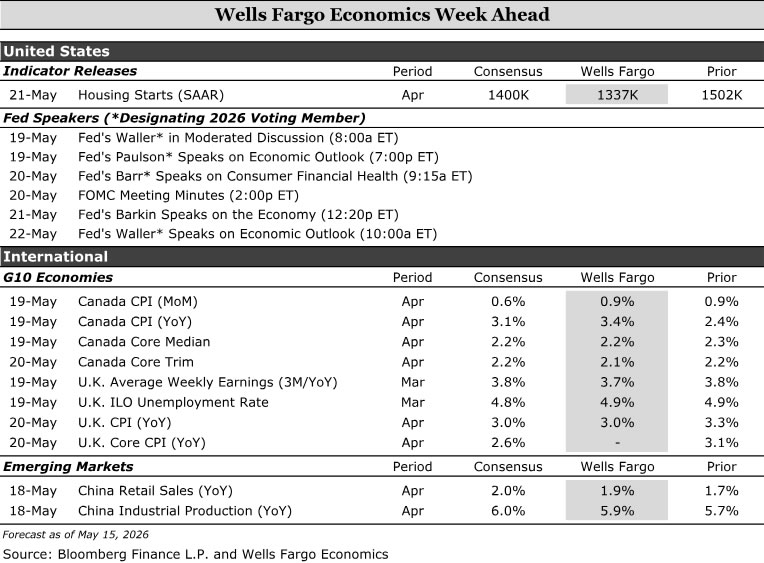

The release of minutes from the April FOMC meeting next week will shed light on how committee members saw the Fed’s next move as balanced between rate hikes and cuts. Meanwhile, US housing data points to a moderate construction backdrop, with a rebound in construction starts in March likely overstating momentum amid a 2.6% YTD decline in permits and continued affordability pressures. In Canada, inflation remains high but mixed, with headline near 3.4% and weaker core measures around 2.1-2.2%, leaving the Bank of Canada cautiously leaning towards further tightening. In the UK, easing labor market conditions – wage growth of around 3.8% and falling job vacancies – contrast with inflation which remains steady at around 3.0%+, leaving policy well balanced. In China, growth remains mixed but steady, with industrial production approaching 5.9% and retail sales around 1.9%, as strong manufacturing offsets weak domestic demand and points to a gradual slowdown ahead.

US:

- FOMC Minutes (Wednesday), Housing Starts (Thursday)

G10 economies:

- Canadian CPI (Monday), UK Labor Market Overview and CPI (Tuesday and Wednesday)

Emerging markets:

- Retail sales and industrial production in China (Monday)

United States next week

FOMC Meeting Minutes • Wednesday

Minutes from the April 29 FOMC meeting will provide details on the Committee’s position ahead of the transition of leadership to Chairman Warsh. Three voters objected to the easing bias that persisted in the April post-meeting statement (even as they approved the decision to keep the federal funds rate unchanged), highlighting growing discomfort with signaling cuts as the default next step.

We’ll look at the minutes to see to what extent nonvoters shared the view that the Fed’s next move is also more likely to be a rate hike rather than a cut. Heading into the April meeting, policymakers received more positive employment data but saw renewed risks to inflation, a dynamic that has since intensified. This will make any discussion of the conditions that would justify raising interest rates more relevant to the current policy outlook. At the same time, Governor Meiran’s departure suggests that the minutes may overstate the degree of cautious support for the committee.

Even with the potential for a tougher tone, we expect the minutes to indicate that most participants still favor keeping interest rates steady for some time while they evaluate how the energy shock will impact inflation and the labor market.

