Global financial markets entered a riskier macro phase last week, as a disappointing Trump-Xi summit failed to deliver tangible progress on reopening the Strait of Hormuz or easing broader geopolitical tensions. Instead of calming investors, the summit reinforced fears that the global economy may now be entering a prolonged period of structurally high inflation, driven by persistent power outages and tightening financial conditions.

The market reaction was rapid and widespread. Crude oil prices rose again, with Brent once again rising above $109, and WTI closing above $101, as traders increasingly concluded that the world was adjusting to the ongoing Hormuz blockade rather than preparing for its resolution. This reignited inflation fears globally and led to a strong sell-off in sovereign bond markets. US Treasury yields rose alongside Japanese government and Japanese government bond yields, as investors quickly repriced interest rate expectations under a “higher for longer” inflation regime.

The result was a strong “triple-up” market environment dominated by rising oil prices, rising bond yields, and a strong dollar. This combination has been a macroeconomic wrecking ball across global asset classes. Stocks gave up earlier AI gains late in the week, precious metals collapsed under the pressure of rising real yields and a stronger dollar, and global risk sentiment deteriorated sharply as markets wondered how long the current inflation shock could last before something in the global economy finally collapses.

The Trump-Xi summit offers symbolism, not solutions

The Trump-Xi summit in Beijing was supposed to provide markets with a geopolitical release valve. Instead, it provided high-level diplomatic symbolism without resolving any of the structural issues driving the current inflation and energy shock. Investors entered the meeting hoping to achieve tangible progress on reopening the Strait of Hormuz, stabilizing global oil flows, and reducing tensions surrounding the US-Iranian conflict. But by the end of the summit, markets had become increasingly convinced that the crisis could last much longer than previously expected.

On the surface, both sides tried to present the talks in a positive light. Trump stressed that China will significantly increase its purchases of US crude oil and reiterated that the two leaders want to “open the Strait.” The Chinese Foreign Ministry also stated that shipping routes “should be reopened as soon as possible” and called for a “comprehensive and permanent” ceasefire. But the carefully managed language hid a deeper truth: there was no operational framework, no implementation mechanism, and no indication that Beijing was willing to put decisive pressure on Tehran to fully reopen the Strait of Hormuz.

This failure had great significance for the markets. Instead of pricing in diplomatic appeasement, oil traders have returned to pricing in a world where global energy flows are simply reorganizing around ongoing disruption. Trump’s comments about China’s purchases of US oil reinforced the impression that Washington may be preparing for prolonged instability rather than anticipating rapid normalization. On the other hand, investors largely dismissed broader trade announcements that included Boeing jets and soybeans and purchase commitments as superficial key agreements that left the deeper trade and technology confrontation between the United States and China fundamentally unchanged.

Global bond yields explode as inflation fears intensify

Global bond markets witnessed one of the strongest simultaneous sell-offs in months last week, as investors increasingly accepted that the inflation shock linked to the Strait of Hormuz crisis may last much longer than previously expected. As the Trump-Xi summit failed to provide a geopolitical release valve, markets quickly shifted toward pricing in structurally higher inflation, tighter financial conditions, and a prolonged period of high interest rates across the world’s major economies.

