A week that began with optimism about lower oil prices ended with markets focusing on the possibility of renewed Federal Reserve monetary policy tightening. The peace gains from the US-Iran agreement continued to push energy prices lower and helped support risk appetite. But the bigger story was the Fed’s sudden shift toward more hawkish forecasts, which led to widespread repricing across currencies, interest rates and stocks.

The Fed’s updated forecasts have radically changed market expectations. Policymakers now see that interest rates will end the year higher than current levels, effectively signaling one additional rise as the baseline. More importantly, the breakdown of expectations revealed that a large minority of officials actually favor raising interest rates two or more times. Investors quickly adjusted, sharply increasing the likelihood of a September increase and reviving discussions about whether the tightening cycle has actually ended.

The consequences were clear across asset classes. The dollar has strengthened broadly and is now approaching a major long-term technical barrier that could determine its direction for the rest of the year. Treasury markets have priced in higher short-term interest rates, while equity performance has been mixed. The Dow Jones Industrial Average rose to new highs as lower oil prices boosted traditional sectors, but the Nasdaq and S&P 500 remained caught in the consolidation as technology stocks grapple with the prospect of monetary policy tightening. During the week, the dollar led all major currencies, while the New Zealand dollar and the British pound lagged as investors reassessed their respective central bank outlooks.

The Fed is moving from higher for longer to higher again

The decisive market event of the week was not the Federal Reserve’s decision to hold interest rates steady. It was a realization that the central bank was no longer just calling for higher policy for a longer period. Instead, they are increasingly preparing markets for the possibility of a rally again. As part of Kevin Warsh’s first meeting as chairman, the Fed delivered one of its tightest forecast updates since the inflation shock began earlier this year.

The catalyst was a significant reassessment of inflation risks. Policymakers raised their forecast for core personal consumption expenditures inflation for 2026 to 3.6% from 2.7% previously, acknowledging that the energy shock caused by the conflict in the Middle East will leave a more lasting mark on prices than previously expected. While growth expectations were revised only modestly, inflation expectations were raised throughout the forecast horizon, indicating growing concern that price pressures may be more persistent than expected.

The headline was that the average forecast for the federal funds rate is now 3.8% by the end of the year, implying another rate hike. However, the most telling story lies below the average. Nine officials now expect at least one increase this year, while six policymakers already see two or more increases as appropriate. One official even predicted three increases. Meanwhile, Wershe declined to advance his points. This distribution is important because it will only take a modest shift in the coming months for the median forecast to move from one rise to two rises, especially if core CPI inflation and personal consumption expenditures remain high over the summer.

Markets responded by aggressively repricing the path of US interest rates. Futures markets now see September as the most likely timing for the next move (74% chance), while expectations for a second rally have increased sharply. By December, investors are nearly 90% likely to see interest rates at least 25 basis points higher than they are today and more than 55% likely to raise rates twice. The debate has shifted dramatically. Just a week ago, investors were still wondering whether the Fed would tighten monetary policy again. The question today is whether one increase is enough.

The two-year yield says the Fed isn’t done yet

If the clearest message from the Fed came through the dot chart, the clearest confirmation came from the Treasury market. Investors wasted little time adjusting to the Federal Reserve’s tighter outlook, pushing two-year Treasury yields to their highest levels since February 2025. The move represents a complete reversal of expectations that gripped markets just months ago, when investors were still debating how many interest rate cuts might take place this year.

What makes this movement particularly noteworthy is that it was concentrated at the front end of the curve. While two-year bond yields rose, the benchmark 10-year yield ended the week little changed at 4.45%. This difference indicates that markets are not appreciating the loss of control over inflation. Instead, investors are pricing in a Fed that will keep interest rates high for longer and possibly raise them again if inflation remains stubborn. The message is clear and direct: policy tightening, not hyperinflation.

The two-year yield is often viewed as the market’s purest expression of the Fed’s expectations over the next few quarters. Its rise reflects the fact that traders have had to completely abandon their hopes for near-term easing and aggressively price in the possibility of multiple upsides. This shift reflects developments in futures markets, with September becoming the preferred time for the next move and the probability of two rate hikes by the end of the year increasing sharply.

TechnicallyThe near-term outlook in the two-year yield forecast remains strongly bullish as long as support remains at 4.016. The next target comes at a 100% forecast of 3.365 to 4.027 from 3.679 at 4.341. There are two aspects to watch closely. The first is whether the current rally accelerates as yields approach new highs. The second is the market reaction at the expected target of 4.341. Strong momentum at and across this level would indicate growing confidence that the Fed may eventually need to tighten monetary policy more aggressively than currently expected.