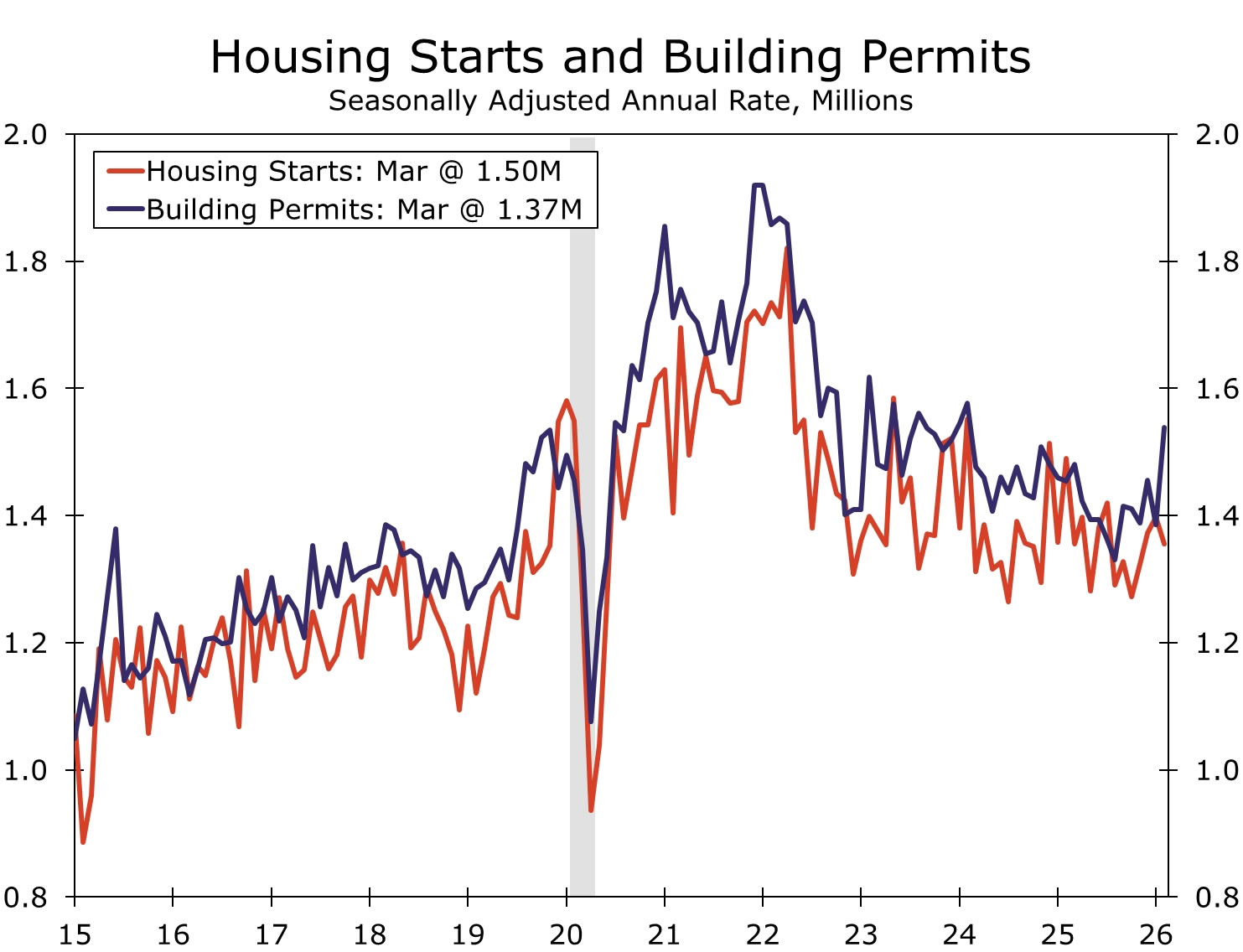

Housing starts • Thursday

Residential construction appears to be trending downwards. The total number of home starts rose strongly during March, with gains in the single-family and multi-family categories. Although the improvement is an encouraging sign that activity is not contracting sharply, our sense is that the monthly gains were mostly a result of the weather-related slowdown in February and greatly overstated the underlying moderating trend in new construction.

So far this year, building permits have trended lower and were down 2.6% year over year in March. The slowdown was most pronounced within single-family households, largely reflecting increased caution on the part of homebuilders stemming from ongoing affordability challenges for buyers, weak new home sales, and high inventory levels. Multifamily permits have outperformed, which we attribute to stable apartment market conditions as well as a slightly lower cost of capital. Taking all these factors into account, we expect the pace of housing construction to decline to 1,337 thousand units in April, below current estimates.

