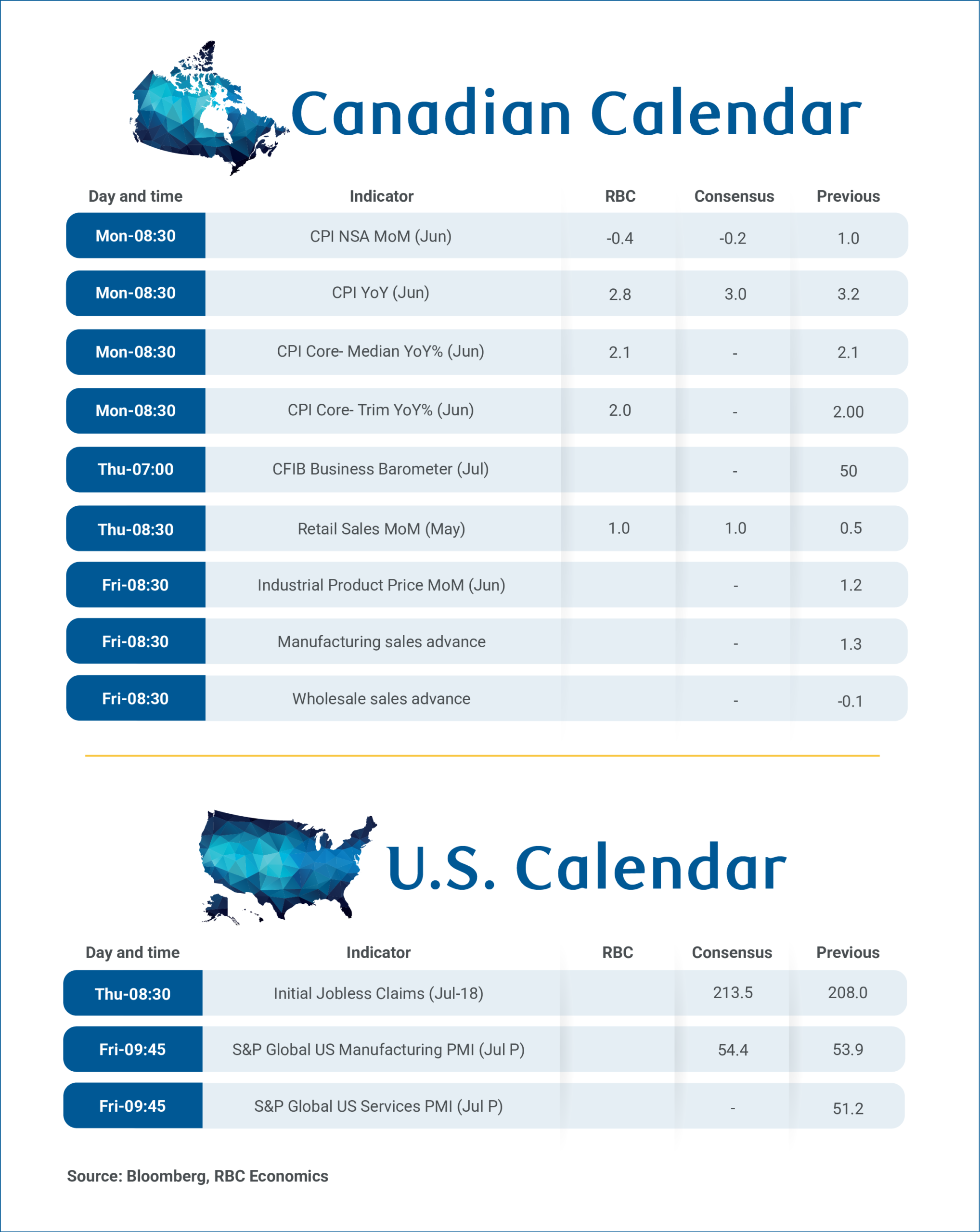

Monday’s June CPI report will provide an updated look at inflation trends following the Bank of Canada’s decision to leave interest rates unchanged for the sixth straight meeting.

We expect headline inflation to ease to 2.8% year-on-year, down from 3.2% in May. Much of this moderation is expected to reflect lower energy prices in June, as gasoline and fuel prices fell by 10% and 6.3%, respectively, compared to May.

Energy prices are still expected to remain high compared to last year, but their contribution to overall inflation should moderate. Meanwhile, food inflation is expected to remain steady at 3.6%, declining only modestly from 3.8% in May.

Excluding the more volatile components, inflation pressures are expected to remain broadly stable.

We expect inflation, excluding food and energy, to remain close to 1.6% y/y, little changed from May, while the Bank of Canada’s preferred core inflation measures are likely to remain consistent with inflation approaching the 2% target.

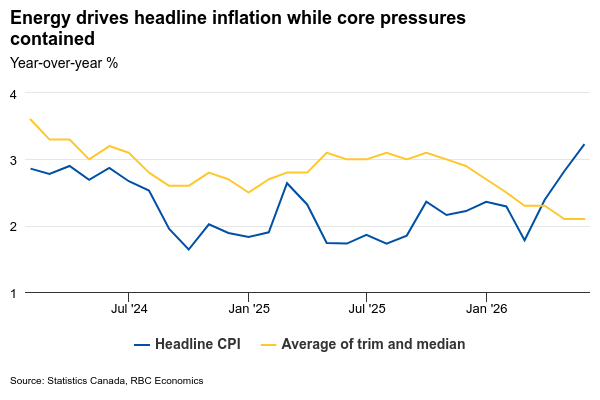

Recent inflation reports continued to point to a divergence between headline and core inflation, with headline readings boosted by higher energy prices, while broader price pressures remained relatively under control.

This distinction is likely to remain central to the Bank of Canada’s assessment of inflation expectations. Policymakers stressed that they are focusing on whether higher energy costs will spill over into broader consumer prices rather than on the direct impact of commodity price movements.

So far, there has been little evidence to suggest such second-round effects, which supports the central bank’s view that core inflation remains consistent with price stability. This is in line with the Bank of Canada’s latest forecasts and our baseline forecast, which assumes inflation will gradually return towards the 2% target over the forecast horizon while the central bank remains in a holding pattern until 2026.

Preliminary estimates from Statistics Canada show a 1% increase in nominal retail sales in June, led by strong sales at gas stations and higher vehicle purchases. After adjusting for price effects, our estimates suggest that retail sales rebounded by about 0.5%, which is consistent with our tracking that household spending remains resilient despite higher energy prices.