- Middle East news headlines continue to dominate as hopes for an agreement grow.

- US CPI and retail sales data are struggling to gain attention as Warsh takes office.

- A summary of the UK and BOJ’s Q1 GDP meeting is also on the agenda.

Markets cheer Trump’s peace efforts despite threats

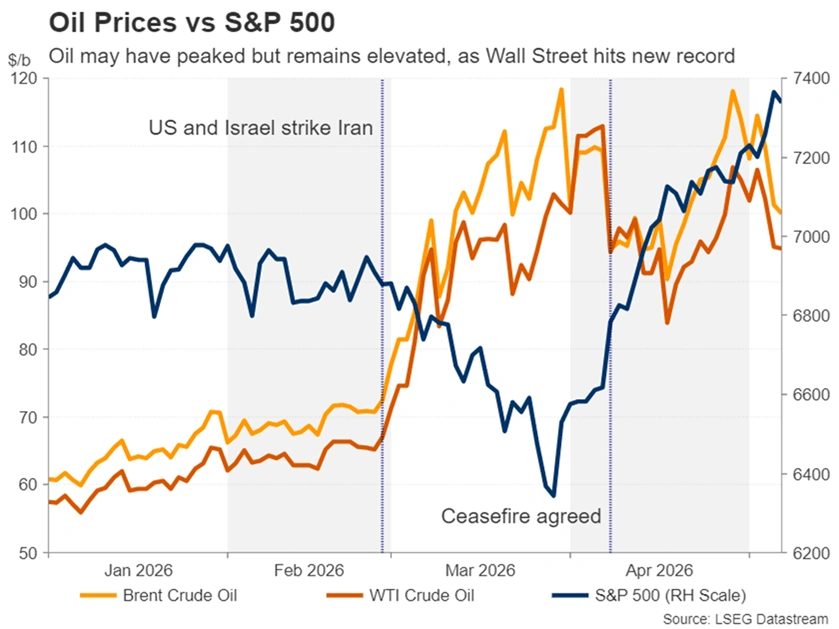

The sudden spike in oil prices in late April was not met with the same risk-off reaction as at the start of the Iranian conflict, as the rise in artificial intelligence overshadowed fears of a worsening energy crisis. However, the rise in inflation expectations has been notable, and even as some of the worst fears have subsided, key measures such as the US 10-year breakeven rate are above pre-war levels.

Investors are likely to be encouraged by the fact that global inflation expectations are still some way off the peaks seen immediately after the Russian invasion of Ukraine. But there is a danger that they are ignoring the real danger that the current energy crisis will become the most severe in history. More importantly, the latest wave of relief is based mostly on hope rather than an actual agreement between the United States and Iran.

Although it is accurate to say that President Trump’s rhetoric indicates a desire to exit the conflict more than to inflame it, the leadership structure in Tehran has become more “fractious,” in the president’s own words. Moreover, the Iranians are known to be tough negotiators, so even if the two sides can agree on a framework for a long-term agreement that includes limits on nuclear enrichment, the risk of re-escalation remains very high amid the battle over who controls the Strait of Hormuz and Israel’s repeated ceasefire violations with Hezbollah.

Even in the best-case scenario of the Strait of Hormuz reopening soon, energy shortages could get worse before they improve, as it will likely take months for oil and gas flows from the Middle East to return to normal. However, Iran negotiations are likely to take a backseat next week, as President Trump travels to China for a meeting with President Xi Jinping where trade will be high on the agenda.

Will the US CPI report matter?

However, investors have trimmed some of their bets on major central banks’ rate hikes in line with the decline in oil prices, with the Fed expected to shift again from rate hikes to cuts. The volatile situation in the Middle East means that the market’s reaction to upcoming releases from the US, specifically Tuesday’s CPI report, will be determined by whether there is any progress in peace talks, or if Trump orders new strikes on Iran.

A major breakout would increase investors’ sensitivity to upward surprises in inflation data, while positive negotiations would reduce it, as any recovery would be considered temporary.

