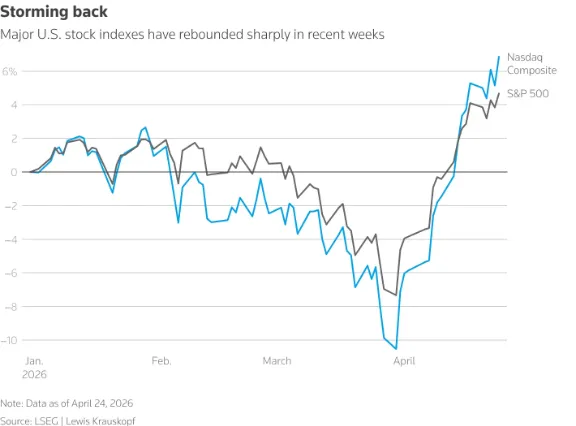

- The S&P 500 and Nasdaq rose to new records during the day, driven by diplomatic hopes for de-escalation in the Middle East and technology performance.

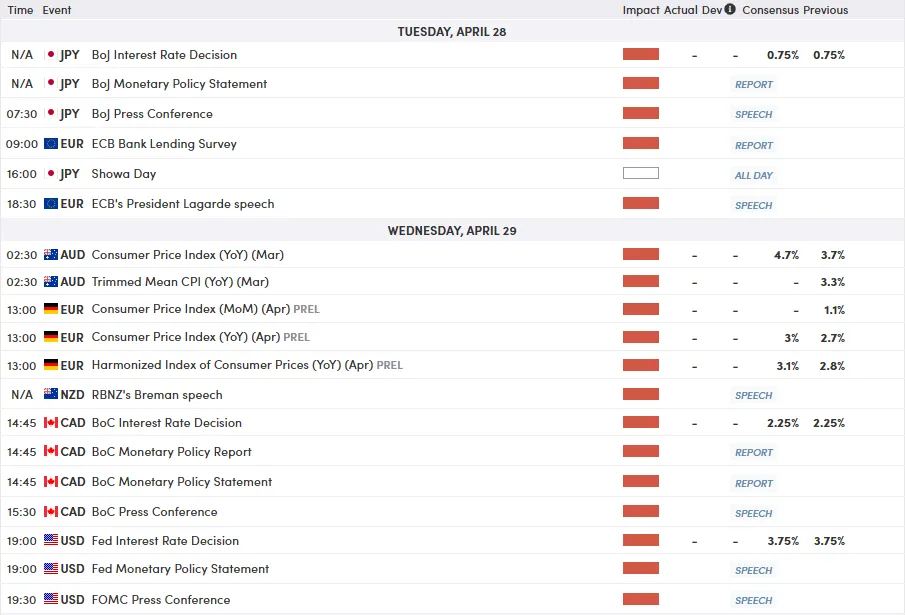

- Next week includes meetings from the Federal Reserve, European Central Bank and Bank of England as well as technology earnings releases.

- The Bank of Japan is the ‘wild card’ facing pressure to suddenly raise interest rates, while markets will also focus on China’s manufacturing PMI, which is at risk of slipping back into deflation.

Global markets find themselves at a crossroads as the week comes to a close, with the narrative shifting between geopolitical caution and corporate optimism. While the US dollar fell slightly on Friday, it is still on track for weekly gains as traders weigh the possibility of a diplomatic solution to the conflict between the US, Israel and Iran.

The US dollar’s path was a reflection of the market’s “wait and see” approach. Optimism about a near-term peace deal has provided temporary relief, while the looming threat of prolonged power outages remains a floor for the currency.

The Dollar Index (DXY) fell 0.11% to 98.71 during Friday’s session, but is still eyeing a 0.50% gain for the week. This relative strength kept the Euro and GBP under pressure, with EUR/USD heading towards a 0.53% weekly loss despite a modest intraday recovery to $1.1699.

Meanwhile, the Japanese yen saw a slight flight to safety, rising to 159.62.

