The dollar ended the week without a clear direction, despite a real shift in the US inflation picture. Both the June CPI and PPI surprised to the downside, reinforcing the view that price pressures have begun to ease more broadly. But instead of expanding lower, the dollar stabilized as investors wondered whether the low inflation story would still be intact one month later.

This hesitation reflects the second development of the week, which was ultimately more forward-looking. The renewed escalation in the US-Iran conflict sent oil prices sharply higher, with Brent closing above $88 and WTI recovering to the $80 level. Because weaker inflation in June was largely driven by lower energy prices, the immediate rebound in crude oil prices raises the possibility that much of this progress will be reversed over the next inflation report or two. In other words, markets have shifted their focus from what inflation has done to what it is likely to do next.

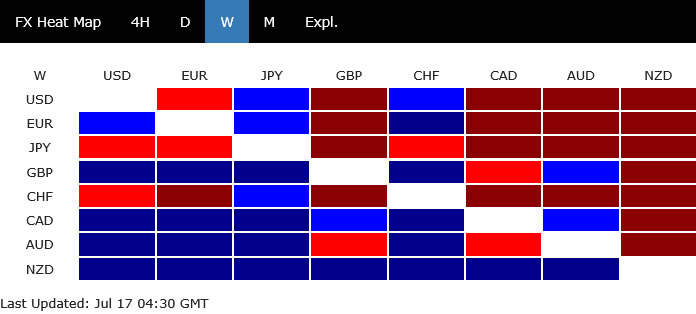

The result was a market stuck between conflicting forces. Falling inflation reduced the urgency for further Fed tightening, but higher oil prices simultaneously revived the risk that inflation could accelerate again, preventing expectations of interest rate hikes from fading. This cross-current has been reflected in the currency’s performance. The New Zealand dollar led gains during the week, followed by the Canadian dollar and British pound, while the yen finished as the weakest major currency. The dollar held near the midpoint of the rating, an appropriate reflection of a market still weighing yesterday’s disinflation against tomorrow’s inflation risk.

A weak Consumer Price Index (CPI) and Producer Price Index (PPI) changed the Fed’s forecasts – temporarily

June inflation reports provided one of the strongest evidence yet that price pressures in the US were moderating. The headline CPI fell -0.4% m/m after rising 0.5% m/m in May, bringing the annual rate down from 4.2% m/y to 3.5% m/y, comfortably below market expectations. Core CPI was unchanged on a monthly basis, slowing from 2.9% y/y to 2.6% y/y. At the wholesale level, the Producer Price Index fell -0.3% month-on-month, its biggest monthly decline in more than six years, reinforcing the view that pipeline inflation pressures are easing.