Perhaps the bigger picture is more important. The corrective pattern from 5.259 (2023 high) may have already completed in a triangle shape at 3.365. The catalyst for this reversal was arguably the March oil shock caused by the US-Iran conflict, which forced investors to reassess inflation expectations and ultimately paved the way for the Fed’s hawkish pivot.

Structurally, the key level to watch is 4.424, which is the January 2025 high. If this resistance caps the current rally, the market will effectively signal that the Fed only reverses interest rate cuts introduced through 2025. In this scenario, the repricing remains a limited cyclical adjustment, with the longer-term final price remaining anchored around the 3.75%-4.00% area.

but, A decisive break above 4,424 would carry much larger implications. This may indicate that investors are no longer simply pricing in a reversal of last year’s easing cycle, but are starting to question whether the entire phase of policy easing since mid-2024 has been a mistake. Such a move would represent a shift from a temporary inflation shock to a complete macrosystem change, as structurally higher inflation forces the Fed to maintain materially tighter policy for years rather than quarters. This is the dividing line between tight adjustment and the era of real higher interest rates.

The biggest test for the dollar since 2025 has arrived

The dollar index rose sharply after the Fed meeting and reached 101.12 before stabilizing again slightly at the weekly close. The rally carried the index almost exactly to the 38.2% retracement level from 110.17 to 95.55 at 101.13. This is no ordinary resistance. It is a level that could determine whether the dollar’s recovery will develop into a broader uptrend in the medium term.

Technically, the near-term picture remains bullish as long as the support at 99.38 holds. A strong break above 101.13 will confirm the continuation of the uptrend and target the 100% forecast from 95.55 to 100.64 from 97.62 at 102.71 after that.

More importantly, it will strengthen the argument that the rise from 95.55 reflects the broader downtrend from 110.17 (2025 high). This would set up a further rally to the 61.8% retracement level at 104.58, or even further to the ceiling of the long-term down channel (now at around 107).

The dollar is facing a tug of war between the Fed and risk appetite

Traditional headwinds for the dollar will be the return of strong risk appetite following the collapse in oil prices and the gradual normalization of shipping through the Strait of Hormuz. Historically, lower energy prices, improving global trade conditions and rising stock markets tend to encourage investors to move away from safe-haven assets and into higher-yielding or growth-sensitive currencies.

However, this cycle may be more complex. A strong stock market does not necessarily mean a decline for the dollar if it reflects improved earnings expectations and stronger economic growth. Lower energy costs effectively enhance the purchasing power of households and the profitability of companies. As supply chains return to normal and transportation costs fall, companies gain the confidence to invest while consumers increase their spending. The stock market reaching record levels under these conditions would strengthen rather than weaken the fundamental strength of the US economy.

This creates an unusual policy dilemma for the Federal Reserve. If geopolitical relief accelerates an economy that is already expanding at a robust pace, the output gap could narrow further, and pressures on the labor market could intensify. At this point, the challenge for the Fed will no longer be balancing growth against inflation. Instead, the focus will shift towards preventing stronger demand from sparking a second wave of core inflation, especially in the services sector. Such an outcome would strengthen the case for additional tightening and provide continued support for the dollar.

For now, the dollar appears to be stuck in a tug of war between improving risk sentiment and rising Fed expectations. The decisive factor in the coming months is likely to be the expansion of local services. If lower oil prices lead to lower headline inflation but services inflation remains stubbornly high, markets may conclude that the Fed needs to remain hawkish despite the improving geopolitical backdrop. In this scenario, the dollar may continue to strengthen even as global risk assets perform well.

Technically, the Dow Jones uptrend resumed last week and almost reached a record high. While it is possible to see some near-term consolidation, the outlook will remain bullish as long as the support at 49,940 holds. The next target is a forecast of 61.8% from 36,611 to 50,512 from 45,057 to 53,648.

While the Nasdaq rebounded last week, the uptrend is stalled well below the record high of 27,190. The near-term outlook remains neutral for more consolidations first. However, in the event of another decline, the downtrend should be contained by a 38.2% retracement from 20,690 to 27,190 at 24,707. A break of 27190 is still expected to resume the larger uptrend, but later.