G10 next week

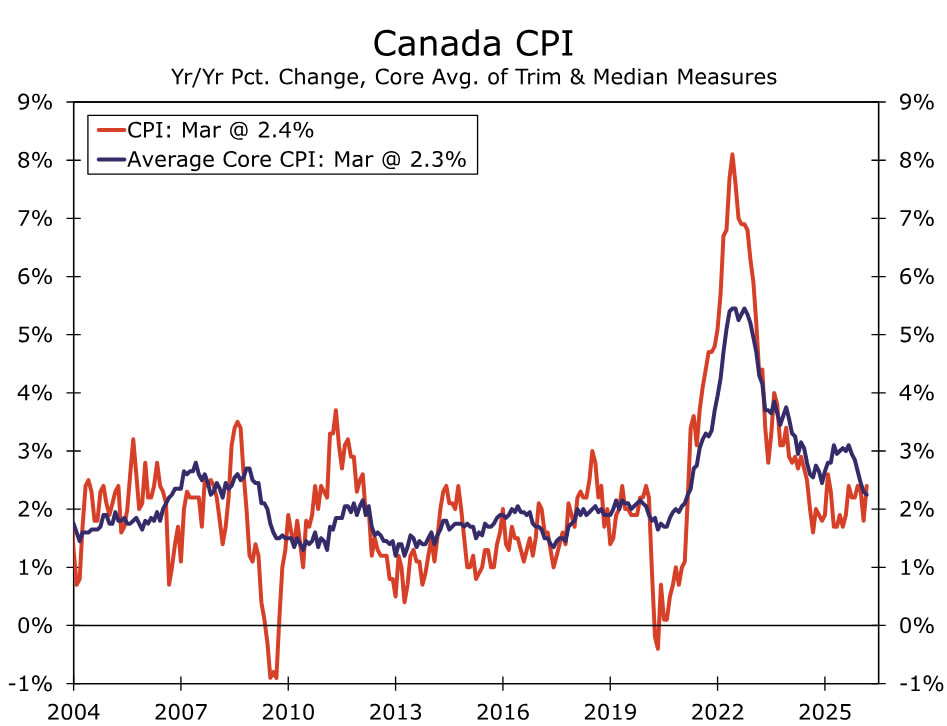

Canadian Consumer Price Index • Monday

We expect headline inflation to rise by another 0.9% m/m in April, after a similar reading in March, taking y/y inflation to 3.4%. Fundamental measures, including average and weighted average inflation, are likely to show another month of decline, supported by favorable base effects. We expect the weighted average inflation rate to decline to 2.1% and 2.2% on an annual basis, respectively. However, April will likely mark an inflection point for core inflation, as core price pressures begin to widen. With headline inflation rising well above the upper end of the Bank of Canada’s target range and core inflation expected to accelerate, we continue to expect the Bank of Canada (BoC) to raise interest rates at its July meeting. The interest rate remains below its estimated neutral range, and we expect downside risks to the Bank of Canada’s outlook to diminish as the July 1 United States-Mexico-Canada Agreement (USMCA) deadline passes without new tariffs, leaving the parties locked in a lengthy annual review process.

