The market narrative has flipped again, and risks are rising. The sudden shift in the Strait of Hormuz…From “open” briefly to back under strict military control within 24 hours– Highlight the fragility of the current ceasefire. What initially looked like the beginning of de-escalation quickly turned into uncertainty, forcing investors to reassess whether the “peace trade” was premature, as the crucial deadline approached.

After Iranian officials initially announced that the strait was fully open to commercial shipping, the situation turned sharply. Military control was re-established, and reports of direct confrontation – including incidents involving merchant ships – ended any assumption of safe passage in the near term.

At the heart of the confrontation lies the collapse of trust between Washington and Tehran. The United States maintained its naval blockade of Iranian ports, insisting that it would remain in place until a broader agreement was reached. In contrast, Iran framed the blockade as a violation of the terms of the ceasefire and responded by tightening control over the strait, linking any reopening of the strait to the restoration of “full freedom of navigation.”

It created this dynamic deadlock Which complicates the prospects for future talks. While reports indicate that another round of negotiations could be held on Monday, there is still no official confirmation. Even if the talks continue, they are likely to unfold under great tension, as both sides enter from hardened positions.

The broader risk is that time is running out. If no progress has been made before The ceasefire ends on April 22. The probability of renewed hostilities is rising sharply. This may include a return to direct military confrontation or escalation at strategic checkpoints such as Hormuz.

For markets, this makes the coming days crucial – not just for geopolitics, but for the direction of oil, inflation expectations, and global risk sentiment.

In this environment, Oil remains the final signal. Their ability – or failure – to unravel decisively will determine whether markets continue to tilt toward diplomacy or begin to price in a return to conflict. As the ceasefire approaches, this signal will become increasingly important. Meanwhile, key technical levels across major assets will help guide traders in assessing whether fundamental market sentiment is indeed shifting, or simply reacting to major volatility.