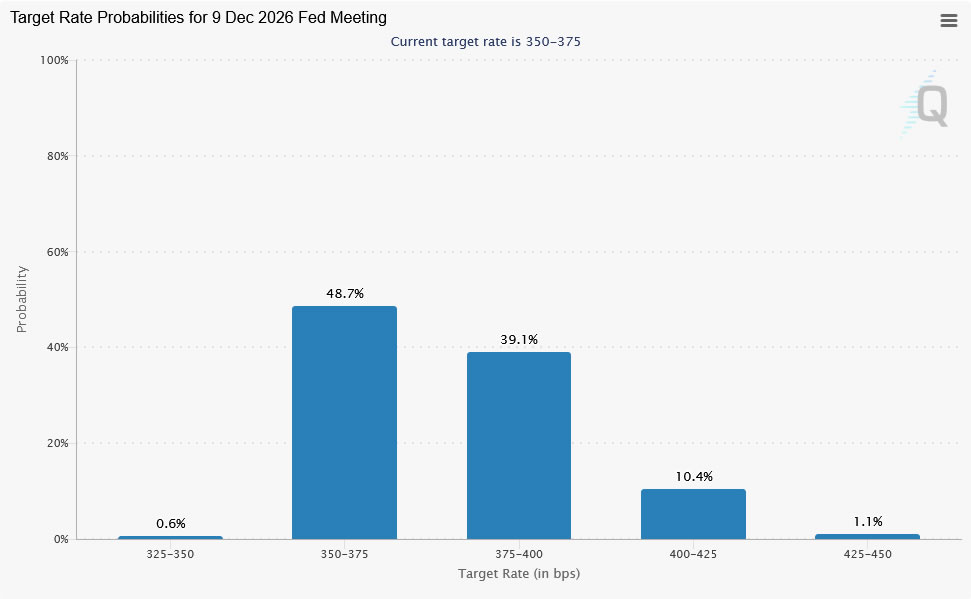

US Treasury yields rose sharply at the heart of the repricing. The benchmark 10-year yield rose through the psychologically important 4.5% level and settled near 4.59%, while short-term yields also rose strongly as traders abandoned expectations of a Fed rate cut. Flat inflation data, rising oil prices, and resilient consumer demand have reinforced concerns that inflation may remain entrenched until next year. Meanwhile, the start of Kevin Warsh’s leadership at the Fed has added another source of hawkish repricing, as markets view the next Fed chair as less willing to tolerate persistent inflation than Jerome Powell. Fed funds futures now indicate a 50% chance of raising interest rates at least once by the end of the year.

The global spread was severe. In the UK, ten-year government bond yields rose to 5.15%, a level not seen since mid-2008, reflecting a toxic mix of energy-induced inflation fears and rising political unease surrounding Prime Minister Keir Starmer’s government. The German 10-year bond yield rose to 3.14%, its highest level since 2011, as the euro zone braced for a renewed inflationary shock despite weak growth momentum. Japan, on the other hand, saw some of the sharpest moves in the world, with the yield on 10-year Japanese government bonds reaching 2.73% – the highest yield since May 1997 due to fears of financial pressures.

The feedback loop related to oil inflation is narrowing

At the heart of last week’s market turmoil was an increasingly dangerous inflation-related feedback loop, which continued to tighten financial conditions globally. With the Strait of Hormuz effectively remaining closed and the Trump-Xi summit failing to provide any reasonable framework for reopening, crude oil prices rose again. Brent crude closed above $109, while WTI settled above $101, reinforcing concerns that the global economy may now be entering a prolonged period of structurally higher energy costs.

The mechanism driving the markets was clear throughout the week. The immediate rise in oil prices intensified inflation expectations in major economies already suffering from difficult price pressures. That, in turn, has led to a sharp rise in global bond yields, as investors quickly price in a world where policymakers must either keep interest rates tight for much longer or tighten them to prevent energy-driven inflation from becoming embedded in wages and broader pricing behavior.

The resulting “triple rally” system – rising oil prices, rising yields, and a rising dollar – has been a powerful tightening force across almost every asset class. Rising yields have boosted the dollar through widening interest rate spreads and safe-haven demand, while at the same time tighter financial conditions have pressured stocks, commodities and precious metals.

The damage spreads across assets across global markets

The combination of rising bond yields, rising oil prices and tightening financial conditions caused widespread damage across global asset classes last week. What initially started as a resilient, AI-driven rally in stocks earlier in the week eventually gave way to a broad risk-off reversal on Friday as markets increasingly struggled to absorb the effects of inflation and structurally high interest rates.

Global equity markets have come under intense pressure, as rising yields have led to a sharp increase in discount rates and undermined valuations, particularly outside the technology sector. The Nikkei 225 fell more than -2% on the week, while Germany’s DAX fell about -1.6% as European markets faced rising energy costs and deteriorating growth prospects. US stocks proved somewhat more resilient due to the ongoing enthusiasm surrounding big tech and artificial intelligence names, but even the Nasdaq gave up much of its previous momentum by the end of the week as Treasury yields accelerated higher. Friday’s sharp sell-off suggests that even AI trading is not completely immune to the tightening pressure generated by the “triple top” system.