The geopolitical premium is most evident in the energy sector, where Brent and WTI crude oil rose 16% and 11% respectively this week, their second-largest gains since the start of hostilities, as the Strait of Hormuz remains effectively paralyzed.

In the area of stocks, the general mood is certainly more optimistic. The S&P 500 and Nasdaq rose to new intraday records on Friday, driven by a dual driver of diplomatic hope and outperformance in technology. Reports that Iran’s foreign minister is heading to Islamabad for peace talks, coupled with news that US envoys, including Jared Kushner, are prepared to participate in Pakistani-brokered negotiations, have offered a glimmer of hope for de-escalation.

These sentiments were further reinforced by a rise in Intel shares, which helped the technology sector shrug off the release of DeepSeek’s latest AI model and lead the broader market higher.

Earnings season also provides a strong foundation for investor confidence. With more than 80% of S&P 500 companies beating expectations so far, the focus now turns to the high-risk week ahead. Five of the “Magnificent Seven” companies, which represent a large portion of the index’s market capitalization, are scheduled to be announced.

As the S&P 500 and Nasdaq look to post a fourth straight week of gains, the longest streak since late 2024, the market’s resilience will be tested by whether these giants are able to justify their valuations amid a backdrop of persistent inflation fears and a volatile geopolitical landscape.

Source: LSEG

Next week: Central banks are walking a tightrope as geopolitical tensions refuse to dissolve

Markets enter the final week of April facing a familiar, if increasingly acute, dilemma. While the “higher for longer” narrative was the theme of 2025, the spring of 2026 is shaping up to be defined by a “wait and see” impasse. As we look ahead to the week of April 26th, the spotlight is firmly on a trio of central bank meetings with the Federal Reserve, the European Central Bank and the Bank of England, all of whom find themselves caught between tough energy-led inflation and a fragile global growth outlook.

Central Banks: All Bark and No Bite?

The main topic for next week is the “balancing problem” facing global policymakers. Geopolitical instability in the Middle East has kept oil prices buoyant, complicating the inflation trajectory, at a time when markets were hoping for a turn to a pessimistic stance.

Federal Reserve Bank (Wednesday): Jerome Powell is expected to hold his ground in what is scheduled to be his final meeting as president. While the US economy continues to show resilience – with first-quarter GDP expected to rebound to 2.7% – the core personal consumption expenditures deflator remains a thorn in the side of the FOMC. A ‘hold’ decision is expected, with Powell likely emphasizing that while labor market risks are tilted to the downside, the inflation battle is far from over.

European Central Bank and Bank of England (Thursday): Across the Atlantic, the story is remarkably similar. Both the European Central Bank and the Bank of England are expected to keep interest rates unchanged. For the ECB, the flurry of data released on Thursday (GDP and inflation in April) will serve as a reality check. In the UK, Conservative Andrew Bailey is facing a market that has recently ignored his attempts to talk up interest rate hike expectations. The challenge for both is to maintain a hawkish bias to hold inflation expectations steady without accidentally causing a deeper economic contraction.