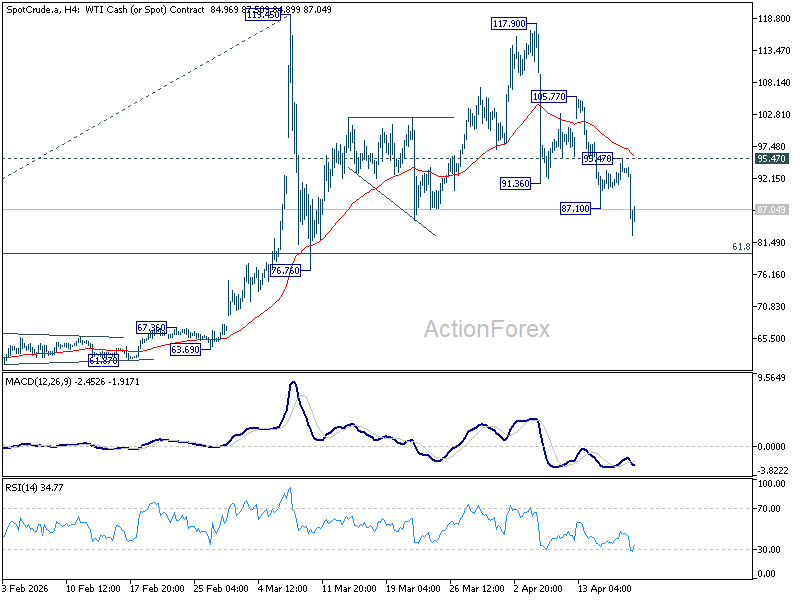

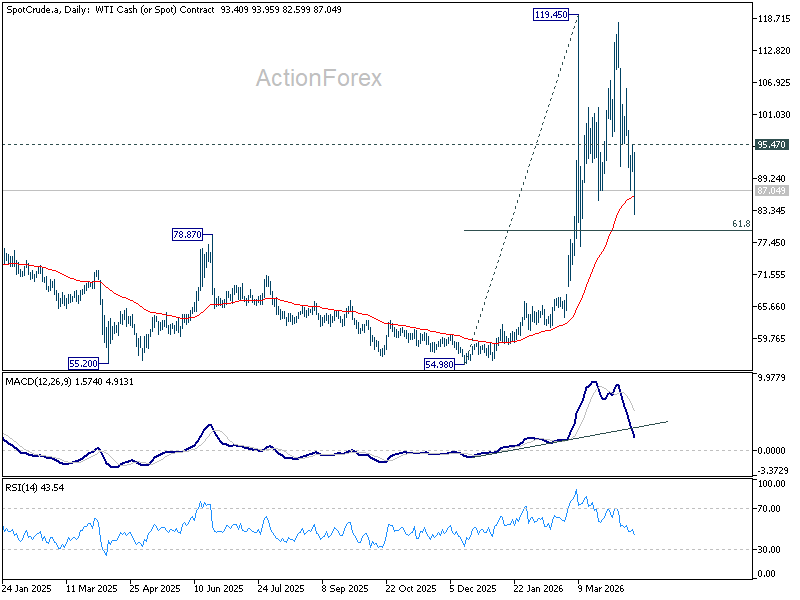

Oil: Still the ultimate signal for global sentiment

Oil remains the most important driver of global market sentiment. The decline in WTI resumed from 117.90 last week, extending sharply lower to a low of 82.59. While further downside is favored in the near term, a decisive break of the 61.8% retracement levels from 54.98 to 119.45 at 79.60 will likely require a more sustained calm in the Middle East – which could include a confirmed and sustained normalization of the Strait of Hormuz. In the absence of that, the psychological level of 80 should serve as a near-term bottom.

Meanwhile, as long as resistance at 95.47 holds, the bias remains to the downside. In other words, while volatility may continue, there is no clear sign of renewed escalation between the United States and Iran as long as this threshold remains unchanged.

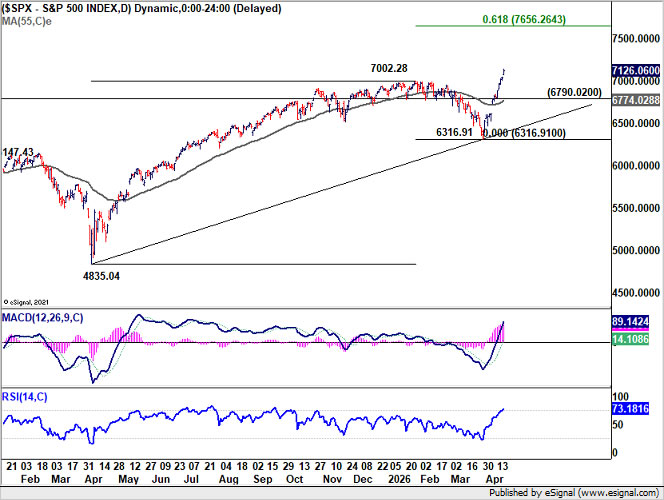

Stocks: New highs as uptrend resumes

The S&P 500 resumed its uptrend last week, surpassing the 7002.28 resistance level and closing at a new record high of 7126.06. While near-term volatility or pullback cannot be ruled out given geopolitical uncertainty, the outlook remains bullish as long as support remains at 6790.02. The current advance continues to target expectations of 61.8% from 4,835.04 to 7,002.28 from 6,316.91 at 7,656.26.

