- Developments in the Middle East keep the dollar’s range limited.

- But the Fed’s bets on raising interest rates remain high ahead of key US personal consumption expenditures data.

- RBNZ decision and Australian CPI data to test steep implied interest rate paths.

- Accelerating CPI numbers in Tokyo may ease intervention fears.

- You can also click on the Italian, French, German CPI and Canadian GDP numbers.

Geopolitics continues to control the market

After recording its strongest week in two months, the US dollar traded consolidated this week, with the dollar index ranging between 98.80 and 99.40. The dollar started Monday on a strong footing after new tensions in the Middle East, including hostile rhetoric between US and Iranian officials, as well as drone attacks.

However, Iran offered the United States a new peace proposal immediately after the friction, while US President Trump said on Wednesday that they are in the “final stages” of peace talks with Iran. This, combined with news that some ships had successfully passed through the Strait of Hormuz, limited the dollar’s rise and allowed oil prices to decline.

However, although the dollar did not accelerate its advance, it did not slide either. This may have been due to the Fed meeting minutes revealing growing concern among policymakers about inflation getting out of control, with many members becoming more open to the idea of raising interest rates.

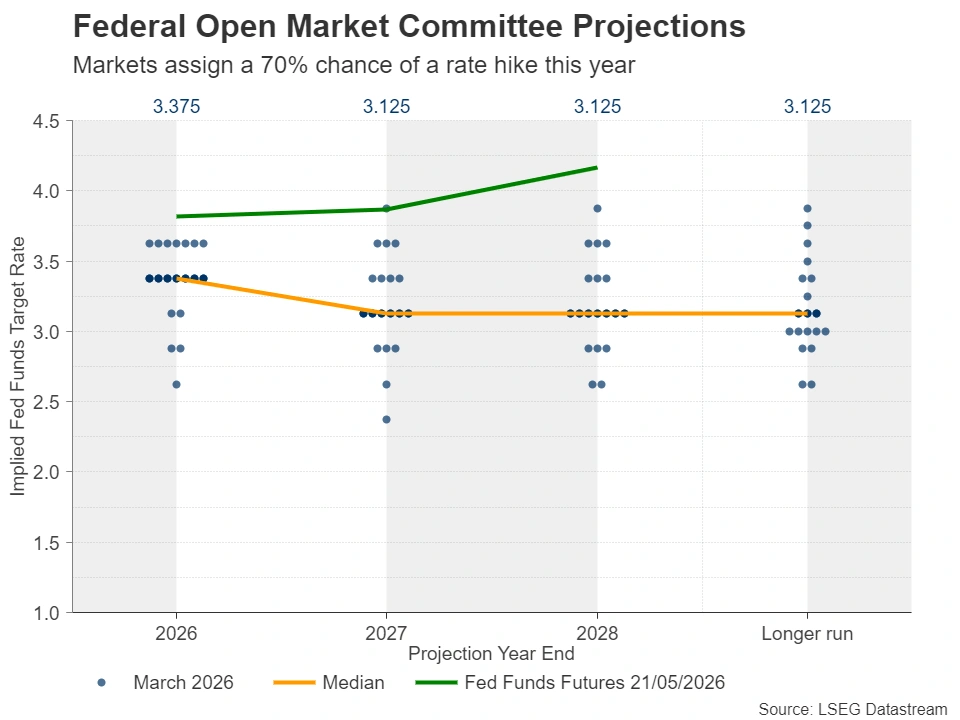

US Personal Consumption Expenditure data is under the microscope amid rising inflation concerns

This allowed investors to maintain their bets on a 25 basis point rate hike for the foreseeable future. Interest rates are due to be fully hiked by March, while there is a strong 70% chance of that happening this year.

Even if oil prices do not rise further, inflation may still be high as annual rates now compare prices to last year’s prices, which were still much lower. Therefore, if the incoming data continues to confirm this, investors may decide to move closer the timing of the interest rate hike.