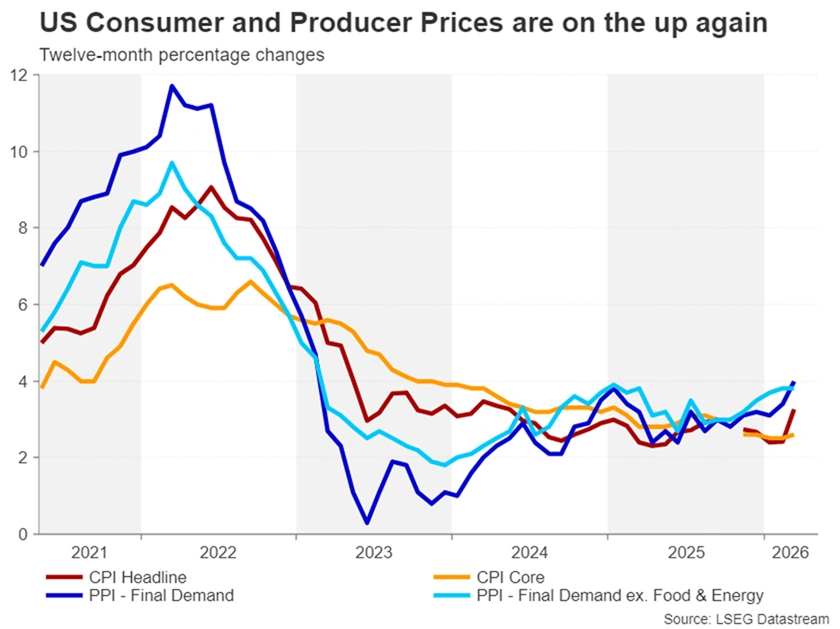

The headline CPI jumped to 3.3% year-on-year in March and is likely to accelerate further in April. The Cleveland Fed estimates a rise to 3.6% y/y, while core CPI is expected to remain unchanged at 2.6% y/y.

Producer prices for the same month are scheduled to be released the next day, Wednesday. The PPI report often tends to cancel out some of the effects of the CPI surprise if it is inconsistent. But if both sets of numbers are hotter than expected, risk appetite is likely to decline as Fed rate cut bets take a hit, with a busy schedule of Treasury auctions next week likely to exacerbate any rise in US yields.

Warsh confirmation awaiting

Also driving the direction of Fed policy next week will be potential comments from Fed chair nominee Kevin Warsh, who appears set to finally be confirmed by the US Senate on Monday, just days before outgoing Chairman Jerome Powell’s term ends on May 15.

Warsh’s nomination has been largely welcomed by investors, as he is likely to champion the need to cut interest rates further. But any overt hints about the kinds of reforms he intends to undertake could spook markets.

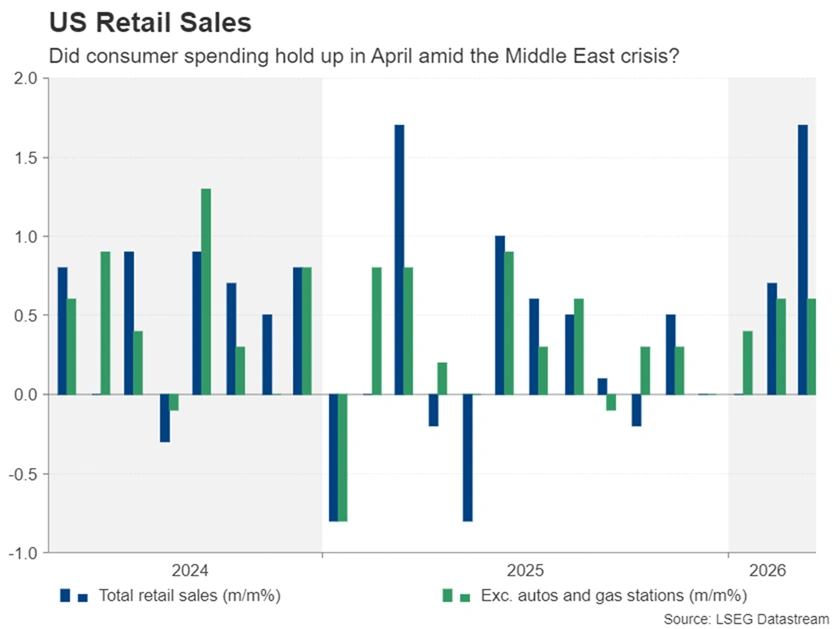

April retail sales figures on Thursday will also be lively, amid some concerns about whether US consumer spending will hold up against the backdrop of higher gasoline prices. Other data will include existing home sales on Monday, and the Empire State Manufacturing Index and industrial production on Friday.

