Please note that we are not authorized to provide any investment advice. The content on this page is for information purposes only.

Microsoft (NYSE: MSFT) released its fiscal second-quarter 2026 earnings on Wednesday after markets closed. The report was not received well by markets, and the stock fell nearly 10% yesterday, the single-day loss since 2020. Here are the key takeaways from the report and how analysts reacted to the earnings.

Key takeaways from MSFT’s earnings report

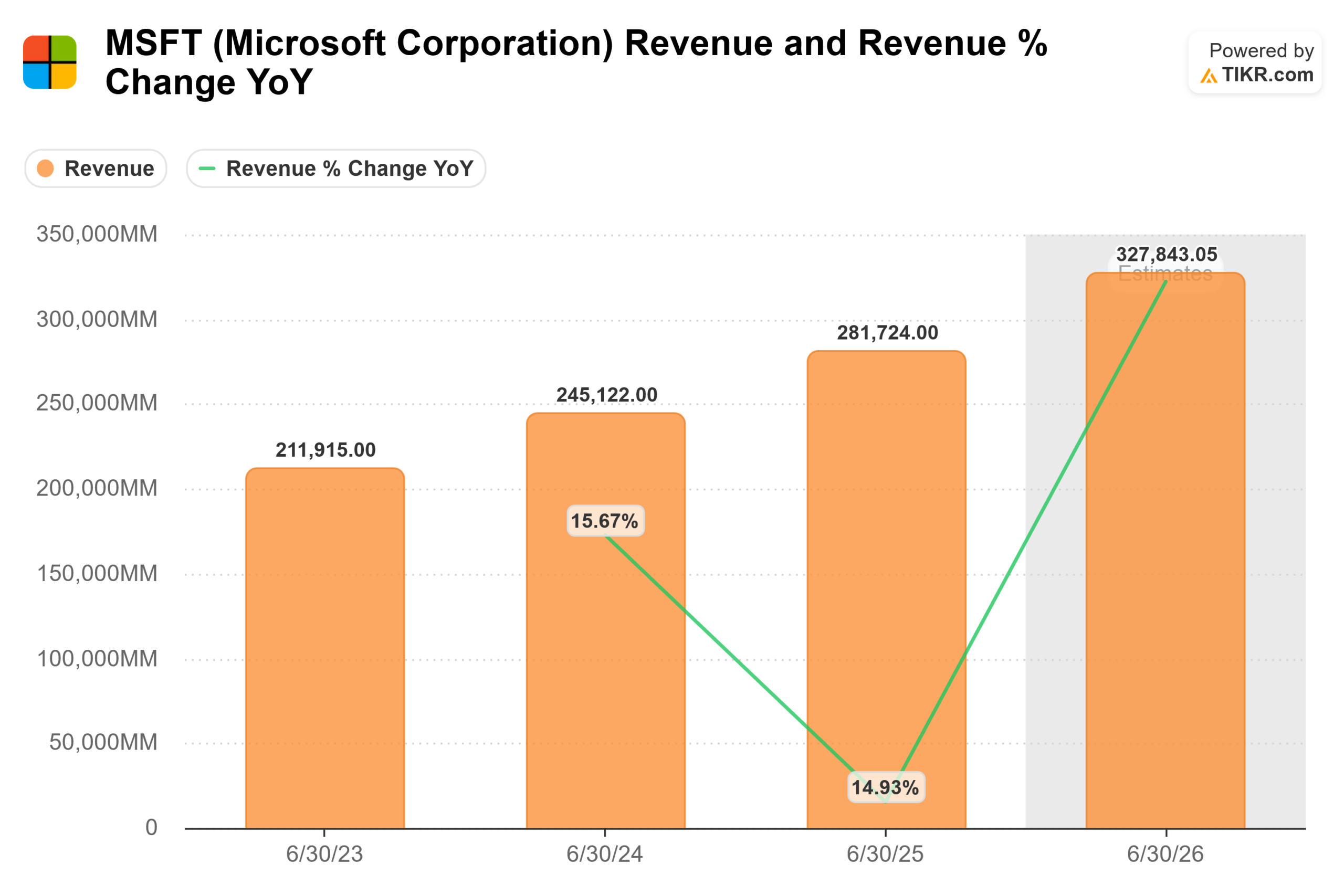

Microsoft reported revenues of $81.3 billion, an increase of 17% year over year, and ahead of consensus estimates of $80.27 billion. The company’s non-GAAP earnings per share were $4.14, beating analysts’ expectations of $3.97. The company’s massive investment in AI infrastructure was evident, with capital expenditures rising 66% to $37.5 billion as Microsoft built out physical capacity, including custom Maia and Cobalt chips, to meet continued demand for generative AI services.

Microsoft has seen widespread growth

Here’s how Microsoft’s various business segments performed this quarter.