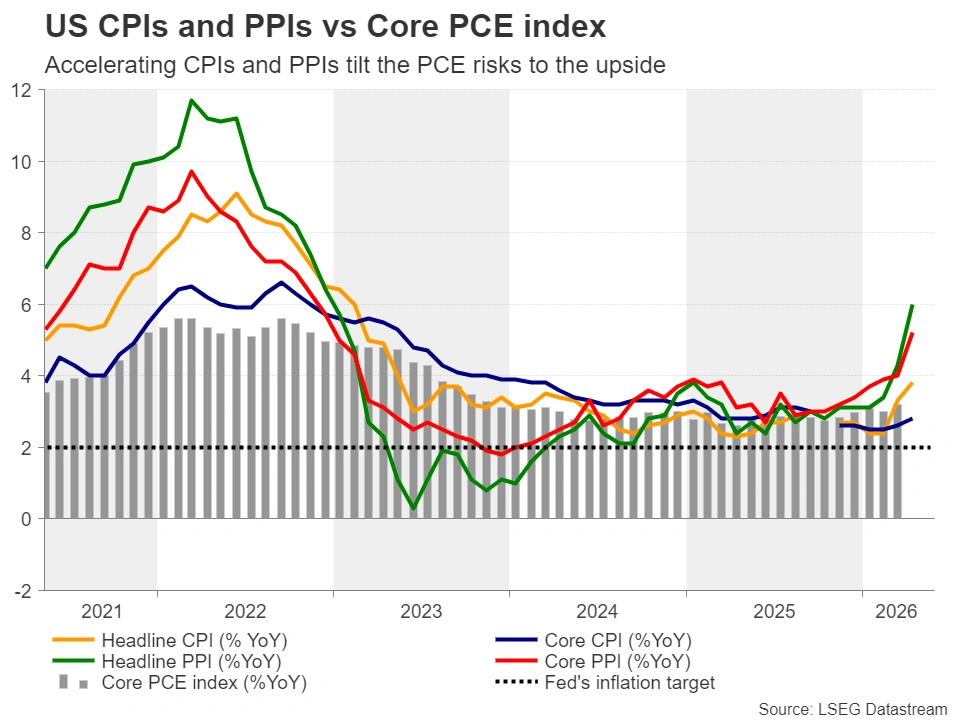

With all that in mind, April’s core PCE index, the Fed’s preferred measure of inflation, comes alongside personal income and spending data for the same month, as well as a second estimate of first-quarter GDP. Given this month’s hotter-than-expected CPI and PPI readings, risks surrounding PCE indicators may be tilted to the upside.

Higher-than-expected PCE rates, coupled with good growth data, could strengthen the case for a rate hike later this year and could allow the US dollar to gain more ground, especially if the US and Iran reach another impasse in peace talks.