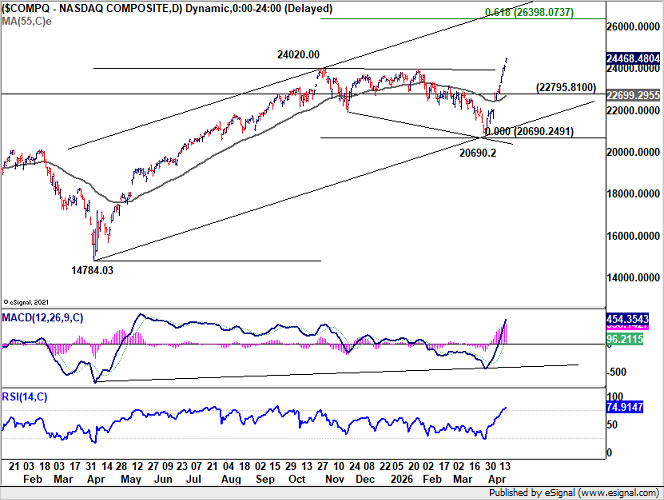

The Nasdaq shows a similar structure, ending the week at a new record high of 24,468.48. The near-term outlook remains bullish as long as support at 22795.81 holds, even in the event of a pullback. The broader upside target is 61.8% forecast from 14784.03 to 24020.00 from 20690.2 at 26398.07 thereafter.

Returns: At key support, bounce or breakout forward

The decline in the US 10-year bond yield from the short-term peak of 4.484 is still corrective so far, indicating that the rise from 3.956 is not yet complete. Yields are now testing a major support group, including the 55 D EMA (now at 4,240), the 50% retracement from 3,956 to 4,484 at 4,220, and the 55 W EMA (now at 4,219).

A strong bounce from this area, followed by a break above the 4,351 resistance level, would indicate that the rally from 3,956 is ready to resume via the 4,484 high. On the downside, a strong break below 4,220 would open the way for a deeper pullback towards the 61.8% retracement levels at 4,157 and below.

Dollar Index: Intact bearish bias below key EMA

The dollar index’s break below the 98.49 support level last week indicates that the rebound from 95.55 has already been completed. More importantly, rejection below the 38.2% retracement from 110.17 to 95.55 at 101.13, combined with failure at the 55 W EMA (now at 99.57), keeps the outlook bearish in the medium term.

Further downside is likely as long as the 55D moving average (now at 98.86) limits any recovery, with an eye on a retest of the low at 95.55. While a break below this level is not the base case yet, it will depend on the momentum of the next stop lower.

Conversely, a sustained move above the 55 D EMA may indicate that the bounce from 95.55 is not yet complete, opening the way for another test of 100.64 and possibly the 101.13 Fibonacci level.

