Markets enter the Fed’s decision with very little uncertainty about what policymakers might do, but a great deal of uncertainty about what they will signal next. The first meeting of the Federal Open Market Committee chaired by Kevin Warsh is widely expected to result in a fixed federal funds rate of 3.50%-3.75%, with little chance of opposition. Following the departure of Stephen Meiran from the committee, there is no clear constituency in favor of an immediate rate cut, while even hawkish members of the Fed have not indicated that conditions justify raising rates at this stage.

This leaves investors to focus on two issues: the updated bullet chart and Werch’s first press conference as president. In all markets, positioning reflects caution rather than condemnation. Nasdaq futures are modestly higher, but S&P 500 and Dow Jones futures are largely unchanged. The 10-year Treasury yield fell slightly on the day but remained comfortably above 4.43%, while gold continues to trade in a narrow range around 4300. In currency markets, the dollar is moving in a wide range against its major counterparts as traders wait for a catalyst for a directional breakout.

Many aspects of today’s announcement have already been largely understood. The Fed is expected to remove the accommodative bias from its statement, acknowledging that recent inflation developments have reduced the likelihood that the next policy move will be easing. Likewise, the median forecast in the Summary of Economic Outlook is expected to go from one cut this year, as expected in March, to no change through the end of the year. Neither development would be particularly surprising given the recent rise in inflation and the resilience of economic activity.

The real question is whether the Fed is just abandoning its dovish bias or is starting to think about tightening monetary policy again. The answer lies in the distribution of points, not the median itself. If two or three policymakers expect interest rates to rise in the future, markets are likely to dismiss these forecasts as the views of the traditional hawks on the committee. However, if four or more officials place their points above the current policy range, investors may conclude that the Fed is moving beyond its “longer rise” framework and begin discussing the possibility of additional policy tightening.

The other wild card is Kevin Warsh himself. Investors want to know whether the latest inflation pressures are seen as a temporary energy shock or the beginning of a more sustained inflationary cycle in the second round. However, there is a problem. Warsh has long argued that central bankers should communicate less, not more. As a result, investors may find that the new Fed chair provides fewer policy signals than markets are accustomed to receiving.

In foreign exchange markets, the dollar remains caught between competing forces. The Swiss Franc is currently the strongest performer during the week, followed by the Euro and the Australian Dollar. The New Zealand dollar, Canadian dollar and yen lag behind. The pound and the dollar sit in the middle of the rankings. By the time the Fed’s decision is announced, markets will already know the interest rate outcome. What they don’t know is how many policymakers now believe the next step may ultimately be higher. This question may ultimately determine the dollar’s next major move.

Sterling slides as UK inflation fails, but bullish case for GBP/CAD remains intact

Today’s data may delay the rally. Maybe he won’t cancel one. Markets may be backing down on expectations about the Bank of England’s next move, but rising services inflation means tightening monetary policy remains a possibility. The GBP/CAD pair still has two strong tailwinds. The UK’s large yield advantage and the collapse in oil prices continue to support the pair even as the pound absorbs weak inflation data. Read more.

Dow Jones hits record high as lower oil prices offset Fed concerns

The real risk is not today’s interest rate decision. That’s probably how many Fed officials have quietly begun anticipating another rate hike. For now, though, lower oil prices are keeping the Dow Jones index rising solidly. Read more.

US retail sales rose 0.9% in May, indicating resilient consumer demand

High rates did not stop consumers from spending. Strong gains in core and core retail sales suggest that demand remains resilient despite inflation and tightening financial conditions. Read more.

Eurozone core inflation accelerated to 2.6% as services and energy prices rose

Title rose. The basic story just got stronger. Eurozone inflation accelerated in May, but the biggest development was a jump in core CPI from 2.2% to 2.6%, suggesting that core price pressures remain stubborn. Read more.

UK inflation holds at 2.8% as deflation in goods prices offsets services pressures

The Bank of England got some breathing room. Headline and core inflation were below expectations, reducing pressure for an immediate policy response ahead of this week’s interest rate decision. Read more.

Japan’s exports beat expectations as demand for artificial intelligence offsets war-related disruptions

Japan’s export boom appears stronger than it actually is. Key exports jumped 17.0% in May, but volumes rose just 0.5%, suggesting higher prices and a weaker yen did most of the heavy lifting. Read more.