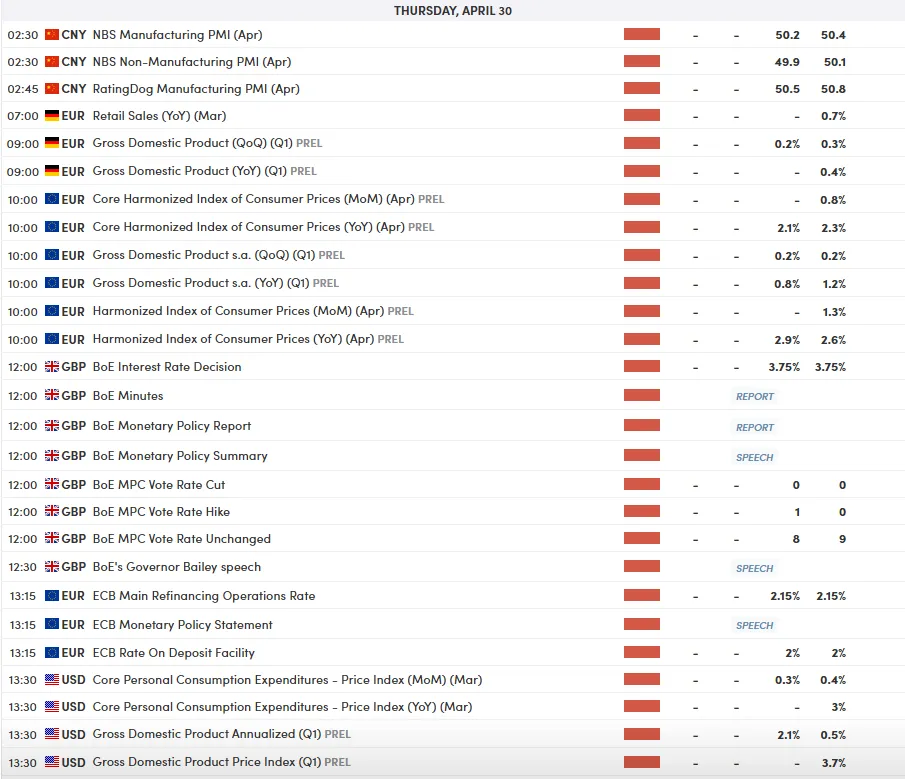

Asia in focus: Bank of Japan and China PMI

As the West grapples with political gridlock, the Asia-Pacific region is bracing for potential volatility.

Bank of Japan (Tuesday): This is the “wild card” of the week. While the consensus leans towards confirmation, a surprise rate hike remains on the table. With the CPI expected to accelerate in Tokyo and real interest rates very negative, the Bank of Japan is under enormous pressure to respond. See the quarterly outlook report for upward revisions to inflation expectations for 2026/2027.

China PMI (Thursday): After a brief entry into expansionary territory, China’s manufacturing PMI is at risk of slipping back into contraction (expected to reach 49.9). Any sign of slowing demand in the world’s second-largest economy could severely impact commodity-linked currencies and broader risk sentiment.

Inflation in Australia (Wednesday): Higher oil prices are expected to push the Australian CPI towards 4.6%. This hot data could force the Reserve Bank of Australia to act as early as May, putting the Australian dollar in the crosshairs.

To see all the economic releases and events affecting the market, see the MarketPulse Economic Calendar. (Click to enlarge)

Weekly Chart – US Dollar Index (DXY)

Technically, the DXY is currently testing an inflection point after a sharp rebound from January lows. After breaking below the ascending ascending channel, the indicator stalled, indicating a loss of upward momentum as it hovers around the 100 and 200 day moving averages.

Main technical notes:

- resistance: The level of 99.56 remains the immediate ceiling. Failure to break this level may lead to a deeper decline. The catalyst may be reaching some form of agreement between the United States and Iran.

- Supports: Immediate support is located at the confluence of the 100/200 moving average (about 98.50). Failure to break above 99.00 would keep the bears in the driver’s seat.

- Indicators: The RSI (bottom) is at 45.726, showing a downward slope after the recent “pivotal” rally.

The trend is currently neutral to bearish. Look for a decisive close below 97.70 to confirm a deeper correction towards 97.00.

On the other hand, a daily close above 100.61 invalidates the downtrend.

Daily chart of the US Dollar Index (DXY), April 24, 2025

Source: TradingView.Com (click to enlarge)

Key motivators

The basic measure of risk. A hawkish Fed “steadiness” could see the dollar challenge recent gains, especially if GDP data surprises to the upside.

Conversely, if the Bank of Japan opts for a hawkish surprise, expect a sharp unwinding in JPY trades, which could lead to a broader “risk off” move across equity markets.

Next week is less about what central bankers will do and more about what they say they might do in June. With inflation proving firmer than expected and growth figures starting to show cracks in rising interest rates, the margin for error has never been narrower.

Traders should remain smart in a week when data and announcements are likely to move in opposite directions.