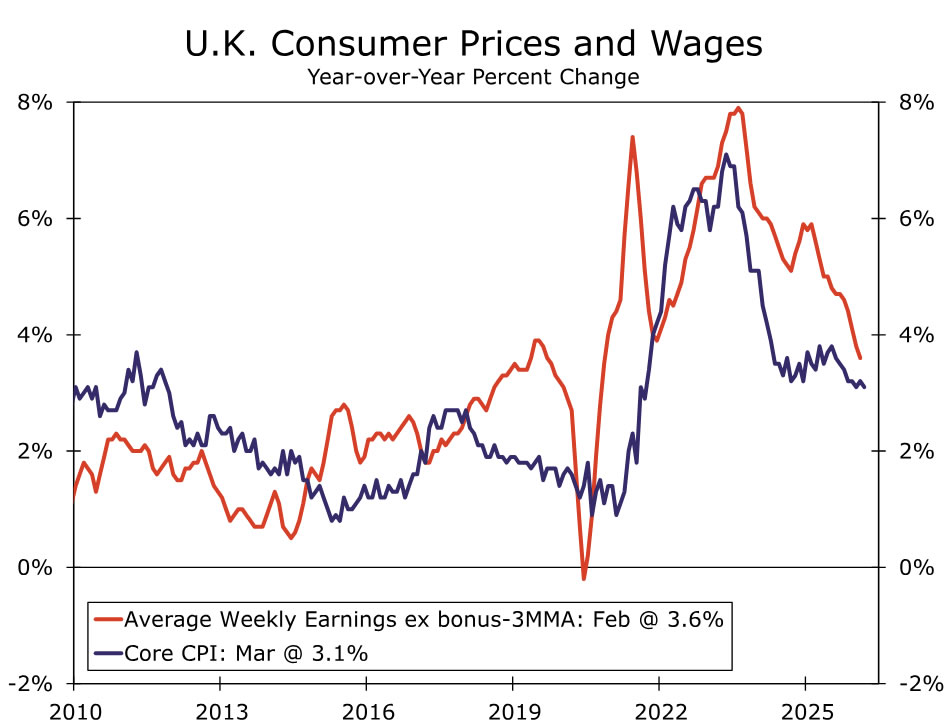

UK labor market overview and CPI • Tuesday and Wednesday

Tuesday’s UK employment and wages data and Wednesday’s April CPI will give market participants a fresh read on wage dynamics and inflationary pressures, as Bank of England policymakers weigh the appropriate response to an energy-induced price shock against a fundamentally weaker labor market. During the three months to February, average weekly earnings growth fell to 3.8% year-on-year, marking the first total pay reading below 4% since 2020. The broader labor market continued to gradually slow, with job openings at 711,000, the lowest level since early 2021, and the number of salaried employees fell by 65,000 year-on-year in the early March estimate. Wage growth is expected to decline slightly, although base effects and the recent increase in the national living wage deserve attention.

Returning to prices, Wednesday’s release follows March’s bullish surprise of 3.3% year-on-year, with services inflation at 4.5% and core at 3.1%. The Bank of England’s April Monetary Policy Report expects headline CPI to decline to 3.0% year-on-year, largely reflecting base effects. So any new upward pressure of energy that appears in the data requires a closer look at the underlying components.

While the 2026 public salary grants and the bulk of private sector wage adjustments were largely completed before the energy shock and labor market downturn were evident, we still see risks of second-round effects tilted to the upside even if they do not play out through the wage channel this year. As energy and fertilizer prices continue to rise amid ongoing conflict, the shift to commodity and food prices calls for a more precautionary stance, in our view. As such, and as we noted in our May International Outlook, we are looking at a 25 basis point rate hike to 4.00% in July, with a further increase in Q4 to 4.25% contingent on developments in the Middle East.

`

`

EM next week

Retail sales and industrial production in China • Monday

April retail sales and industrial production data next week will provide an early read on how the Chinese economy is performing at the start of the second quarter. The Chinese economy got off to a strong start in 2026, beating expectations, although growth has been somewhat uneven. The strength was largely driven by more stable manufacturing output, strong foreign trade performance, and direct fiscal stimulus, while domestic demand remained relatively weak. Up to that point, activity data for March had shown some stability, with industrial production growth flat at 5.7% year-on-year and retail sales growth rising to 1.7%. However, China’s April PMIs suggest that conditions may have eased at the start of the second quarter, as export-led manufacturing resilience contrasted with contraction in services and construction. As such, we expect both measures to grow at a somewhat slower pace in April and look for year-on-year industrial production growth of 5.9% and retail sales growth of 1.9%.

Looking at the bigger picture, we expect recent strength in the Chinese economy to gradually ease in the second half of 2026. Support from fiscal stimulus should fade over time, while rising energy prices and shortages in energy supplies could become more significant headwinds. Accordingly, we look for China’s annual GDP growth to decline to 4.5% in 2026, before slowing further to 4.3% in 2027.