- Intelligent Cloud: This segment remains the company’s main growth driver, with revenues up 29% to $32.9 billion. Within this, revenues for Azure and other cloud services grew 39%, fueled by massive demand for AI-powered infrastructure and a customer base that is increasingly migrating workloads to the cloud to support large-scale model training and inference. However, the growth rate was slightly lower than the 40% growth that Microsoft reported in the previous quarter.

- Productivity and Business Operations: Revenue increased 16% to $34.1 billion. Growth was driven by Microsoft 365 business cloud (up 17%) and a notable 29% increase in consumer cloud revenue. Additionally, Dynamics 365 achieved 19% growth, highlighting the continued integration of AI “agents” into business workflows through platforms like Agent 365.

- More Personal Computing: This sector saw a slight contraction, with revenues down 3% to $14.3 billion. While Windows OEM revenues showed resilience with 5% growth (helped by the approaching end of support for Windows 10), the segment was affected by a 32% decline in Xbox hardware sales, reflecting a slowdown in the global console market.

Microsoft cloud revenue reaches $50 billion

Meanwhile, Microsoft has reached a major milestone, as its cloud revenue surpassed $50 billion in the December quarter for the first time. The company is very bullish on the AI opportunity, and during the earnings call, CEO Satya Nadella said: “We are in the early stages of AI deployment and its broad impact on GDP. Our TAM will grow significantly across every layer of the technology as this deployment accelerates and spreads. In fact, even in these early roles, we have built an AI business larger than some of our largest franchises that took decades to build.”

Microsoft provided optimistic guidance

Looking ahead to the third quarter of fiscal year 2026, Microsoft presented a confident forecast with expected revenues between $80.65 billion and $81.75 billion, representing a growth rate of 15-17%. The company expects Azure revenue growth to remain strong at around 37-38% in constant currency. The guidance was pretty much in

While heavy capital spending is expected to continue to pressure margins in the short term, CFO Amy Hood noted that Microsoft Cloud’s gross margins should hover around 65%, as efficiency gains from custom silicon and “tokens per watt” improvements begin to offset the higher cost of purchasing a GPU.

Analysts lower their price targets on Microsoft

Despite the decline in Microsoft’s stock price, Wall Street analysts maintained their bullish view even as many of them lowered their price targets.

Keith Weiss of Morgan Stanley noted that the market “is not seeing the forest for the trees.” The observed slowdown is not due to a lack of customers; It’s a lack of hardware. CFO Amy Hood revealed that if Microsoft had not prioritized internal AI needs (such as Copilot) over external Azure customers, the growth KPI would have exceeded 40%.

“The debate is no longer about demand, it’s about timing of capacity,” added Evercore’s Kirk Mattern.

Dan Ives of Wedbush Securities lowered his price target from $625 to $575. “The company is benefiting from the growing momentum of the AI revolution… and the weakness in the stock price represents strong buying opportunities for long-term investors. We have said this is a multi-year journey,” Ives said in his note.

JPMorgan also lowered its price target on Microsoft from $575 to $550 while maintaining an outperform rating. “Microsoft showed a ‘strong demand picture’ in its quarterly results… Key drivers include softness in the less important gaming and search segments and CPU/GPU capacity constraints in Azure,” JPMorgan analyst Mark Murphy said in his note.

Goldman Sachs lowered its price target for MSFT

Gabriela Borges of Goldman Sachs lowered her price target on Microsoft from $655 to $600 while maintaining her buy rating. “We believe the stock reaction reflects another consecutive quarter of higher-than-expected capex without a commensurate increase in Azure growth. Trading short-term Azure growth now may lead to more long-term AI-driven growth.”

KeyBanc also lowered its price target for Microsoft from $630 to $600. In his note, analyst Jackson Adair said: “We know the short-term pain is real — we’re living it now. What we don’t know is whether the long-term gains are real. We have to wait for the investments to pay off.”

Hargreaves Lansdown’s Matt Bretzman also expects AI to drive Microsoft’s long-term growth.

“Demand for AI is so strong that Microsoft cannot build capabilities fast enough. AI services drive a large and growing portion of Azure’s growth… and this is a trend we expect to continue.”

OpenAI accounts for a large portion of MSFT’s Cloud Backlog

Microsoft revealed that its remaining business performance obligations (RPO) amounted to $625 billion. However, what is concerning is the fact that OpenAI represents 45% of this backlog. It is worth noting, Microsoft is the largest investor in OpenAIand its fortunes are closely intertwined with that of the artificial intelligence startup.

“The backlog is really good, but the revelation that OpenAI represents 45% of their backlog, it gets back to a position where OpenAI can meet those financial targets to pay Oracle, Microsoft and many providers,” Jefferies analyst Brent Thiel said in a recent interview. CNBC.