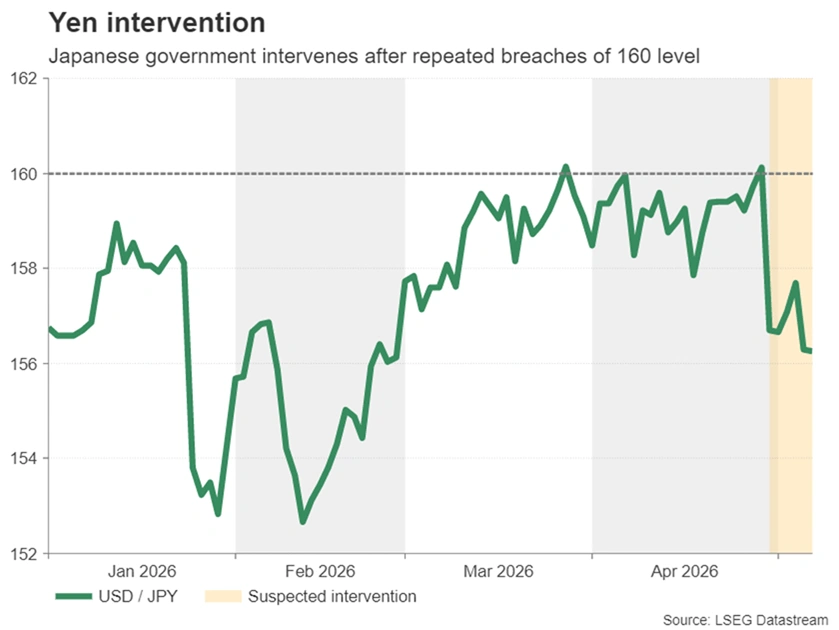

The resilience of the dollar was tested by intervention in the yen

The US dollar’s losses on the back of optimism about ending the Iranian conflict were relatively modest, and could have been lower had it not been for the Japanese government’s intervention in the yen price. But although the Fed’s bets on raising interest rates have diminished, a resumption of the dollar’s bullish trend for 2026 is also not out of the question, as Japanese authorities are suspected to have remained active in the FX market after the April 30 intervention.

The best short-term prospect for the yen is to try to push towards the 152 area against the dollar, which served as resistance twice earlier this year. Such support could come from a summary of the Bank of Japan’s views for its April meeting scheduled to be published on Tuesday.

There were three opponents at the meeting, with hardline voices rising louder. If the summary reveals that other Governing Council members may soon join calls for an imminent rate hike, the yen may enjoy better demand beyond central bank buying.