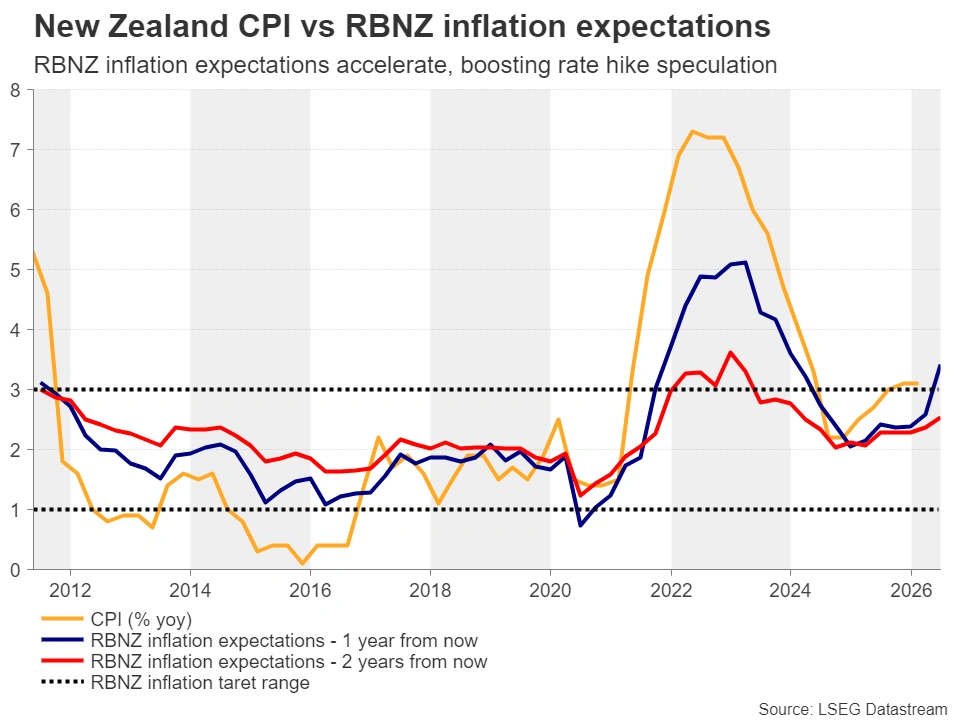

Will the Reserve Bank of New Zealand repeat its hawkish message?

Traveling to New Zealand, the Reserve Bank of New Zealand meets to decide on monetary policy on Wednesday. When they last met, policymakers decided to keep the official interest rate unchanged at 2.25%, but appeared concerned about the impact of the conflict in the Middle East on inflation and economic growth, suggesting they were prepared to act “decisively” if price pressures became more pronounced.

This was interpreted as a hawkish commentary, which combined with accelerating one- and two-year inflation expectations, convinced investors that a three-quarter point rate hike by the end of the year may be justified. Although the probability of action in this group remains low at 25%, it rises to 80% at the July meeting.

Therefore, any further stability accompanied by hawkish language could seal a rate hike deal in July and potentially send the New Zealand dollar higher.