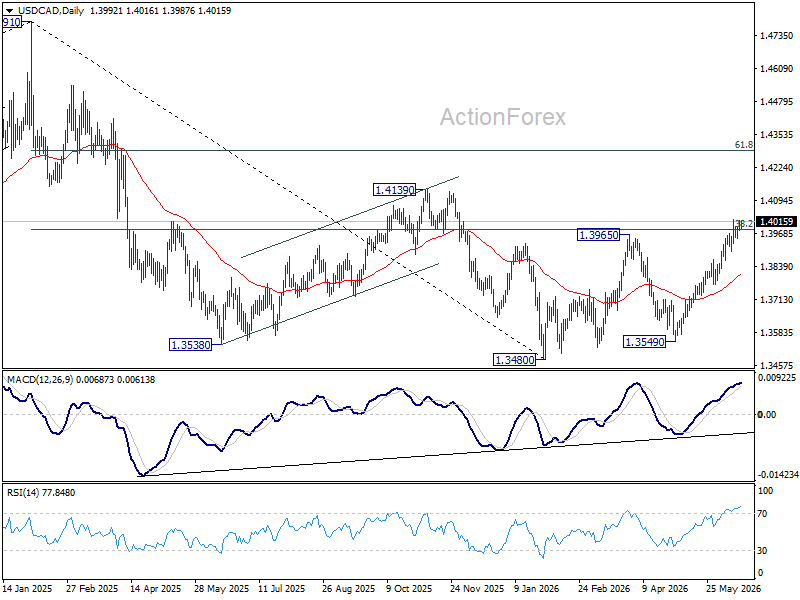

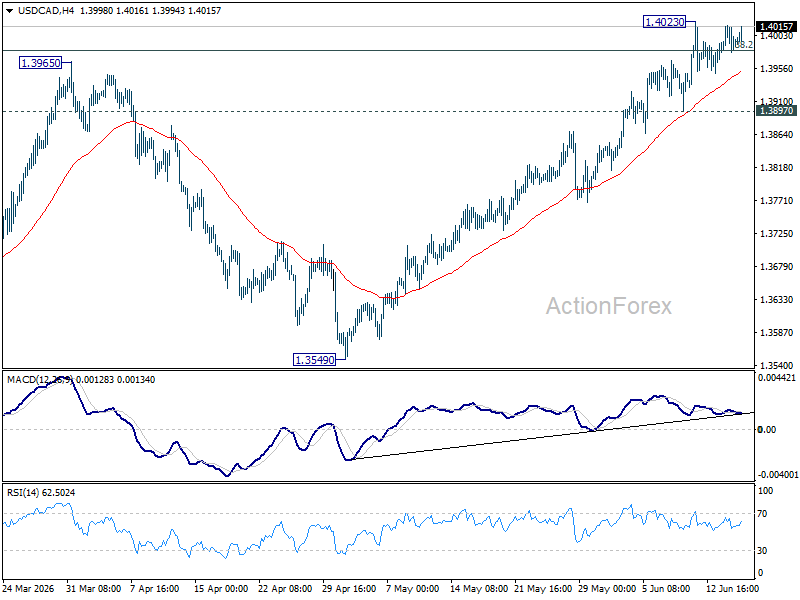

Daily forecast for the USD/CAD pair

USD/CAD remains range bound below 1.4023 and intraday bias remains neutral. Further rise is expected as long as the support at 1.3897 remains stable. On the upside, the sustained breakout of the 38.2% retracement level from 1.4791 to 1.3480 at 1.3981. A decisive break there would carry larger bullish implications and would target the 61.8% retracement at 1.4290 next. However, a strong break of 1.3897 will shift the bias back to the downside for a deeper pullback.

In the bigger picture, price action from 1.4791 is seen as a corrective pattern for the entire uptrend from 1.2005 (2021 low). Rejection of the 38.2% retracement from 1.4791 to 1.3480 at 1.3981 will keep the decline intact, and bring another decline through 1.3480 at a later stage. However, a strong break of 1.3981 would indicate that the decline has completed, setting up further upside to retest 1.4791 instead.