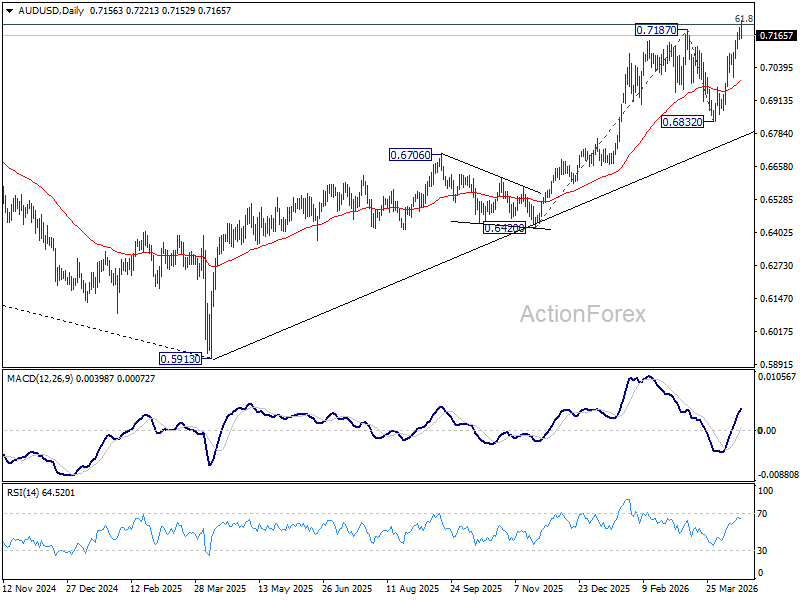

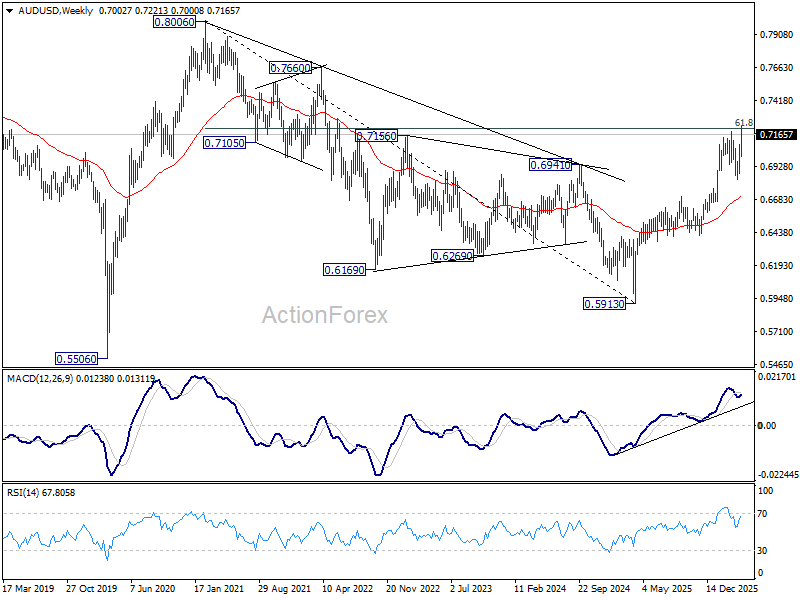

AUD/USD: Breakout structure will rise above 0.72

AUD/USD was the best performer last week, rising 1.46%. While some near-term consolidation is possible after rejection at the 0.72 handle on the first attempt, the broader outlook remains bullish as long as the 55 D moving average remains (now at 0.6985).

More importantly, a decisive break of the 61.8% retracement levels from 0.8006 to 0.5913 at 0.7206 will strengthen the case that it is reversing the downtrend from 0.8006 (2021 high), rather than correcting it. This should pave the way for at least a retest of 0.8006.

