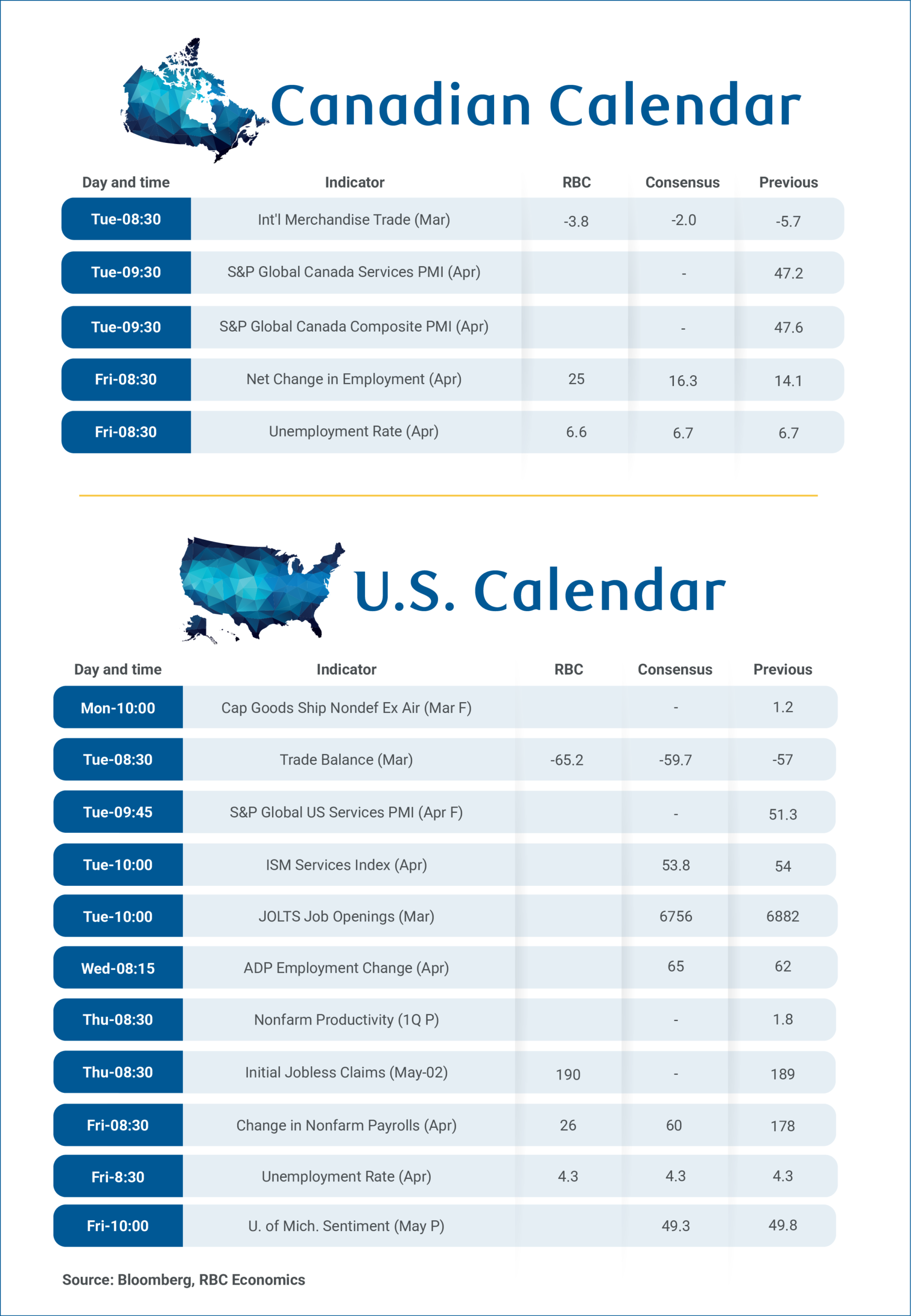

Canadian labor market data for April next Friday will be in focus, and we expect hiring to remain broadly consistent with conditions for each worker gradually improving after an unprecedented decline in labor force growth is brought under control.

We expect to add about 25,000 jobs in April after losses in January and February that only partially recovered in March.

This would leave employment down 70,000 in the first four months of 2026, but would also likely still be enough to push the unemployment rate down to 6.6% from 6.7% – well below the recent peak of 7.1% in August and September 2025.

We’ve discussed before how tough federal immigration restrictions and an aging population have sharply reduced the amount of employment growth needed to push the unemployment rate (the best indicator of working conditions for each worker) down.

Also, the details of recent labor market reports were not as weak as the headline employment growth numbers suggest. especially:

- The vulnerability has been largely contained to trade-exposed sectors with little evidence of its spread. Employment in sectors highly exposed to US trade (with 35% or more of jobs due to demand from the US) has fallen by 3% since February 2024, while other sectors have grown by 1%.

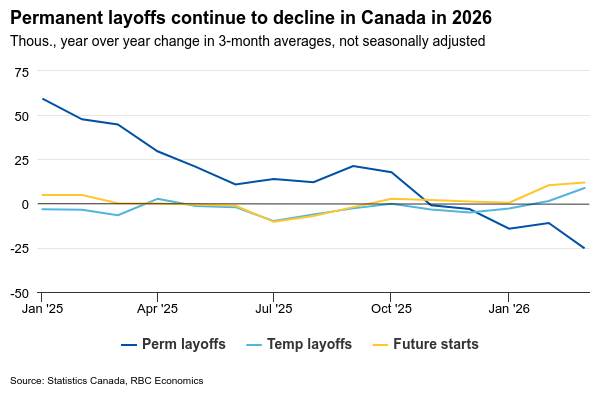

- Permanent layoffs decreased. Job losses in early 2026 were not driven by permanent layoffs, which have declined since October 2025. Instead, the recent increases represent temporary layoffs and future starts (workers who have a future job start date, but are still technically unemployed).

- There are no signs of “hidden” unemployment. The unemployment rate provides a “clean” reading of each worker’s circumstances only if frustrated workers do not give up their jobs or are pushed into part-time work when they would rather have full-time jobs.

- However, broader unemployment measures, such as the R-8, which includes these workers (discouraged and involuntary part-time workers) remain in line with the official rate. Both metrics are relatively unchanged from last year, suggesting that weakness is not hidden beneath the surface.

- Business sentiment is booming. The Bank of Canada’s business expectations survey in February revealed strengthening hiring and investment intentions. Businesses reported plans focused on productivity gains and capacity expansion, reflecting a healthy rebound in household spending in 2025, and a significant improvement in trade uncertainty.

The labor market is not yet strong: the decline in the unemployment rate remains modest so far, and we do not expect the rise in wages in March to be repeated in April.

But our baseline forecast assumes more gradual improvement this year, with the unemployment rate falling to 6.3% by the end of the year even as job growth is historically weaker than usual.

Canadian international trade data has been exceptionally volatile, but the merchandise trade deficit is expected to narrow in March as a 40% rise in oil prices due to conflict in the Middle East pushes the energy surplus higher. We expect exports to rise by approximately 5%, and imports to register a smaller increase of 1.5%, pushing the trade deficit down to -$3.8 billion from -$5.7 billion in February.

We expect US non-farm payrolls to add just 26,000 jobs in March – a figure that, under current conditions, represents break-even growth that has become routine. With the labor supply shrinking, the United States does not need large job additions to maintain a constant unemployment rate. The significant decline in continuing claims between the reference weeks of March and April supports our expectations that the unemployment rate will remain steady at 4.3% in March.