- The US inflation report and Warsh’s testimony will dominate the week’s headlines.

- The dollar will dominate amid a flurry of other US data and tensions in the Middle East.

- Amid new Iranian escalation, China’s GDP highlights second-quarter impact.

- The Bank of Canada is not expected to follow the Reserve Bank of New Zealand by raising interest rates.

- Wall Street gears up for second-quarter earnings season amid AI concern.

Warsh is once again in the spotlight

It’s been more than a month since Kevin Warsh took over as Fed Chairman, but one Federal Open Market Committee meeting and two public appearances later, investors are still trying to gauge where the new chair stands on the hawk-dove scale. Next week will provide another opportunity for investors to weigh Warsh’s views, as he is scheduled to testify at his semiannual hearing before lawmakers in the House and Senate on Tuesday and Wednesday, respectively.

Not that there are high hopes that Warsh will give in to pressure and reveal anything he hasn’t already done on interest rates, but perhaps congressional questioning will at least elicit more from him on his plans to reform the Fed.

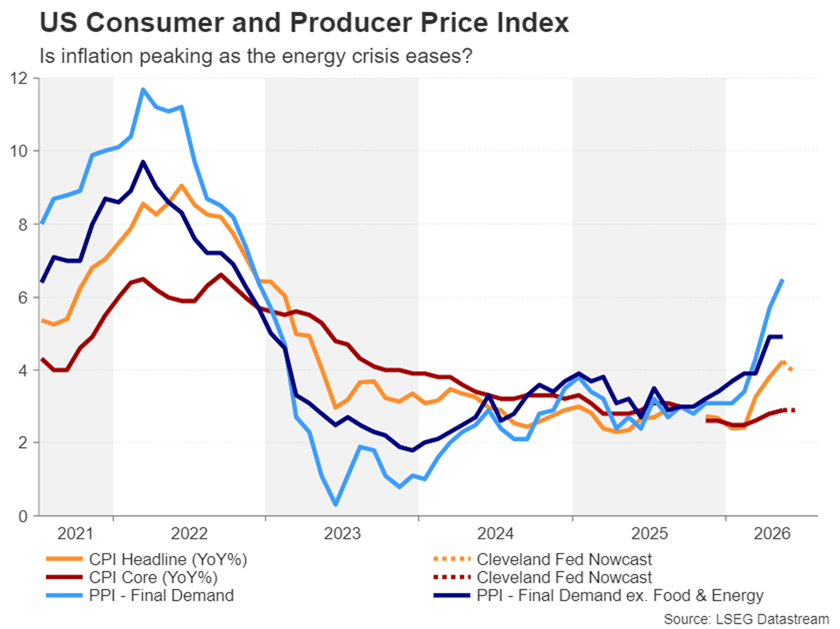

Will the CPI report boost the Fed’s bets?

What could make Tuesday’s testimony particularly interesting is that the latest CPI data is released 90 minutes before the session begins, making it difficult for Warsh to sidestep questions about the U.S. inflation picture.

With CPI and PCE readings rising above 4.0%, it is fair to say that inflation is at serious risk of spiraling out of control. Underlying measures were a bit more tame, but policymakers should be concerned, as the core PCE price index has been trending upward over the past few months, reaching 3.4% in May.

What’s most significant about the current rally is that the Fed has not met its 2% target with any inflation measure since early 2021, hence Warsh’s recalibration of policy priorities. There may be some relief in the June data, as the headline CPI is expected to fall to 3.9%, while the core CPI is expected to remain unchanged at 2.9%.

Policymakers may feel they can wait a while before pressing the rate hike button if inflation appears to have peaked, especially as the energy crisis begins to ease. But with the June meeting minutes acknowledging that price pressures are becoming more widespread and not limited to just energy, any upward surprises in CPI data could revive bets on a July rate hike.