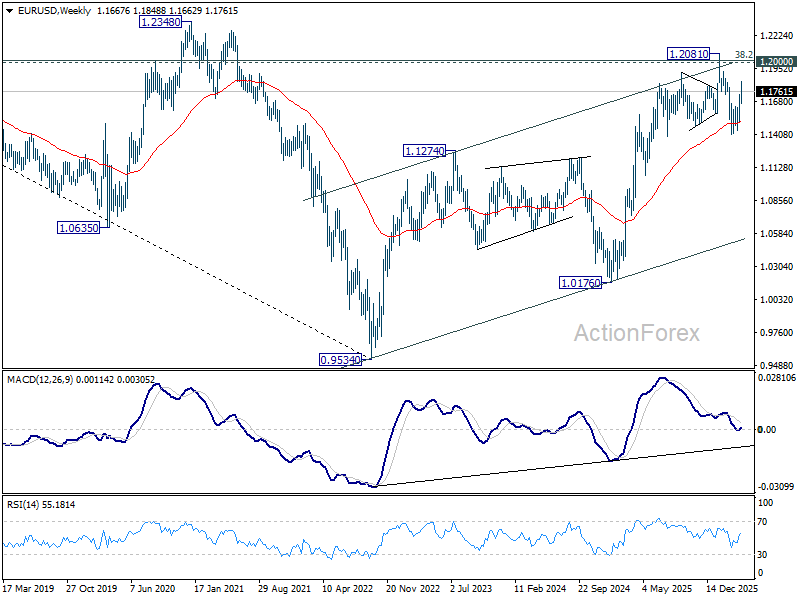

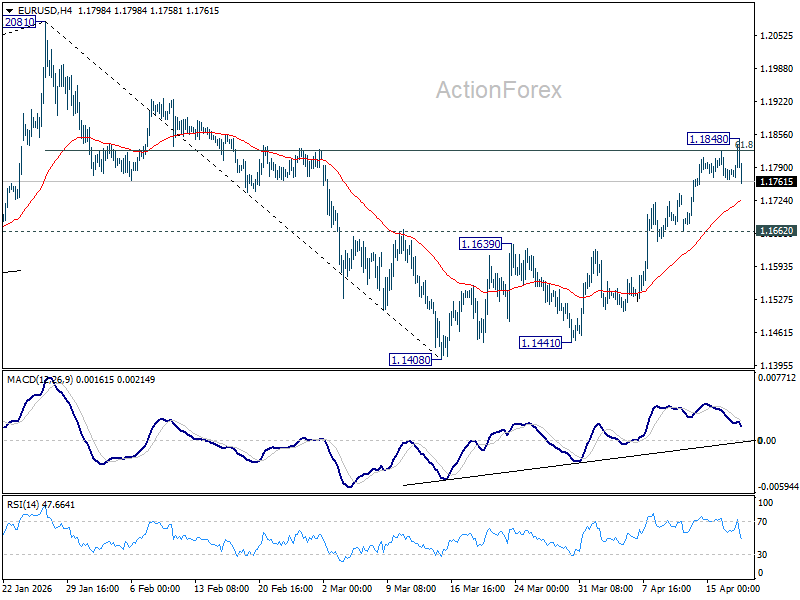

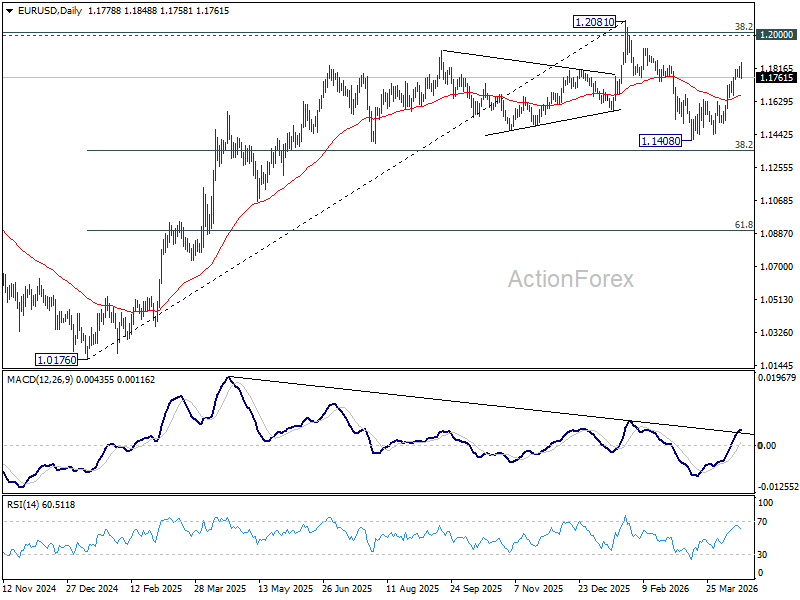

Weekly forecast for EUR/USD

The EUR/USD rally extended from 1.1408 to 1.1848 last week, but failed to break the 61.8% retracement from 1.2081 to 1.1408 at 1.1824 decisively. The initial bias turned neutral this week for the first time. On the upside, continued trading above 1.1824 will pave the way for a retest of the 1.2081 high. However, a strong break of the support at 1.1662 would bring a deeper decline towards the bottom at 1.1408 instead.

In the bigger picture, strong support from the 38.2% retracement level from 1.0176 to 1.2081 at 1.1353 suggests that a pullback from 1.2081 is likely a corrective move. Strong support was also found at the 55 W EMA (now at 1.1507). Focus is back on the key cluster resistance level 1.2. A decisive breakout there would have long-term bullish implications. However, breaking the support 1.1408 will revive the bearish trend reversal in the medium term.

In the long-term picture, the 38.2% retracement from 1.6039 to 0.9534 at 1.2019, which is close to the psychological level of 1.2000 is key to the outlook. Rejection at this level would keep the multi-decade downtrend from 1.6039 (2008 high) intact, and keep the outlook neutral at best. However, a decisive break of 1.2000/19 would signal a reversal of the long-term upside trend, targeting the 61.8% retracement levels at 1.3554.