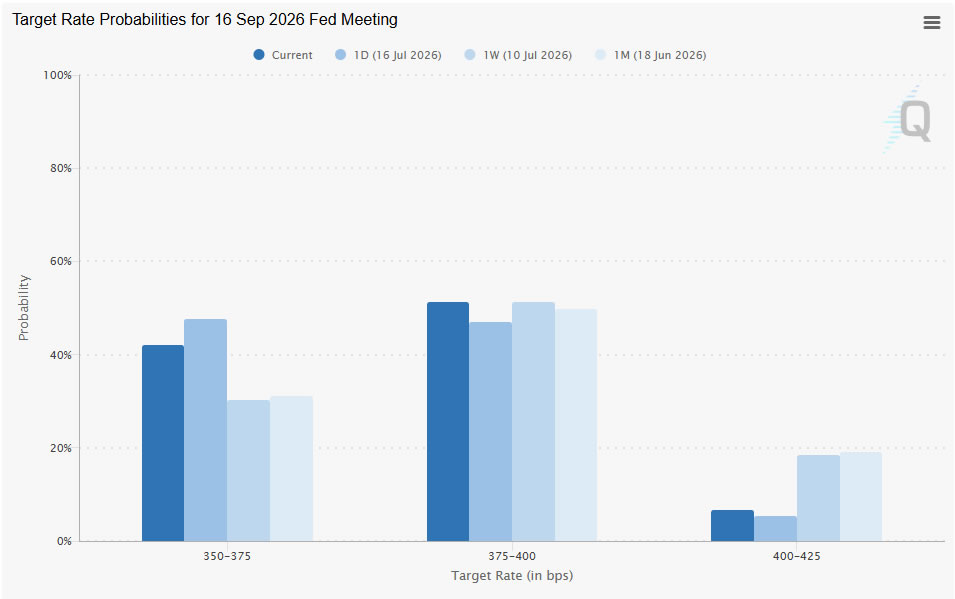

The breadth of the slowdown suggests that this was more than a one-time statistical fluctuation. After months of flat inflation, successive downward surprises in consumer and producer prices have prompted investors to reassess the urgent need for additional Fed tightening. Fed funds futures reacted quickly, with the implied probability of a September rate hike falling from about 70% the week before to about 58% immediately after the data was released.

However, the combination of decelerating inflation provided an important warning. Lower gasoline prices accounted for a large share of the improvement in both the Consumer Price Index and the Producer Price Index, reflecting a period in which tensions in the Middle East briefly eased and oil prices declined. As energy markets reversed later in the week, investors quickly realized that June’s encouraging inflation data was based on a foundation that had already begun to shift. The result was a story of low inflation that seemed real, but also increasingly fragile.

WTI above $80 changes the inflation narrative

The development that defines the market this week may ultimately turn out to be not weak inflation data, but rather a decisive rebound in crude oil. As the conflict between the United States and Iran intensifies, concerns about energy supplies have escalated sharply. The conflict expanded beyond previous tit-for-tat exchanges, with strikes targeting bridges, railway infrastructure, communications facilities and an airport inside Iran, while Iranian retaliation spread across Kuwait, Bahrain, Qatar, Oman and a US military site in Syria. Against this backdrop, WTI settled above US$80 and Brent closed above US$88, recording its strongest weekly gains since April.

The significance of WTI recovering to $80 lies in what it means for inflation expectations. The lower inflation surprise in June was largely driven by lower energy prices after a temporary decline in tensions in the Middle East earlier in the month. Now that crude oil has recovered those losses, the energy component is likely to move in the opposite direction over the coming months. Markets are therefore beginning to wonder whether June’s encouraging CPI and PPI readings will prove to be the low point rather than the beginning of a sustained moderation in inflation.

These changing expectations also explain why expectations for another Fed rate hike have not continued to decline despite the weak data. Investors have become less focused on what inflation showed in June, and more concerned about what inflation might look like in July and August if oil prices remain high. With crude oil now becoming a renewed source of inflation risk, energy markets – not last month’s economic data – have become the main driver of the Fed’s repricing, and thus the dollar’s direction.

The Fed is keeping the door open for further tightening

Federal Reserve officials broadly maintained a dovish and hawkish tone throughout the week, even as June inflation reports appeared weaker than expected. In testimony before Congress, Chairman Kevin Warsh rejected any suggestion that the Fed’s mission was complete, arguing that inflation remained too high despite recent progress. He also stressed that monetary policy “has not been particularly restrictive”, reinforcing the view that the committee still sees room for further tightening if inflation risks intensify.

Gov. Christopher Waller echoed that position. Ahead of the inflation data, he noted that another rate hike may be justified in the near term if the CPI and PPI surprise to the upside. While the actual data reduced the immediate case for further tightening, his comments made clear that the Fed remains highly sensitive to any renewed inflationary pressures. Dallas Fed President Lori Logan emerged as the most hawkish voice this week, becoming the first Fed official to publicly support another rate hike since Warsh became chairman.

The Fed’s overall message has changed little despite the encouraging inflation data. Policymakers acknowledged the improvement but showed no willingness to signal that raising interest rates was off the table. Instead, the committee seems content to let incoming data – and increasingly developments in energy markets – guide its next move. With the Fed offering few surprises, markets have become more focused on whether higher oil prices will eventually force policymakers back into a more aggressive stance.

