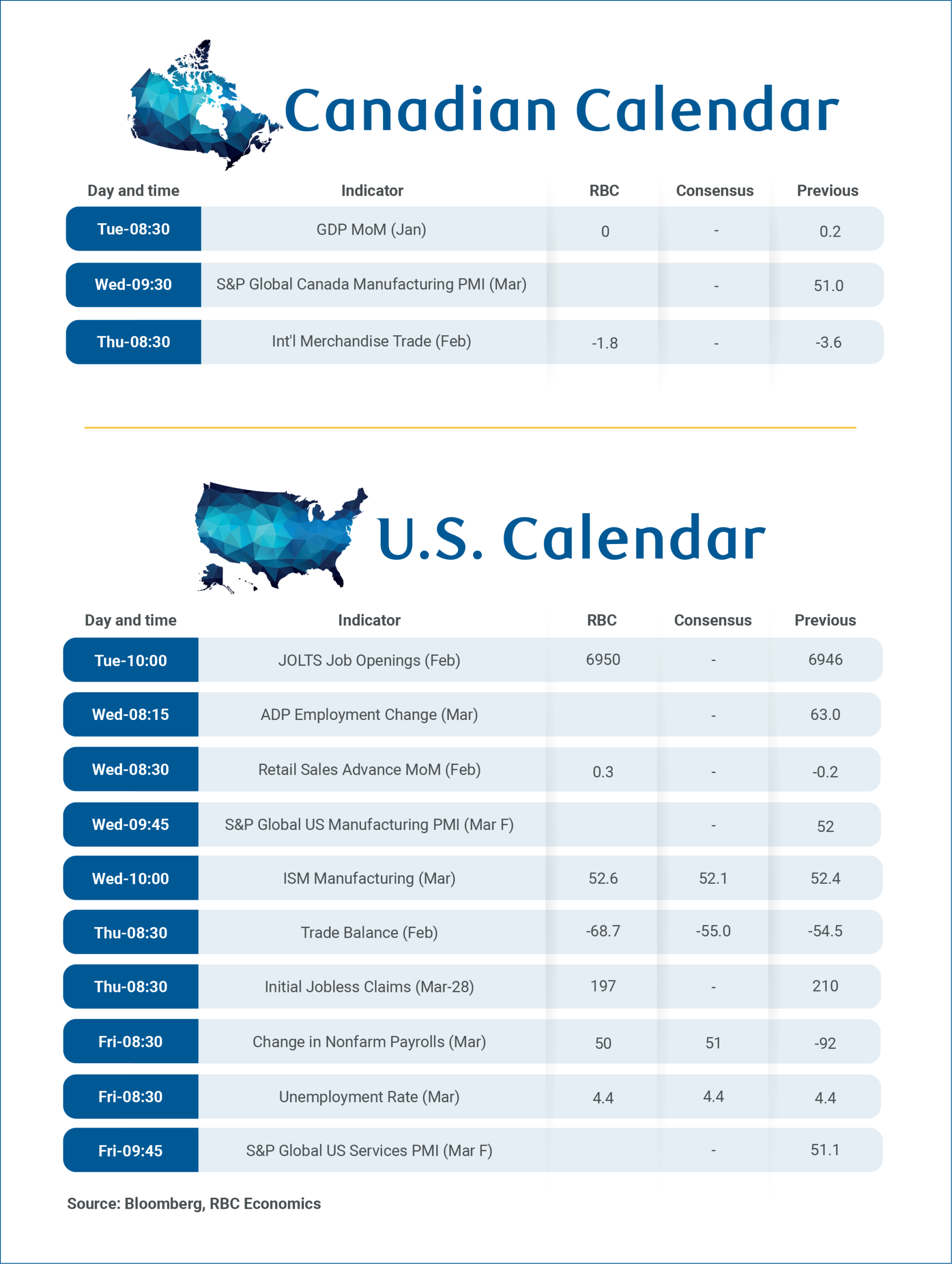

Canada’s January GDP on Tuesday and February trade data on Thursday will provide further clues about the economy’s path in early 2026.

In line with Statistics Canada’s advance estimate, we expect GDP growth to slow to a flat level in January after rising 0.2% in December.