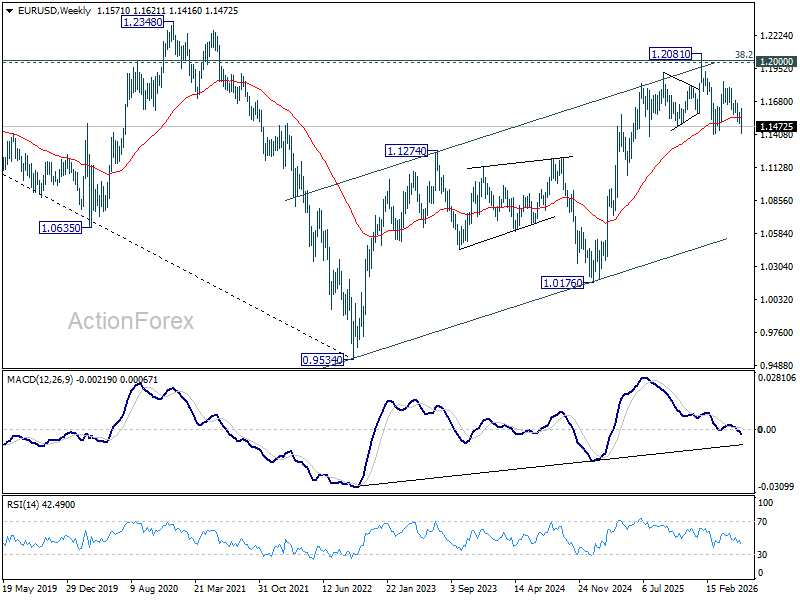

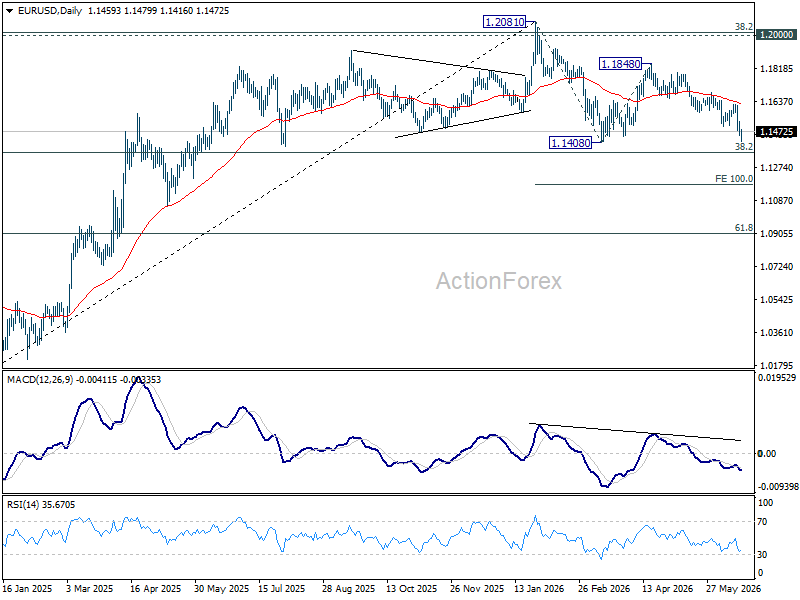

Weekly forecast for EUR/USD

Immediate focus is now on the 1.1408 support level for EUR/USD after last week’s decline. A strong break there would resume the full decline from 1.2081 and target the 100% forecast from 1.2081 to 1.1408 from 1.1848 at 1.1175. On the upside, support above 1.1499 turned resistance will shift the intraday bias to neutral again first. However, the outlook will remain slightly bearish as long as resistance remains at 1.1621, in case of a recovery.

In the bigger picture, focus is back on the 38.2% retracement level from 1.0176 to 1.2081 at 1.1353. A decisive breakout there would revive the medium-term bearish trend reversal case after the rejection of the 1.2 key cluster resistance level. Further decline we should see to 61.8% retracement levels at 1.0904. However, a strong bounce from 1.1353, followed by a break of resistance at 1.1621, will sustain the upside in the medium term.

In the long-term picture, the 38.2% retracement from 1.6039 to 0.9534 at 1.2019, which is close to the psychological level of 1.2000 is key to the outlook. Rejection at this level would keep the multi-decade downtrend from 1.6039 (2008 high) intact, and keep the outlook neutral at best. However, a decisive break of 1.2000/19 would signal a reversal of the long-term upside trend, targeting the 61.8% retracement levels at 1.3554.