Technical Outlook: Dollar awaits confirmation from oil and yields

Brent crude It remains the main indicator of the market. The advance from 70.14 has taken on the characteristics of a five-wave impulsive rally, indicating a potential reversal to the upside. A close above the 55 D EMA (now at 85.75) reinforces this interpretation. The next crucial test is at the 38.2% retracement level from 119.50 to 70.14 at 89.00, an area that also coincides with the psychologically important 90 level.

A decisive break above the 89/90 area may indicate that Brent is already fully reversing its decline from 119.50. This would pave the way for the 61.8% retracement at 100.64, which is close to the psychological level of 100. Failing to overcome the 89-90 area, followed by a break below 83.71, one might instead argue that the recent rally was just a corrective bounce, and it is complete.

US 10-year yield It fell to 4.51 but quickly recovered after drawing support from the 55 four-hour EMA (now at 4.51). There is no change in the forecast as the correction from 4.69 is completed at 4.36, and the rise resumes from 3.96. Resistance above 4.62 will confirm this bullish case and target a retest of the 4.62 high.

Nasdaq Friday’s sell-off and break of the 55 D moving average (now at 25634.10) suggest that the consolidation pattern from 27190.21 extends with another bearish leg. Strong support should be seen around the 38.2% retracement from 20690.25 to 27190.23 at 24707.22 to contain the downside for a bounce. However, a strong break of the Fibonacci level support would indicate that this is not only a near-term correction, but could be on a broader scale and risk a deeper sell-off to the 61.8% retracement levels at 23173.23.