There are a lot of factors driving the dollar

For the US dollar, the biggest risk is a scenario in which the CPI report is hot, but Warsh is repeating in Congress his recent comment that inflation risks have “decreased.” Alternatively, if Warsh does not rule out a rate hike in July if requested, the dollar is well positioned to resume its rise after the FOMC meeting.

In the absence of a clear trend from either the CPI numbers or Warsh’s appearance on Capitol Hill, investors will turn their attention to other releases from the US, of which there are many.

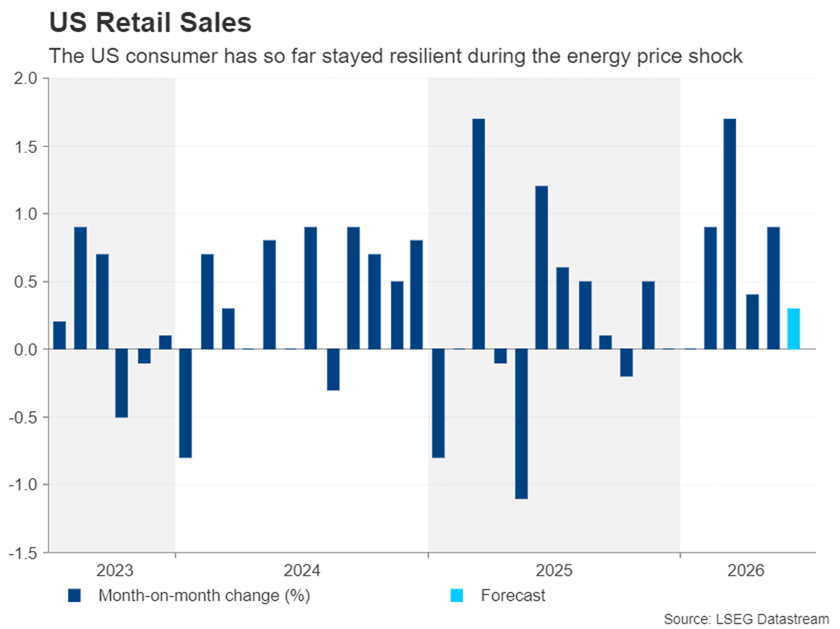

The June Producer Price Index will be released on Wednesday along with the Empire State Manufacturing Index. This will be followed by the Philadelphia Fed’s manufacturing index on Thursday, along with retail sales and pending home sales. More housing indicators are scheduled for Friday, and the week concludes with June industrial production numbers and the University of Michigan preliminary consumer confidence index for July.

