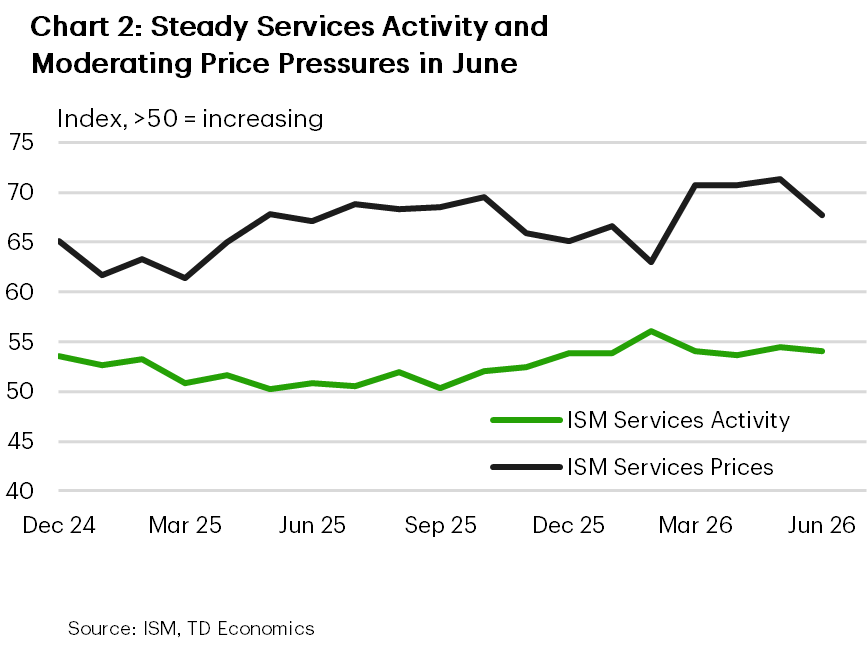

- The ISM Services Index declined only modestly in June, as activity and orders continued to expand and employment returned to growth.

- Existing home sales were disappointing as affordability remained binding, while FOMC minutes confirmed the Fed is divided but remains focused on inflation.

Canada – Steps in the right direction

It’s summer and life is easy – or at least that’s the impression of this week’s economic data. Trade surprised to the upside, while another month of job gains, albeit modest, suggests the economy is still in decline, but has put recession fears to rest. These releases were largely received by the markets, with attention focusing squarely on developments in the energy markets. The collapse of a fragile ceasefire in the Middle East sent crude oil prices higher during the week. The S&P TSX ended the week flat, while the Canadian dollar rose about 1 cent against the US dollar.

The Canadian economy added 18,000 jobs in June, with employment concentrated in the private sector, led by accommodation and food services. The unemployment rate fell to 6.5%, returning to where it started the year (Chart 1). Given the month-to-month fluctuations, the broader picture remains encouraging: employment is up year-on-year, with hiring concentrated in full-time private sector jobs, while the unemployment rate has declined slightly faster than expected in our June forecast. Another welcome development is improved youth labor market conditions, with the youth unemployment rate falling to 12.7%, after reaching a peak of 14.6% last September. Statistics Canada also noted that the summer job market for students appears more favorable than it did a year ago.

The trade provided further evidence that the economy is moving in the right direction. Canada’s merchandise trade surplus widened to $4.2 billion in May, consolidating the improvement seen in recent months (Chart 2). This increase was primarily driven by strong exports to the United States, while exports to non-US destinations continued to decline. Imports fell, partly reversing the increase seen in April. Combined with the April GDP report, the latest trade data strengthens the case that economic growth will rebound in the second quarter after slowing in each of the previous two quarters.

However, the business picture is still far from stable. Monthly trade flows continue to be strongly influenced by volatile sectors, suggesting that the contribution of net exports is likely to remain uneven over the remainder of the year. Importantly, high trade policy uncertainty continues to impact business and household confidence. This caution was evident in the Bank of Canada’s latest Business Expectations Survey and the Canadian Survey of Consumer Expectations. Business sentiment remained weak in the second quarter, amid weak hiring intentions and continued reports of weak demand. Consumers also remained cautious, while their inflation expectations rose modestly. One caveat is that the surveys were conducted during the recent rise in energy prices and are therefore likely to overestimate the extent to which underlying inflationary pressures will persist.

Taken together, this week’s releases remain consistent with our broader outlook. The improvement in trade coupled with a labor market that continues to generate employment indicates that the economy is still afloat despite increasing uncertainty. With little evidence that higher oil prices are spilling over into broader inflation, we expect the Bank of Canada to keep interest rates unchanged at 2.25% at its policy meeting next week.

Maria Solovieva, CFA, economist

United States – NATO tensions on Nasdaq records

The week began with investors dealing with another round of geopolitical shocks. The NATO summit highlighted changing headlines regarding the US-Iran conflict, including renewed doubts about the continuity of the ceasefire and subsequent reports of technical talks. Oil prices moved with each headline, but the broader stock market held up well. The S&P 500 has remained near the record it set in early June and is up nearly 10% this year, while the Nasdaq has been buoyed by renewed enthusiasm around demand for AI-related chips (Chart 1). In short, markets remain willing to consider geopolitical uncertainty as long as energy prices remain under control and the technology earnings story remains intact.

The week’s data provided some support for this resilience narrative. The ISM services index fell to 54.0 in June from 54.5 in May, but remained comfortably in expansionary territory for the 24th straight month. Details were mixed, but not alarming. Business activity and new orders slowed, while the employment index returned above 50 for the first time in four months. Price pressures also eased, with the prices paid index falling to 67.7 from 71.3, although that still leaves services sector inflation hot (Chart 2). The bottom line here is that demand is trending toward moderation, but the service economy is not declining.

Housing sent a less encouraging signal. Existing home sales fell 2.4% in June to an annual pace of $4.09 million, missing expectations, while the median resale price rose to a record high of $440,600. Inventory remains too weak to provide significant price relief, and high mortgage rates continue to keep buyers and sellers on the sidelines. Meanwhile, minutes from the FOMC meeting showed that the committee is still grappling with inflation expectations. Officials appear to be divided between scenarios in which lower energy prices and fading effects of tariffs allow inflation to cool, and scenarios in which persistent price pressures driven by AI-related investment demand require a tougher policy. New York Fed President John Williams later said the minutes effectively captured the committee’s “collective reaction function,” stressing that policymakers were considering a range of inflation scenarios rather than pointing to a predetermined rate path.

Taken together, the week’s data points to an economy slowing on the margins, but still achieving moderate growth. Services activity remains expansive and employment has stabilized, while housing remains constrained by affordability rather than excessive weakness in demand. The FOMC minutes confirm that the Fed is not on a predetermined path, but they also do not provide much comfort to markets looking for imminent easing, or even an anchor for their expectations. The barrier to raising interest rates again is likely to depend on whether inflation is broader and more persistent. This makes next week crucial: the CPI will test whether price pressures are easing, while Chairman Warsh’s testimony to Congress should clarify how the Fed weighs inflation risks against a still-resilient growth backdrop.