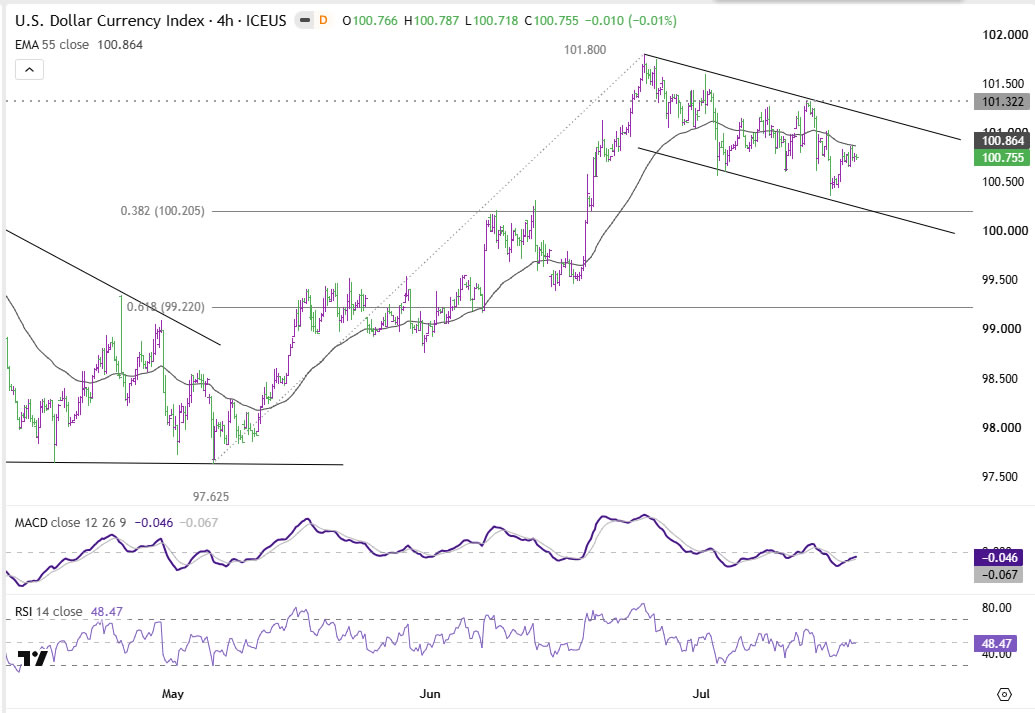

Dollar index The correction from 101.80 extended lower last week but is holding above the 38.2% retracement from 97.62 to 101.80 at 100.20, as well as the 55 D EMA (now at 100.17). Further rise is still expected. Above 101.32, secondary resistance will lead to a retest of 101.80 first. A strong break there would extend the entire rally from 95.55 to the 50% retracement level of 110.17 to 95.55 at 102.86. However, a sustained break of the 55 D EMA would bring a deeper decline back to 97.62 support, and increase the chance of a bearish reversal in the near term.

Outlook: Gulf developments are likely to determine the dollar’s next move

The dollar enters the new week still searching for a decisive catalyst. If the US-Iran conflict continues to escalate, Brent crude will likely challenge or exceed the $90 threshold, reinforcing expectations that the recent deflationary trend may be short-lived. Such an outcome would likely lift Treasury yields, boost pricing for another Fed rate hike later this year, and provide new support for the dollar.

On the other hand, any significant de-escalation that allows oil prices to decline would revive confidence in inflation returning to a downward path, encouraging markets to reduce hawkish expectations and reopen the door to broader dollar weakness.

At this point, an escalation scenario seems marginally more likely. The increasingly coordinated nature of recent military operations and increasing Iranian retaliation suggest that the conflict is entering a more dangerous phase than previous exchanges. However, investors have learned in recent weeks that geopolitical developments can change suddenly. Thus, the dollar remains at a crossroads, with its next major move likely to be determined less by Fed speech or scheduled data releases than by whether oil will continue to rewrite inflation expectations.