Geopolitics and earnings to test the nerves of the market

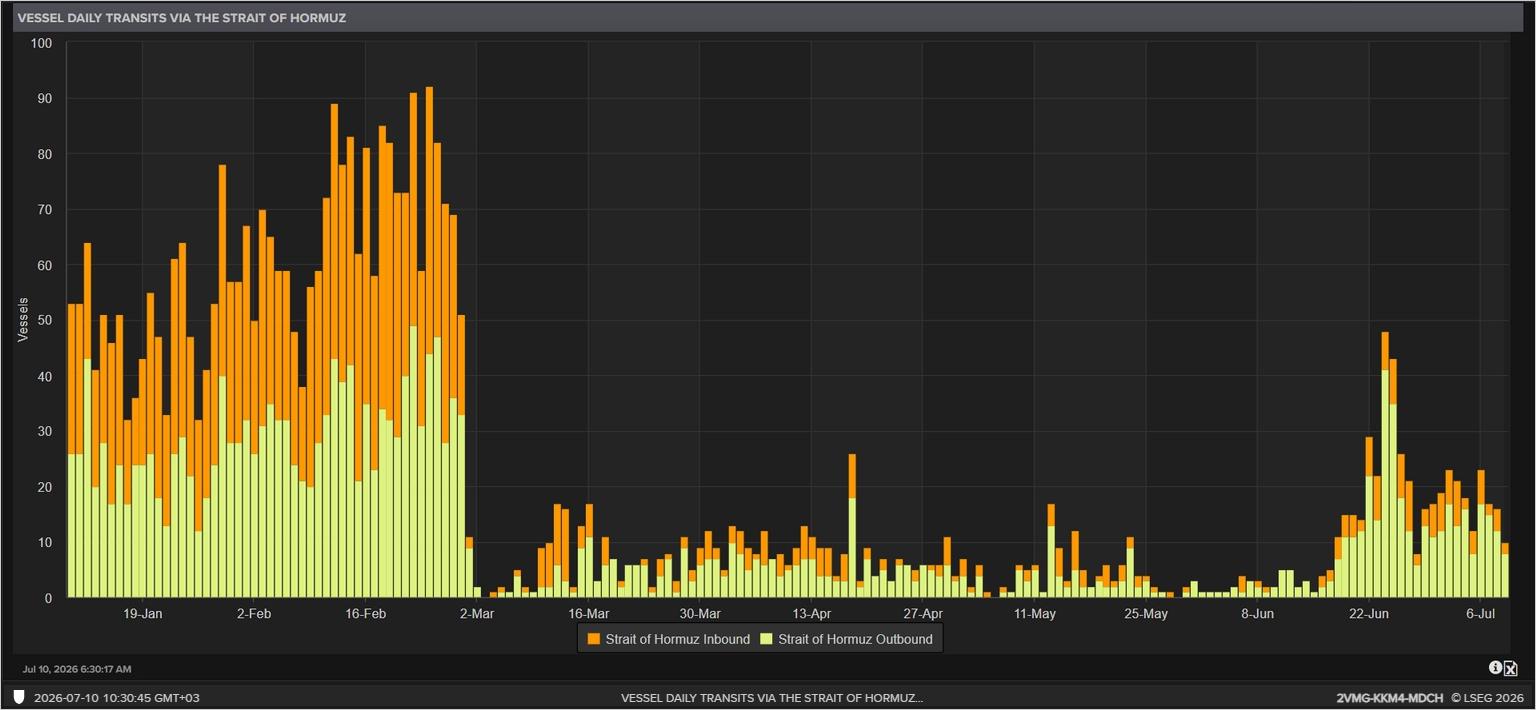

With Fed forecasts likely to increase next week, the situation in the Middle East may increase volatility. In the wake of the escalation that prompted President Trump to declare the end of the ceasefire agreement with Iran, further escalation is very likely as neither side seems to be in a very submissive mood.

But the important thing for markets is whether the Strait of Hormuz will remain open, at least partially, or whether another blockade is possible. The latter would boost both the safe-haven dollar and oil prices, raising expectations of policy tightening for the Fed and other major central banks.

A return to all-out fighting in the region could dampen sentiment in stock markets – where sentiment is already fragile – and distract traders from the second-quarter earnings season, which will peak next week. The focus will be on the big banks, as well as Netflix, but most investors are likely to be primarily concerned about what the earnings outlook holds for the AI sector, with ASML Holding and Taiwan Semiconductor reporting their results.

