EUR/GBP’s progress this week tells a bigger story than just the strength of the euro. What markets are really pricing in is the fading belief that the Bank of England will need to tighten its policies more than the European Central Bank. For months, the pound has benefited from the assumption that persistent inflation in the UK would eventually force policymakers to take a more aggressive stance than their European counterparts. This narrative is now beginning to collapse.

The first hit came from Energy price collapse After the US-Iranian agreement. Just weeks ago, rising oil prices threatened to spark inflation fears across Europe and the UK. Today, this risk appears much lower. The second blow came from UK inflation report. Headline CPI held steady at 2.8%, below expectations of 3.0%, while core inflation rose modestly to 2.6%, also below expectations. Services inflation remains high, which explains why some policymakers remain concerned, but the overall report failed to deliver the kind of inflation shock that would force markets to aggressively price in further BoE tightening.

The finished piece arrived with Bank of England meeting itself. Although two members voted in favor of raising interest rates, the broader committee showed little sign of shifting in a hawkish direction. More importantly, the bank’s statement emphasized the slowdown in the labor market and signs of economic weakness. This is important because the BoE’s centrists ultimately hold the balance of power. As long as they remain focused on slowing growth rather than sustained inflation, the likelihood of getting enough votes to raise interest rates remains low. Investors conclude so The more likely outcome is an extended pause rather than another move higher.

This leaves EUR/GBP benefiting from increased policy asymmetry. The European Central Bank has already raised interest rates to 2.25%, and while expectations for further tightening remain limited, investors no longer see the Bank of England moving forward decisively. The market is not necessarily becoming more optimistic about the euro. Instead, he became less optimistic about the pound. This distinction helps explain why the EUR/GBP has strengthened even without a major change in the ECB’s forecasts.

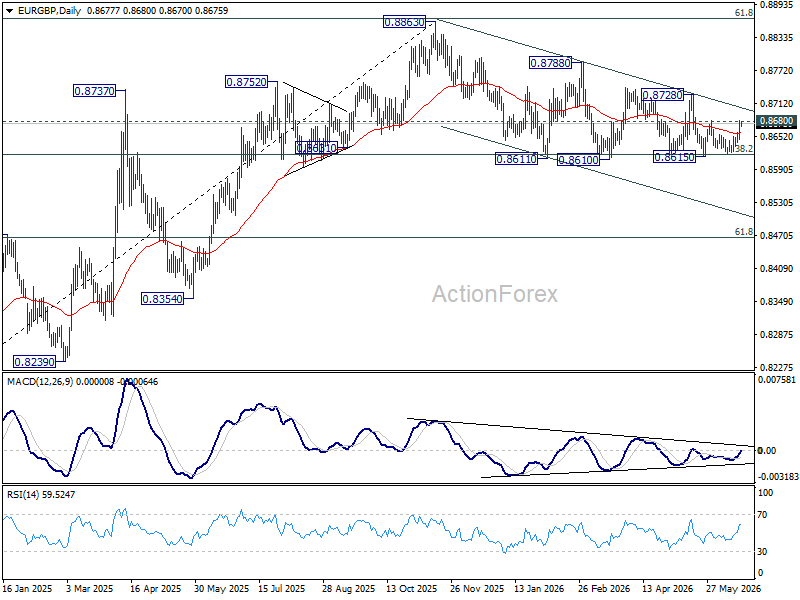

Technically, the crossovers continue to send constructive signals. Repeated defense of the 0.8618 support area, corresponding to the 38.2% retracement from 0.8221 to 0.8863, indicates that buyers are still firmly in control. An uptrend greater than 0.8221 (2024 low) remains in place.

A decisive break above the 0.8680 resistance level will add more confidence to the bullish case and target 0.8728 next. Beyond that, attention will shift back towards the 2025 high at 0.8863. Unless incoming UK data materially changes the outlook for the Bank of England, the balance of risks appears to be tilted towards further EUR/GBP gains in the coming weeks.