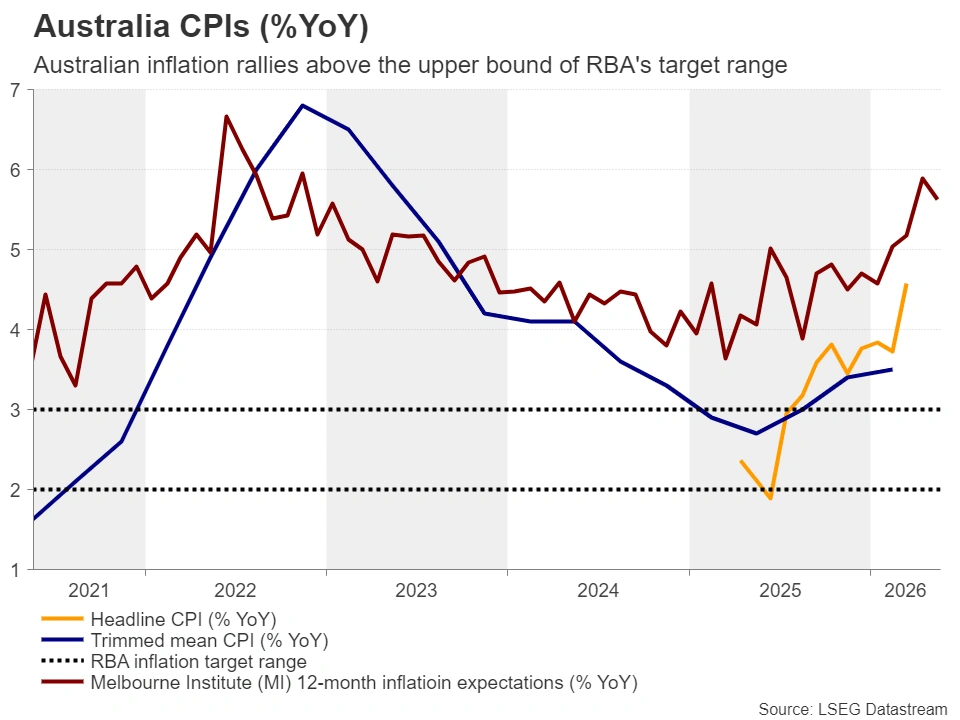

Australian CPI may recharge RBA

Just half an hour before the Reserve Bank of New Zealand’s decision, Australia’s inflation index for April will be released. The RBA has already raised three times, and although it has appeared content to hold off on tightening efforts for a while, another 70 basis points of interest rate hikes are still due by the end of 2026, according to Australian Overnight Index Swaps.

The annual CPI rate for March jumped to 4.6% from 3.7%, and further acceleration could push traders to price in a sharper implied path, which could add fuel to the Australian dollar’s engines. After all, the Reserve Bank of Australia has set an inflation target range of 2% to 3%, and CPI rates are already well above the upper limit.

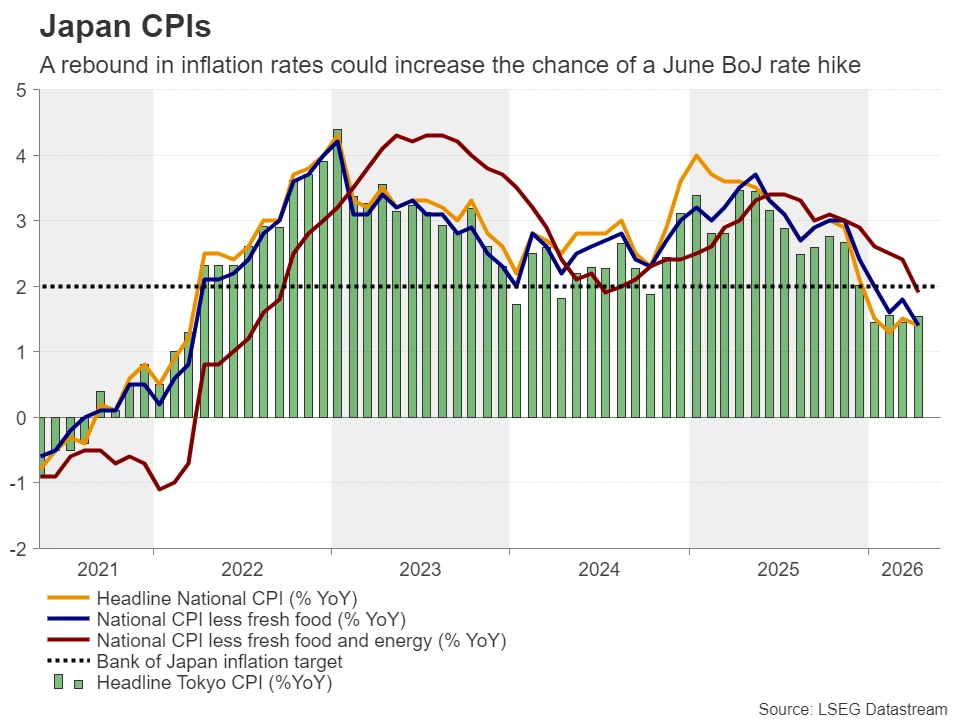

Yen awaits Tokyo CPI data to ease intervention

In Japan, Tokyo’s May CPI report is likely to be accompanied by April industrial production and employment data. Even after Japanese authorities have intervened several times recently, the yen remains on the defensive against its US counterpart, with USD/JPY back in the 158-160 zone, with Finance Minister Katayama inclined to be more vocal about officials’ willingness to intervene.

