At first glance, the Euro appears to be in good health this week. The dollar is falling, oil prices are collapsing, and risk appetite is rising again as markets price in the possibility of a detente between the United States and Iran and the reopening of the Strait of Hormuz. But amid the broad dollar sell-off, the euro is quietly losing two very important battles – one against the pound, and the other against the Swiss franc.

The battle against sterling is fundamentally about the credibility of growth. The slowdown in Europe looks uglier than the slowdown in Britain. The euro zone composite PMI collapsed to 47.5 in May, the weakest level in 31 months, with services collapsing to 46.4 and manufacturing momentum fading quickly. The UK was also weak, with the composite index falling to 48.5, but the details are very important. British manufacturing held steady at 53.7, the strongest reading in four years, while factory output improved to 52.4. In other words, Britain still looks like an economy that is slowing and headed for a soft landing. The eurozone increasingly looks like a region drifting toward recession, with inflation problems still unresolved.

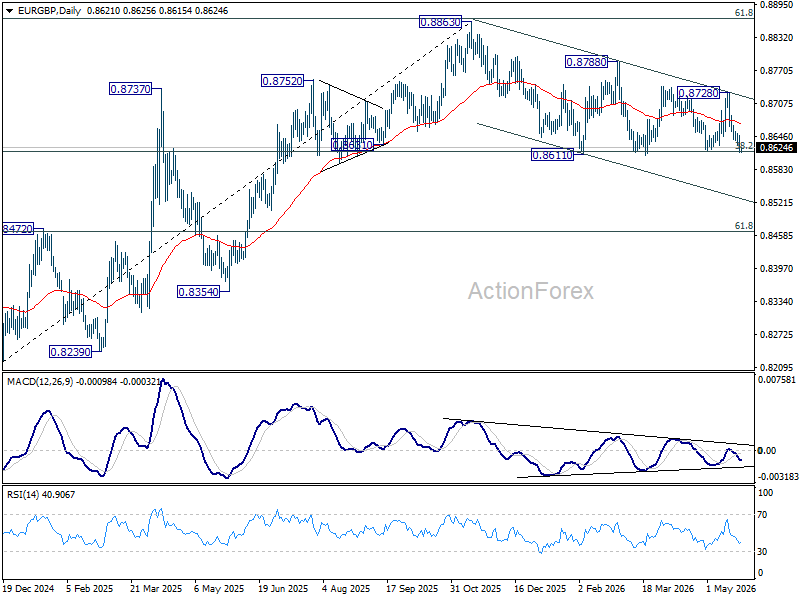

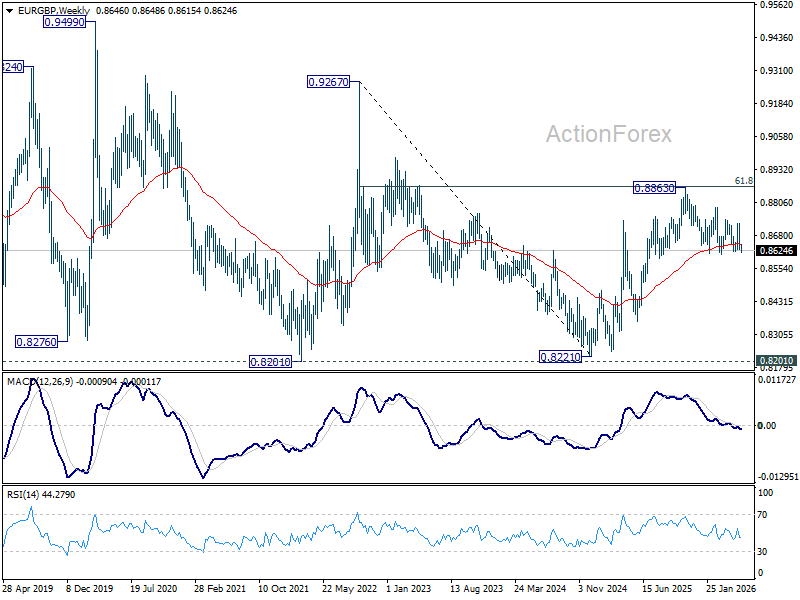

Markets are beginning to reflect this divergence more strongly in the EUR/GBP pair. The pair has now returned to pressure on the critical Fibonacci support area of 0.8618, a 38.2% retracement from 0.8821 (2024 low) to 0.8863 (2025 high).

A decisive breakout there would also push the pair strongly below the 55 W EMA {now at 0.8649). This would reinforce the possibility that the entire rally from 0.8821 has already reached 0.8863 after rejection near the key 61.8% retracement at 0.9267 (2022 high) to 0.8821 at 0.8867. In this scenario, deeper losses towards the 61.8% retracement levels from 0.8821 to 0.8863 at 0.8466 should follow.

The battle against the Swiss franc is completely different. Here, the problem is not growth, but revenues and oil. As markets increasingly price in de-escalation in the Middle East, oil prices fall sharply and global bond yields decline. Ironically, the same “peace yields” that are helping global stocks are also boosting the Swiss franc because lower yields reduce the carry advantage that has been supporting the EUR/CHF pair.

Technically, the rejection of EUR/CHF at the 55 EMA (now at 0.9164) reinforces the near-term bearish outlook. The bounce from 0.8979 should complete at 0.9264, while the broader downtrend remains intact below the bearish 55W EMA and medium-term trendline resistance.

A retest of 0.8979 is likely next, and a strong break there would resume the broader decline from 0.9928, extending the long-term downtrend that started from the 2018 high of 1.2004.