Precious metals suffered some of the biggest losses in the markets. Gold fell about -$170 during the week to close near $4,560, as rising real yields and broad dollar strength overshadowed any safe-haven demand generated by geopolitical tensions. Silver fared even worse, suffering a brutal late-week collapse as rising real yields and concerns surrounding China-linked industrial supply chains weighed heavily on sentiment.

Rising yields and risk aversion are fueling a strong dollar rally

The strength of the dollar dominated currency markets last week, as rising Treasury yields, rising oil prices and deteriorating global risk sentiment boosted demand for the US currency. The dollar finished as the strongest major currency by a clear margin, simultaneously benefiting from widening yield advantages, safe-haven demand, and growing expectations that the Federal Reserve may need to maintain restrictive policy for much longer amid persistent inflation pressure.

The dollar’s strength was particularly notable because it occurred alongside weakness in both global stocks and precious metals, highlighting how aggressively markets have prioritized yield and liquidity over traditional inflation hedges. The Canadian dollar finished as the second strongest performer, largely supported by a sharp rebound in crude oil prices and Canada’s commodity-linked exposure to an energy shock. The Swiss franc and yen also outperformed most of their major counterparts as defensive positions intensified late in the week, although both were ultimately overshadowed by the dollar’s overwhelming yield advantage.

At the other end of the spectrum, the British pound was the weakest of the major currencies as investors continued to price in escalating political instability in the UK along with rising financial and energy concerns. The New Zealand dollar and Australian dollar also underperformed as rising global yields and deteriorating risk sentiment put pressure on currencies with high betas closely tied to global growth expectations and Chinese demand. The euro finished near the middle of the pack, supported modestly by higher bond yields and growing expectations that the European Central Bank may eventually need to tighten policy further if energy-driven inflation persists.

Outlook: The “triple top” system may persist until the Strait of Hormuz reopens

The dominant macro theme in the coming weeks is likely to remain the “triple bull” regime of rising oil prices, rising bond yields, and a strong dollar. As long as the Strait of Hormuz remains effectively blocked and global energy supply chains continue to operate under extreme pressure, markets are unlikely to meaningfully reflect the inflation repricing that accelerated last week. .

Oil remains the most important variable in this entire macro framework. Markets will continue to focus on physical shipping conditions rather than political headlines. The UAE’s accelerating efforts to expand the capacity of bypass pipelines through Fujairah highlight how regional producers are beginning to brace for long-term disruption rather than rapid normalization. As long as Hormuz remains restricted, Brent is likely to remain structurally supported in the $100-115 range, maintaining upward pressure on inflation expectations globally.

A decisive breakout of US 10-year Treasury yields above 4.5% could be particularly significant from both a technical and psychological standpoint, as the move signals that markets are beginning to demand a greater premium against inflation risks. If yields continue to rise towards the 4.75%-5.00% region, financial conditions could tighten significantly and put much greater pressure on equity and credit markets globally.

The main turning point in the markets remains remarkably simple: the definite reopening of the Strait of Hormuz.

This is the most important macro domino capable of breaking the current feedback loop of inflation, yield and the dollar. If tanker traffic starts flowing reliably again and the geopolitical risk premium remains embedded in oil collapses, Brent crude could quickly fall by $15 to $20 a barrel, sharply alleviating inflation fears and allowing bond yields to stabilize. But until markets see actual physical normalization – not just diplomatic language – investors are likely to remain defensive and continue to price in persistent inflation risks.

An important counterforce to this broader system remains the AI-driven stock boom, especially in the United States. The resilience of big tech stocks and continued optimism surrounding AI productivity gains so far has helped mitigate broader stock weakness. If the Nasdaq and S&P 500 can quickly resume their record highs after the recent pullback, risk appetite could partially offset safe-haven demand for the dollar. However, even AI trading may struggle to remain completely isolated if oil prices remain high and global yields continue to rise strongly.