Accelerating CPI numbers in Tokyo could boost the likelihood of a rate hike by the Bank of Japan at the next meeting and increase the chances of further increases in the coming months. According to overnight index swaps in Japan, there is a 75% chance of a rate hike on June 16, while another possibility is almost fully taken by the end of the year.

Increasing the chances of a rate hike is likely to help the Japanese yen strengthen and possibly reduce the risks of intervention. However, the Bank of Japan may need to meet market expectations if it really wants to help any intervention achieve the desired effect and avoid further declines in the Japanese yen.

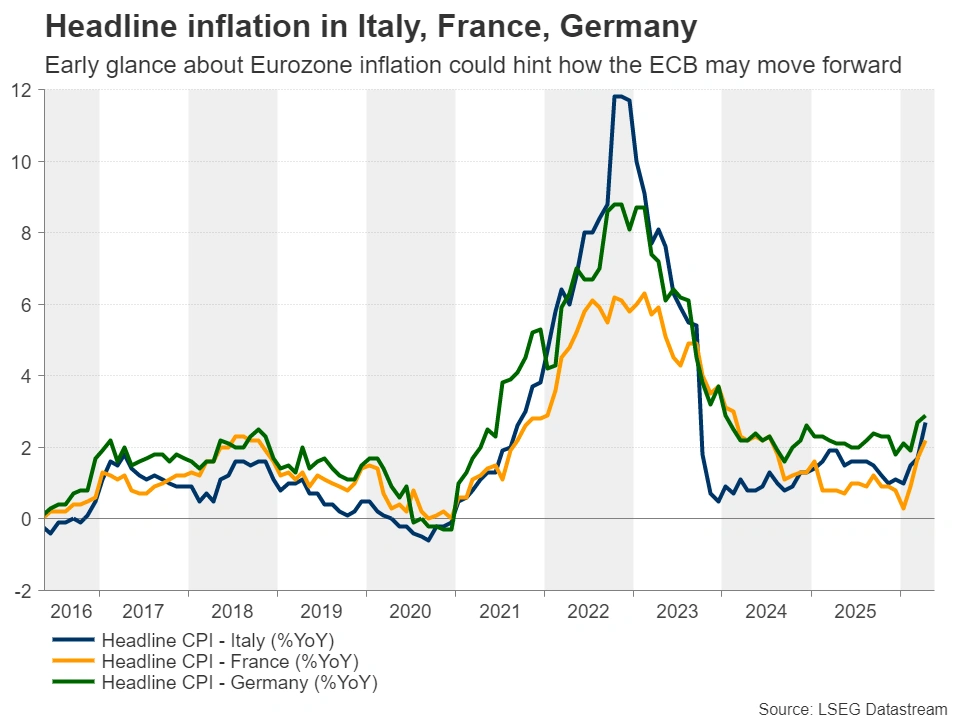

Italy, France and Germany publish inflation data; Canadian GDP is also available

Finally, preliminary May CPI data from Italy, France and Germany on Friday will provide an early gauge of where euro zone inflation may be headed. Eurozone CPI data will be released on Tuesday, June 2. The ECB is now expected to hit the rate hike button at its next meeting, while it may be possible to raise interest rates by a further 40 basis points after that. Growing risks of out-of-control inflation could lead to a tighter interest rate path, but whether this will help the euro move higher remains in doubt.

While the ECB is expected to raise interest rates more aggressively than the Fed, at the same time, the eurozone economy appears to be more severely affected by the current energy crisis and the war in the Middle East. This is evidenced by weak PMIs, with the bloc’s preliminary composite PMI for May slipping into contractionary territory, to 47.5 from 48.8.

Canada’s GDP for the first quarter and March is also on the agenda Friday. The Canadian dollar has held up relatively well amid the geopolitical chaos in the Middle East, perhaps supported by higher oil prices. After all, Canada is the fourth largest oil exporter in the world. Therefore, if data indicates that the Canadian economy has remained resilient amid the turmoil, the Canadian dollar may benefit a little more.