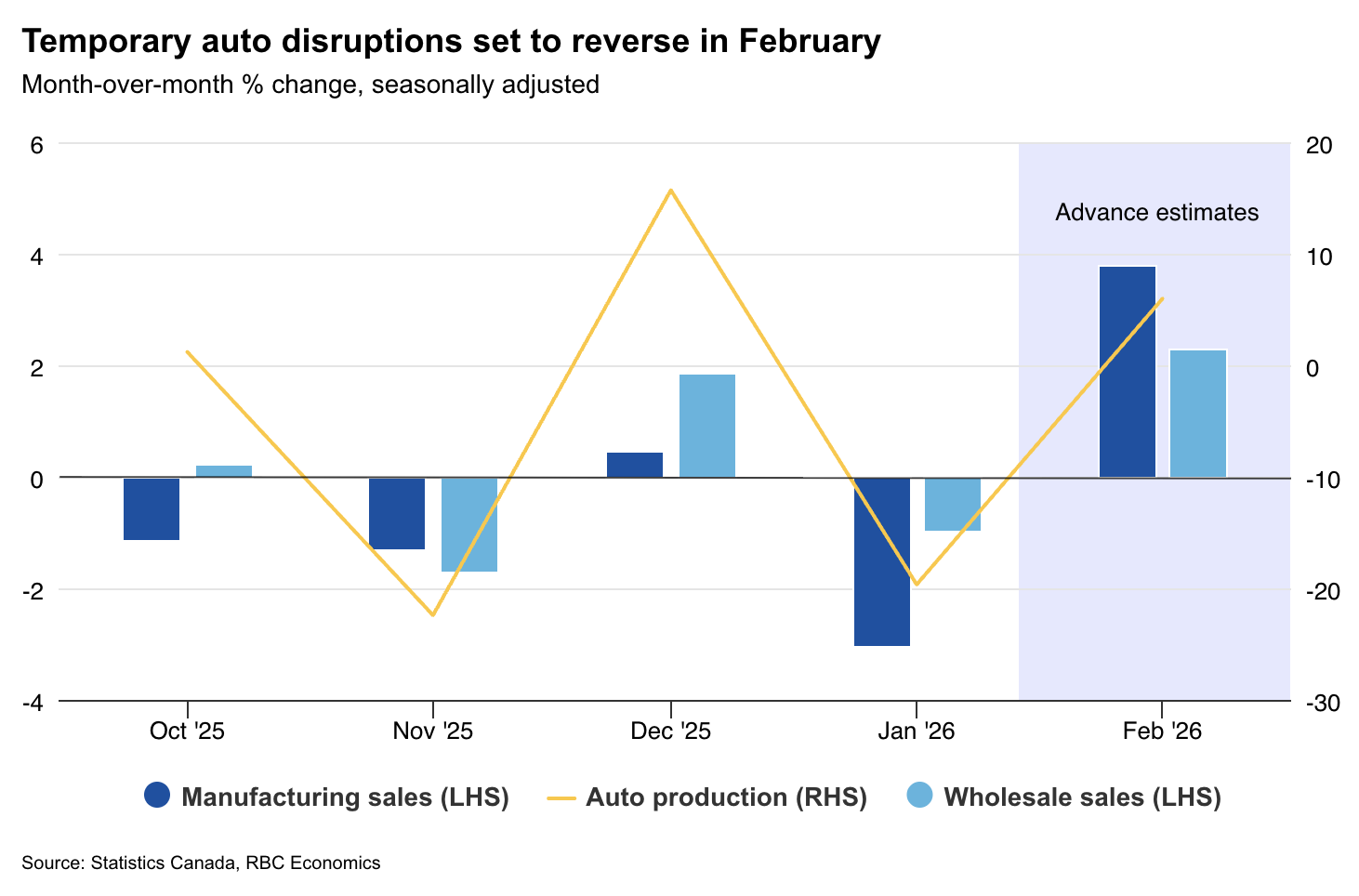

The weakness was concentrated in the automotive sector, where production disruptions at Ontario plants led to a decline in manufacturing and wholesale sales of 3.9% and 1.5%, respectively. However, early indicators point to a partial recovery in February as unrest subsides.

Real estate agent and brokerage services also weakened, as unusually severe weather discouraged home resales in January. Strength in the energy sectors offset these declines, with Alberta’s unconventional oil and mining production (excluding oil and gas) rising modestly after contracting in December. Retail sales rose 1%, reflecting resilient household spending.

February indicators point to a partial recovery

Spending flexibility appears to have extended into February. Early indicators including our tracking of RBC card spending data, as well as Statistics Canada’s advanced retail sales estimates (0.9% nominal increase) point to improvement.

Other advanced industry estimates also showed recovery. Manufacturing sales rose 3.8% in nominal terms, according to Statistics Canada, driven by strength in transportation equipment and food product manufacturing. Wholesale sales rose 2.3%, similarly supported by higher sales of automobiles and spare parts. Housing-related activity will likely remain weak in February as home sales remain weak.

The Bank of Canada flagged downside risks to its 1.8% annual GDP growth forecast for the first quarter at its March meeting. After a weak January, an improvement in activity in February and March and a decline in vehicle breakdowns should leave growth balanced and in line with our expectations of a modest increase.

For February international trade data, we expect Canada’s trade deficit to narrow from $3.6 billion to $1.8 billion driven by a partial recovery in auto exports and higher oil prices. The deficit is expected to continue to shrink in March after conflict in the Middle East sent oil prices sharply higher.

We expect next week’s US March payrolls report to show a 50K increase in hiring, driven in part by the end of the nurses’ strike. The unemployment rate is expected to remain steady at 4.4%, as layoffs decline and initial jobless claims stabilize.