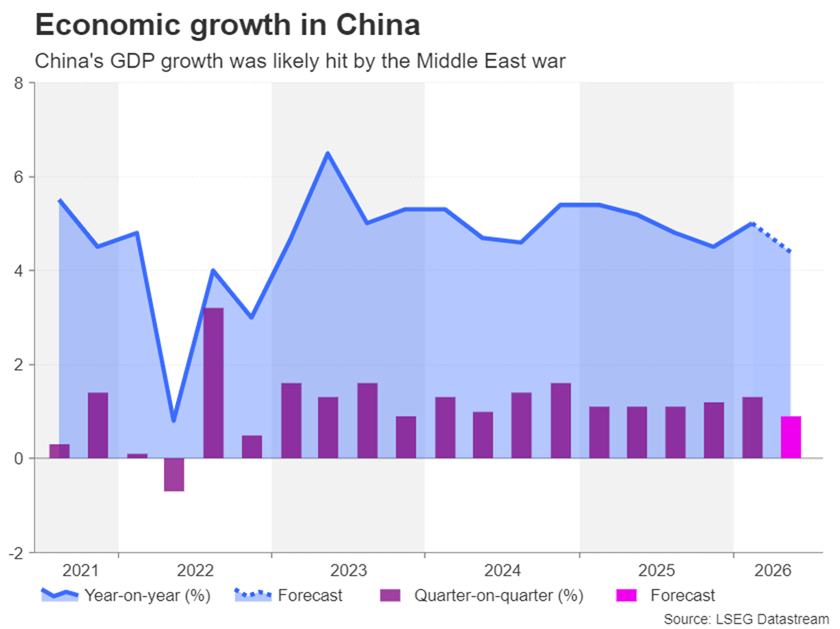

The Chinese economy may have suffered a shock in the second quarter

Although China has been in the eye of the storm of the trade war with Trump, its economy has suffered surprisingly few wounds from all the tariff strikes. However, it may not have been immune to conflict in the Middle East, where economic growth likely slowed in the three months to June.

After achieving strong growth of 5.0% y/y in the first quarter, GDP is expected to rise 4.4% y/y in the second quarter, which would represent the slowest annual expansion since the end of 2022. On a quarterly basis, growth is expected to reach 0.9% q/q – a pace last seen in the fourth quarter of 2023.

However, although the energy price shock may have been the biggest drag, the Chinese economy has been in trouble for a while. The government’s efforts over the past decade to reduce debt have curbed growth. But although these policies have had only modest success in reducing debt, one side effect is that they have caused a real estate collapse.

As a result, consumer demand declined and was unable to recover even with endless support measures by the government to increase spending. The jump in exports this year does not appear to be enough to push overall growth to a higher level. The latest trade figures due on Tuesday will show whether export growth maintained its momentum in June. A day later, GDP data will be released, which will include June readings for industrial production and retail sales.

Stronger than expected GDP numbers could boost risk appetite, although perhaps not by much, while any sharp slowdown could hurt global stocks as well as the risk-sensitive Australian and New Zealand dollars.