The British pound is moving cautiously

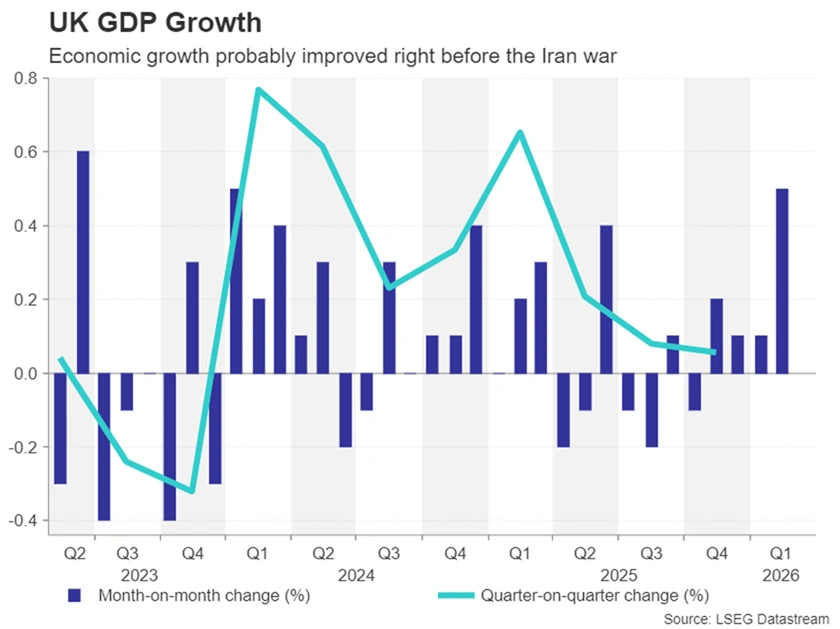

For sterling, whose recovery against the dollar has been constrained by stagflation risks even as the Bank of England sets the stage for interest rate increases in the summer, geopolitical developments are being closely watched for the timing and scale of any tightening.

Next week’s preliminary estimates of first-quarter GDP growth will likely play second fiddle to the headlines on Iran, but will nonetheless be important, particularly the March monthly edition, to gauge how the start of the Iran war will impact the British economy.

The data is due out on Thursday, along with details of sector growth for the full quarter and March.

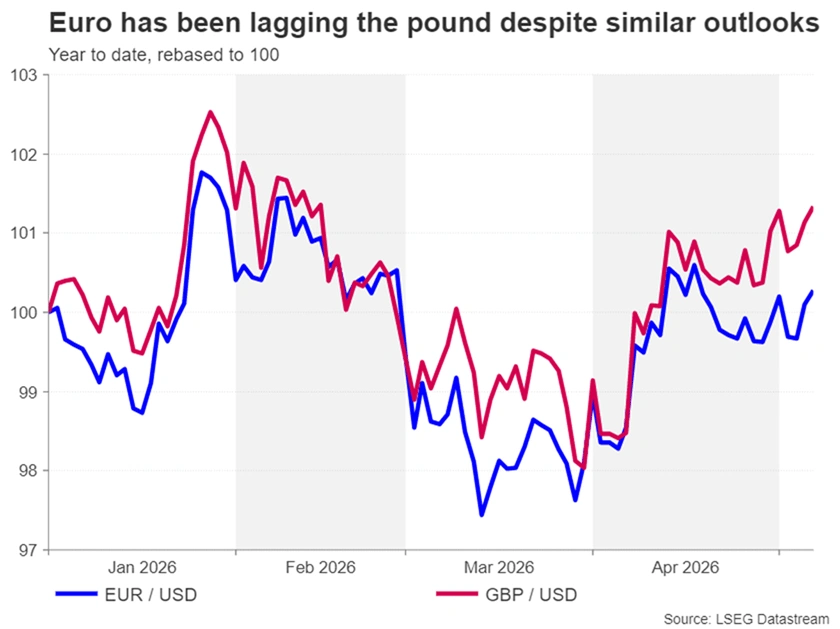

Kiwi shines while euro lags

It’s a very similar story for the euro, which has had a slower recovery than the pound and remains below its mid-April peak. Pricing in a full rate hike of around 25 basis points from the ECB’s expectations at the end of the year following an easing of tensions in the Middle East is likely to be the reason behind the euro’s weak performance.

Quarterly employment figures and a second estimate of first-quarter GDP growth, both on Wednesday, and Germany’s ZEW economic sentiment gauge on Tuesday are highlights of the European docket, although they are unlikely to impact the euro much.

Elsewhere, China is expected to report a jump in both the CPI and PPI on Monday as energy prices continue to rise in April. On Wednesday, Australia’s quarterly wage growth data will be watched for clues about a possible fourth interest rate hike by the Reserve Bank of Australia. Meanwhile, in New Zealand, the Reserve Bank of New Zealand’s survey of quarterly inflation expectations could help the New Zealand dollar’s impressive month-long rally against the US dollar if it shows a slight rise.