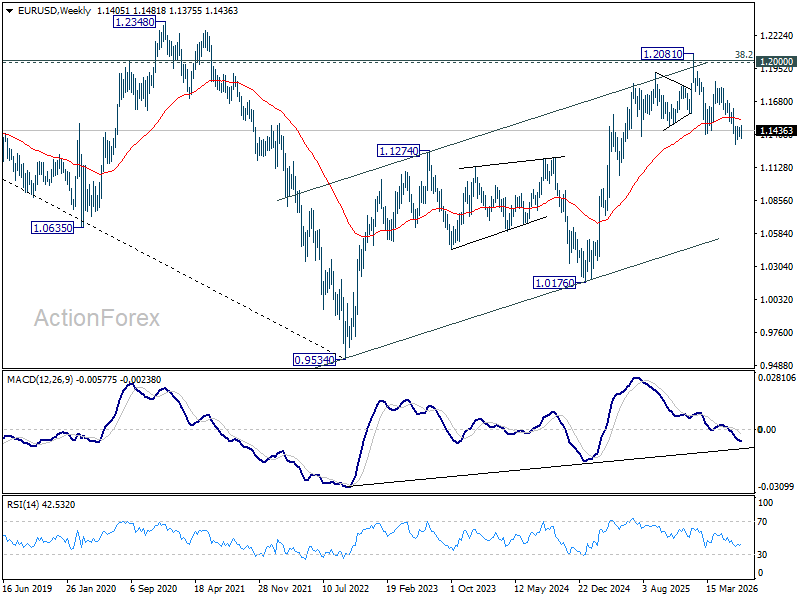

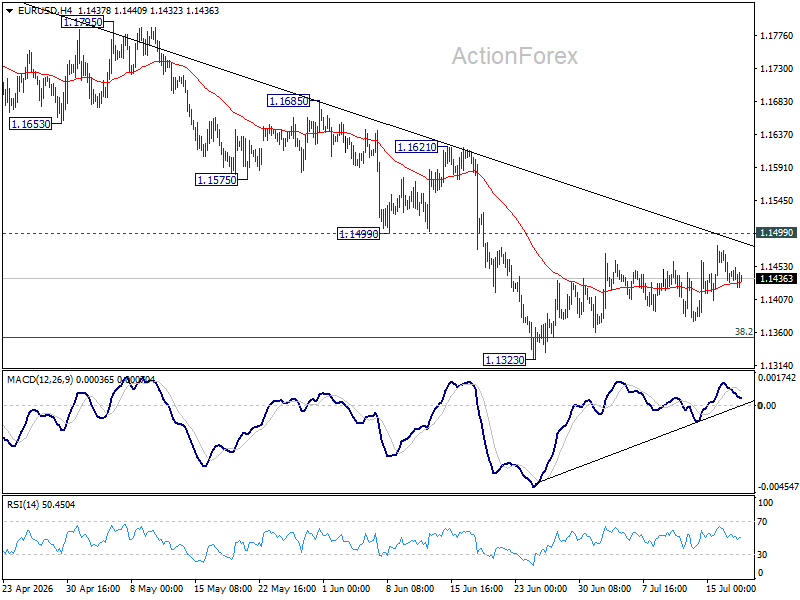

Weekly forecast for EUR/USD

EUR/USD extended the consolidation pattern above 1.1323 last week and the outlook remains unchanged. Initial bias remains neutral this week, and with support at 1.1499 turning into healthy resistance, further decline is expected. On the downside, a break of 1.1323 will resume the decline from 1.2081 to 100% prediction from 1.2081 to 1.1408 from 1.1848 at 1.1175. However, a decisive break of 1.1499 will bring back the upside bias to resistance at 1.1621.

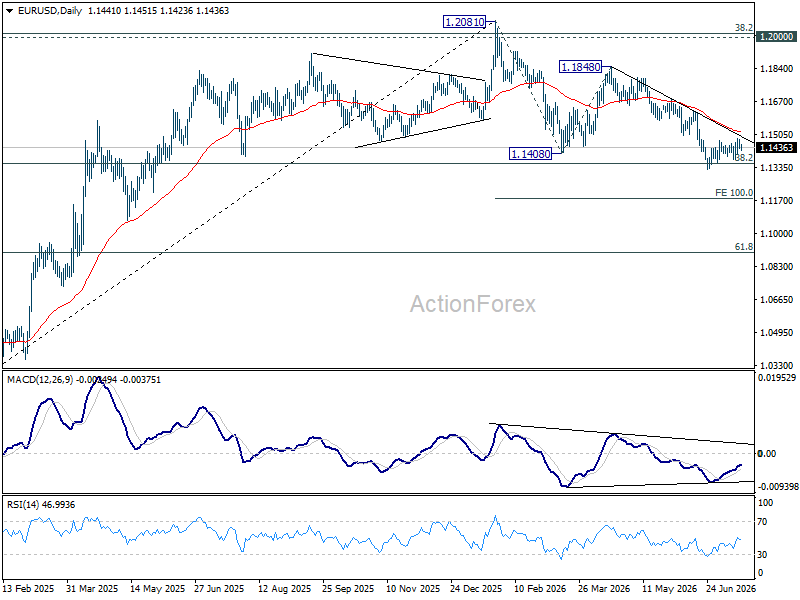

In the bigger picture, focus is back on the 38.2% retracement level from 1.0176 to 1.2081 at 1.1353. A decisive breakout there would revive the medium-term bearish trend reversal case after the rejection of the 1.2 key cluster resistance level. Further decline we should see to 61.8% retracement levels at 1.0904. However, a strong bounce from 1.1353, followed by a break of resistance at 1.1621, will sustain the upside in the medium term.

In the long-term picture, the 38.2% retracement from 1.6039 to 0.9534 at 1.2019, which is close to the psychological level of 1.2000 is key to the outlook. Rejection at this level would keep the multi-decade downtrend from 1.6039 (2008 high) intact, and keep the outlook neutral at best. However, a decisive break of 1.2000/19 would signal a reversal of the long-term upside trend, targeting the 61.8% retracement levels at 1.3554.