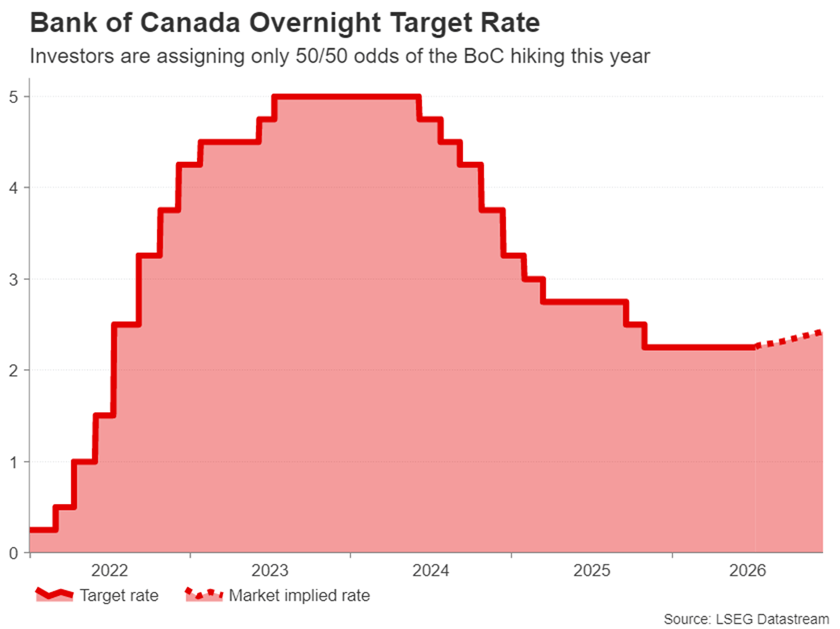

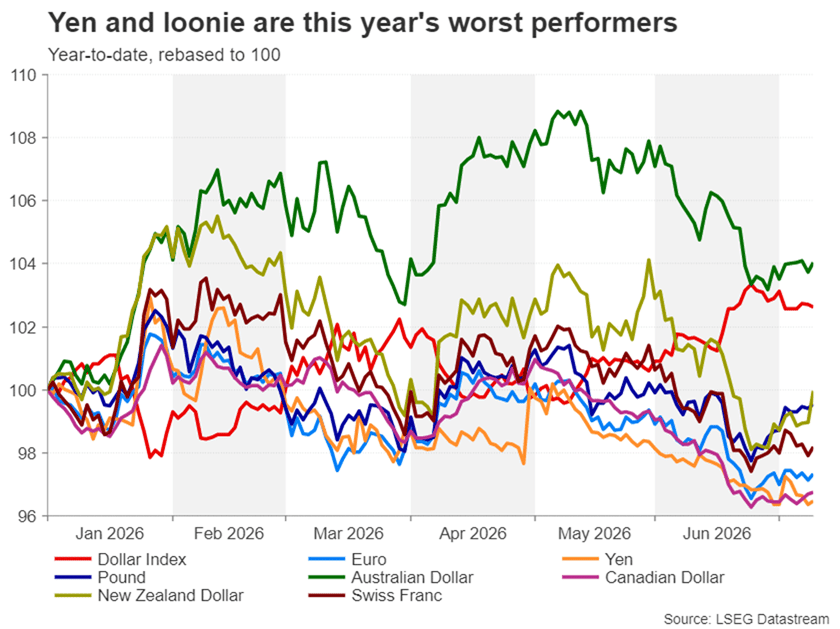

The dovish Bank of Canada is doing the Canadian dollar no favors

Speaking of the New Zealand dollar, the Reserve Bank of New Zealand’s decision this week to raise interest rates and announce more to come gave the currency a big boost. However, the Canadian dollar is unlikely to enjoy similar support when the Bank of Canada meets on Wednesday.

No change in interest rates is expected at the Bank of Canada’s July meeting, as Governor Tiff Macklem remains concerned about the “weak” economy. Despite some improvement in the jobs market and headline inflation rising, growth remains sluggish and core CPI measures remain stable.

Moreover, with oil prices almost erasing the post-war high, even after last week’s surge, the risk of inflation appears to be easing, removing the urgency for policymakers to respond with tougher policy. More importantly, after Macklem’s repeated downplaying of inflation risks, investors see a little more than a 50% chance of a 25 basis point rate hike by December.

On the other hand, it appears that the Fed will raise interest rates at least once in the coming months, and this divergence between the Fed and the Bank of Canada has hurt the Canadian dollar, which has fallen to 15-month lows against the greenback.

The British pound ignores political risks, and the euro and yen struggle

The pound, which has performed on par this month with the New Zealand dollar but not the Canadian dollar, will also attract some attention next week, as investors watch the May monthly GDP estimate on Thursday. UK GDP contracted by 0.1% month-on-month in April when oil and gas supplies in the Gulf remained limited. A further decline in May would raise concerns about the resilience of the British economy as Labour’s Andy Burnham prepares to replace Keir Starmer as prime minister later this month.

Labor MPs have until July 16 to submit nominations for the leadership race, otherwise Burnham will automatically become party leader and prime minister by July 20. Burnham may wait for the official announcement before providing further policy details, leaving sterling vulnerable to speculation until then.

Meanwhile, the Euro has performed poorly against both the British Pound and the Dollar recently. But there could be some support for the single currency on Friday if there is an upward revision to the final Eurozone CPI estimate for June.

The yen is another laggard, and traders will be on high alert for possible intervention by Japanese authorities, as the dollar continues to rise in an unrelenting manner, now approaching the 163 yen level.